43% of Americans Can’t Answer a Single Retirement Longevity Question: Why That’s CFOs’ Problem?

Most employees are misjudging how long they’ll live, and it’s putting pressure on CFOs to rethink retirement planning. These fast facts show why.

Linkedin

Linkedin

Facebook

Facebook

Twitter

Twitter

Copy url

Copy url

3 trillion

cashless transactions by 2030

50%

e-commerce via digital wallets by 2024

70%

rise in payment fraud since 2020

60%

of central banks exploring CBDCs

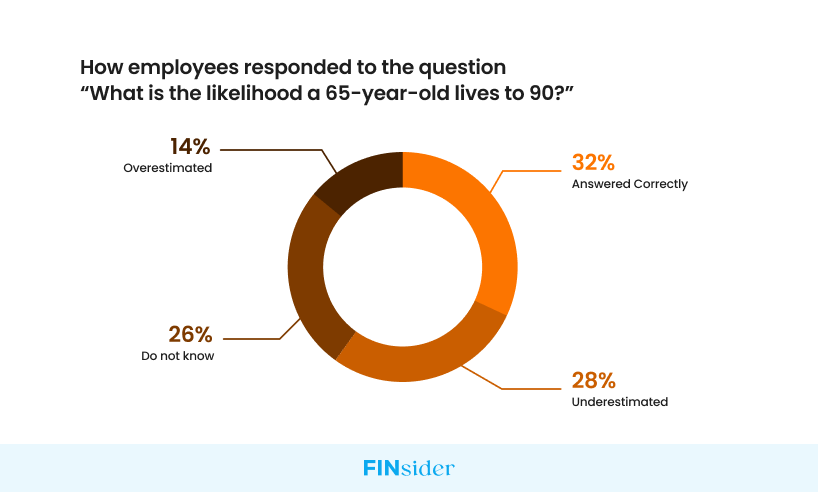

When was the last time you asked your employees how long they expect to live in retirement?

Odds are, they’ve either never thought about it or they’re wrong. New research shows nearly half of U.S. adults couldn’t answer even one longevity question correctly. And for CFOs managing benefits and retirement programs, that gap in understanding could be more than a stat, it could be a liability.

Most Employees Don’t Understand How Long Retirement Lasts

According to new data from the TIAA Institute and the Global Financial Literacy Excellence Center, 43% of Americans failed to answer any longevity questions correctly. Even basic facts like the average life expectancy of a 65-year-old eluded the majority.

Why it matters: If employees are budgeting for 10 or 15 years of retirement instead of 25 or 30, they’ll save less, retire earlier, and increase their reliance on employer-sponsored benefits longer than expected.

Retirement Confidence Depends on Financial Literacy

There’s a clear link between knowledge and confidence. Among those who got 4–5 answers right, 26% said they’re very confident about retirement. But among those who missed every question? That number plummeted to 10%.

That confidence-or-lack of it, translates into behavior. Financially fluent employees are more likely to save, invest, and plan. Those in the dark tend to delay or disengage. For CFOs, this results in underused retirement plans, misaligned benefits strategies, and rising long-term risk.

Those Who Expect Longer Retirements Save More, But Many Don’t

Workers expecting 20–30+ years of retirement are more likely to plan. Nearly 80% of them save regularly, and nearly half calculate how much they need. But this group is in the minority. Many workers expect shorter retirements or don’t have an estimate at all, which means they’re not preparing adequately.

This expectation gap affects everything from 401(k) participation to interest in annuities and other lifetime income tools, many of which remain underutilized due to a lack of understanding.

The Gaps Extend Across Generations, Genders, and Income Levels

Even older generations, Baby Boomers and the Silent Generation, only got about half of the longevity questions right. Meanwhile, men outperformed women slightly (43% correct vs. 38%). And questions about Medicare and Social Security stumped almost everyone.

These persistent gaps mean one-size-fits-all messaging won’t work. Finance leaders need to collaborate with HR to tailor communication and education strategies around retirement planning, especially if they want to shift behavior long-term.

Poor Longevity Literacy = Higher Risk for CFOs

If employees retire too early, under-save, or ignore critical tools like annuities, CFOs could face long-term pressure on benefits design, matching contributions, and overall plan sustainability. It’s not just about generosity, it’s about strategy and survival.

A workforce that misjudges retirement needs can drain resources faster than anticipated. But a workforce that understands the risks is more likely to plan wisely and stick with an employer who helps them do it.

It’s easy to assume retirement planning is someone else’s problem until the costs show up on your balance sheet. The 43% stat is more than a red flag, it’s a wake-up call for CFOs.

So ask yourself: What steps are you taking to make sure your workforce understands the retirement reality and is financially ready for the long haul?

Want more insights? Subscribe to our finance newsletter for the latest in finance—from the best finance newsletters and compelling finance stories to treasury, R2R and AR insights.