What Is General Ledger Reconciliation: Types, Best Practices and Importance

Last Updated: 16 July, 2026

•

Soumi Sarkar Fintech content strategist

S

Soumi Sarkar

Soumi specializes in O2C, finance, and accounting transformation with a focus on bringing a domain-led perspective to accounting, finance and order-to-cash transformation. She crafts insight-driven, CFO-aligned content that helps finance teams optimize operational workflows and drive measurable outcomes. Beyond her professional work, Soumi is a published author of two books, a poetess, an avid reader, and a storyteller who enjoys exploring narratives across both B2B and creative formats.

Analyst Recognition

HighRadius Named a Challenger in 2026 Gartner® Magic Quadrant™ for Financial Close and Consolidation Solutions

Discover how HighRadius brings practical, results-driven AI to record-to-report processes with automation, anomaly detection, and continuous close capabilities.

GL reconciliation ensures financial accuracy by validating account balances against bank statements and sub-ledgers.

Automated reconciliation tools eliminate manual data entry errors, allowing accounting teams to streamline the close.

Integrated systems provide robust audit trails and real-time oversight to ensure compliance with financial regulations.

Accurate financial reporting starts with accurate account balances. General ledger reconciliation provides the control framework that finance teams use to verify every account balance against the records that back it up, whether that’s a bank statement, a subledger, or a supporting schedule. It is one of the few controls that catches problems while they’re still small, like a missed invoice, a timing gap, or a data entry slip, before they turn into a misstated financial statement.

This guide walks through what general ledger reconciliation actually involves, the types of reconciliation that fall under it, the step-by-step process, how often it should happen, and the best practices that separate teams with a clean, audit-ready close from teams still chasing down discrepancies days after month-end.

What is a General Ledger Reconciliation?

General ledger (GL) reconciliation is the process of comparing the balances recorded in a company’s general ledger against the independent records that support them, bank statements, subledgers, vendor invoices, or supporting schedules, to verify the accuracy and integrity of financial data.

The general ledger itself is the master record of every financial transaction a business makes, organized into accounts like cash, accounts receivable, accounts payable, and revenue. Reconciliation is the check that keeps that master record honest: it catches missing entries, duplicate postings, timing differences, and outright errors before they make their way into a financial statement.

Why it Matters

The objective of GL reconciliation is to ensure that recorded balances reflect actual transactions and to identify and correct discrepancies, errors, or fraudulent activity.

Enables Better Decisions – Ensures leaders have accurate data for planning and analysis.

Confirms accuracy – GL balances match what actually happened, as evidenced by external documentation.

Strengthens internal control – it’s a built-in check against errors, omissions, and fraud.

Supports reliable financial reporting – statements built on reconciled balances hold up under review.

Enables audit-readiness – a documented reconciliation trail is what auditors look for when testing internal controls.

Reconciliation Is the Foundation of Financial Accuracy.

Discover how AI is helping finance teams transform general ledger reconciliation with greater accuracy, stronger controls, and faster financial close.

Understanding the Process of General Ledger Reconciliation

General ledger reconciliation follows a consistent sequence, whether it’s done manually or with the help of software. Here’s how the process typically works.

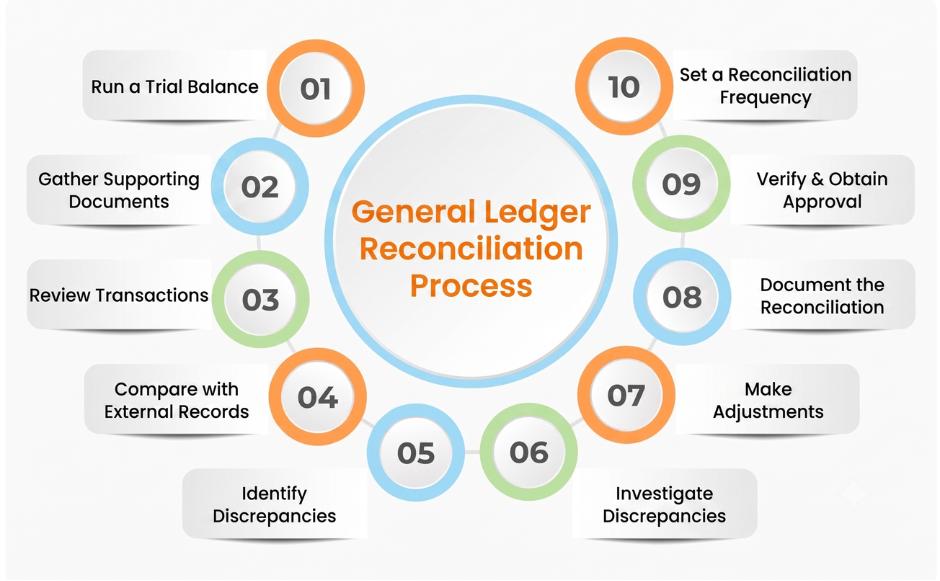

1. Run a trial balance

Before reconciling anything, pull a trial balance for the period, a summary of every account and its ending balance. This confirms which accounts exist, flags any new accounts added since the last reconciliation, and gives the full list of what needs to be checked before one starts comparing anything against outside records.

