Accounts Receivable Solutions for

Manufacturing Companies

Trusted by 1500+ global enterprises and mid-sized companies to automate complex distributor

emittances, speed payment matching across multi-entity ledgers, and

free up working capital for production and inventory spend.

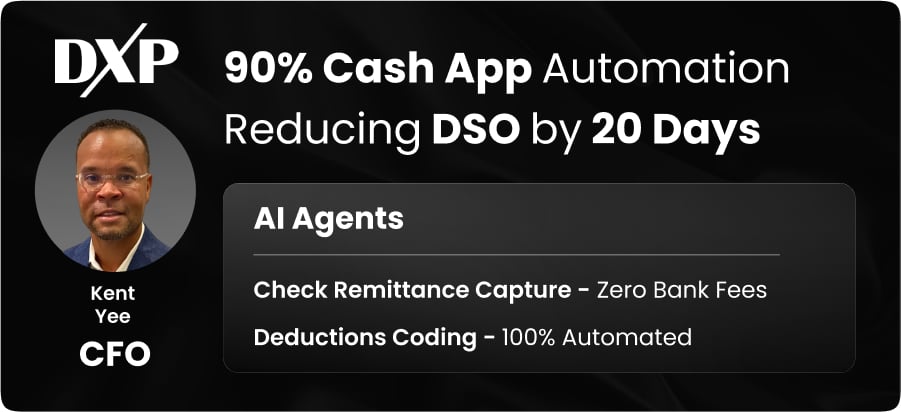

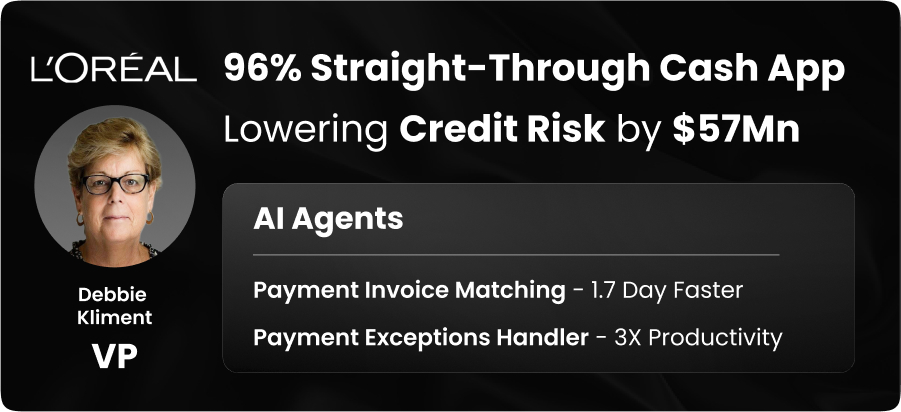

Trusted by leading companies worldwide