2. Gather supporting documents

Collect the records each account will be checked against, like bank statements, subledgers, vendor invoices, receipts, and any other internal records for the period being reconciled.

3. Review transactions

Review the transactions recorded in the general ledger for the period. Confirm they’re accurately recorded, categorized, and posted to the correct accounts.

4. Compare with external records

Compare each GL account against its corresponding external record. Pay attention to dates, amounts, descriptions, and account numbers. Small mismatches here are often where discrepancies first surface.

5. Identify discrepancies

Flag any differences between the GL and the external record. Common discrepancies include outstanding checks, deposits in transit, unrecorded transactions, duplicate entries, or recording errors.

6. Investigate discrepancies

Trace each discrepancy back to its source. Verify supporting documents and, where needed, check with the relevant stakeholder. The goal is to determine whether the gap is a timing difference, an error, or something else entirely, since the fix depends on which one it is.

7. Make adjustments

Correct the discrepancy on whichever side actually needs it, recording a missing transaction, fixing an error, reversing a duplicate, or updating a balance.

8. Document the reconciliation

Record what was found, what was adjusted, and how it was resolved. This documentation is what auditors look for when testing your controls, so treat it as a required output, not an afterthought.

9. Verify and obtain approval

Confirm the reconciled balances match across the GL and supporting records, double-check the adjustments, and obtain approval or sign-off from authorized personnel, such as a finance manager or controller, to confirm the completion and accuracy of the general ledger reconciliation

10. Set a reconciliation frequency

Establish a schedule for regular reconciliations, such as monthly, quarterly, or annually, depending on the volume and complexity of transactions.

Monthly, at minimum – cash, accounts receivable, accounts payable, and other high-volume or high-risk accounts, since these are the accounts most likely to hide a discrepancy if left too long.

Quarterly – lower-volume, lower-risk accounts where errors are less likely and less material if they do occur.

Weekly or daily – businesses with high transaction volume or multiple entities, where waiting a full month lets discrepancies pile up and get harder to trace.

The less time between reconciliations, the smaller and easier each discrepancy is to catch and fix, which is the whole reason frequency matters as much as the process itself.

Types of General Ledger Reconciliation

General ledger reconciliation is a discipline applied account by account, and each type of account gets checked against a different kind of supporting record. Together, these types make up what “GL reconciliation” actually covers. The most critical types include:

1. Bank Reconciliation

Bank reconciliation aligns the company’s general ledger cash accounts with external bank statements. The bank reconciliation process verifies that deposits, withdrawals, and fees are accurately recorded and helps detect timing differences, errors, or fraudulent activity. It provides assurance that cash balances reported to leadership are reliable.

2. Credit Card Reconciliation

Credit card reconciliation ensures that expenses charged to company cards match approved transactions and receipts. By comparing card statements against the general ledger, finance teams can catch duplicate charges, unapproved spending, and misclassified expenses, reducing the risk of leakage and strengthening spend control.

3. Payment Reconciliation

Payment reconciliation connects customer payments—via ACH, wire, or checks—with open invoices in the general ledger. This step is critical to reducing unapplied cash, accelerating revenue recognition, and giving CFOs real-time visibility into collections performance.

4. Account Reconciliation

Account reconciliation validates balances across accounts such as accounts receivable, accounts payable, and accrued expenses. The account reconciliation process helps businesses ensure every figure in the general ledger ties back to supporting records. This process reduces reporting risk and builds confidence in period-end financials.

5. Intercompany Reconciliation

For businesses operating across multiple entities or subsidiaries, intercompany reconciliation matches transactions between related entities, such as inter-entity loans, shared expenses, or transfer pricing, so that balances agree on both sides of the transaction. Left unreconciled, intercompany discrepancies are a common source of consolidation errors and audit findings.

6. Fixed Asset Reconciliation

Fixed asset reconciliation compares the fixed asset register (the detailed record of equipment, property, and other long-term assets) against the GL’s fixed asset accounts, accounting for depreciation, disposals, and new acquisitions along the way. It ensures the balance sheet reflects what the business actually owns.

Though these are the most common, businesses often perform many other types of reconciliation to maintain accurate, compliant, and audit-ready books.

Ebooks

Complex Reconciliations Need Smarter Technology.

Discover how finance teams use AI to simplify reconciliation across accounts, entities, and systems while improving accuracy and accelerating close.

Let’s say XYZ Company is closing its books for the month of June. As part of the month-end close, the accounting team reconciles three key general ledger accounts: Cash, Accounts Receivable, and Accrued Expenses. Each account is checked against a different supporting record.

1. Cash Account

The GL shows a cash balance of $50,000. The bank statement shows $47,200.

The team traces the $2,800 gap and finds:

A vendor check for $3,000 was issued and recorded in the GL, but hasn’t cleared the bank yet (outstanding check)

A $200 bank service fee was deducted by the bank, but has not yet been recorded in the GL

Item

Amount

Bank Balance

$47,200

Add: Outstanding Check

$3,000

Less: Bank Service Fee

($200)

Adjusted Balance

$50,000

Once the outstanding check clears and the bank fee is recorded, both sides agree, no error, just timing.

2. Accounts Receivable

The GL shows AR of $80,000. The AR subledger (the detailed record of every open customer invoice) totals $83,000.

Investigating the $3,000 gap, the team finds that a customer payment of $3,000 was received and recorded in the GL, but the corresponding invoice was never marked as closed in the subledger, so the subledger still shows it as open.

Here, the subledger is corrected to reflect that the invoice was paid, bringing both records to $80,000. This is a process error, not a timing difference; someone missed a step.

3. Accrued Expenses

The GL shows accrued expenses of $12,500. The supporting schedule (a list of expenses incurred but not yet invoiced) totals $15,500.

The team traces the $3,000 difference and finds a data entry error: an accrual of $3,000 was calculated correctly on the schedule, but entered into the GL as $500, a simple transposition mistake.

Here, the GL entry is corrected to $15,500 to match the schedule, since the schedule is the accurate source.

Common Mistakes to Avoid in General Ledger Reconciliation Process

Discrepancies in the general ledger can stem from a range of causes, and overlooking them affects the accuracy of financial reporting. Here are the most common mistakes to watch for:

Data entry errors – Typing mistakes, transposition errors (entering numbers in the wrong order), or incorrect categorization of transactions can all create discrepancies between the general ledger and external records.

Timing differences – Transactions recorded in the general ledger and in external records don’t always land on the same day, a check that hasn’t cleared yet, or a deposit still in transit. These cause temporary discrepancies that resolve once both sides catch up.

Missing transactions – Failing to record a deposit, payment, or invoice results in an understated or overstated account balance until it’s caught.

Duplicate entries – Recording the same transaction more than once inflates account balances and distorts financial reporting.

Bank errors – Financial institutions make mistakes too; processing errors or misstatements on a bank statement can create discrepancies that have nothing to do with your own records.

Reconciliation errors – Sometimes the mistake is in the reconciliation itself, overlooked transactions, miscalculated adjustments, or discrepancies that weren’t investigated thoroughly enough to actually resolve.

Fraudulent activity – Unauthorized transactions, fictitious entries, or misappropriated funds can also show up as reconciliation discrepancies. This is one of the reasons reconciliation functions as a real control, not just a bookkeeping step; it’s often the mechanism that catches this kind of activity before it compounds.

System glitches – Technical errors in accounting software or reconciliation tools can introduce inaccuracies of their own if they aren’t caught and corrected promptly.

Miscommunication across teams – A lack of coordination between departments or individuals involved in reconciliation can lead to misunderstandings, delays, or errors in recording and resolving discrepancies.

Failure to reconcile regularly – Delaying or skipping reconciliations lets errors accumulate, making them harder to trace and more expensive to fix the longer they sit.

General Ledger Reconciliation Best Practices

Getting reconciliation right consistently comes down to a handful of practices that separate teams with a clean, predictable close from teams still chasing discrepancies days after month-end.

1. Standardize the process

Use the same steps, templates, and documentation format for every account and every period. A standardized process means any team member can pick up a reconciliation and understand what was done and why, which matters as much for cross-coverage during time off as it does for audit review.

2. Prioritize by materiality and risk

Not every account carries the same risk. High-volume, high-value accounts (cash, AR, AP) deserve reconciliation first and most often. Reconcile to a sensible materiality threshold rather than chasing every rounding difference; the goal is catching discrepancies that actually matter, not perfection for its own sake.

3. Reconcile on a consistent schedule

Set a frequency for each account based on its risk and volume (see the process section above) and stick to it. Reconciliations that happen “whenever there’s time” are the ones that let small discrepancies turn into large ones.

4. Segregation of duties

Have one person prepare the reconciliation and a different person review and approve it, commonly called a maker-checker workflow. This segregation of duties catches errors the preparer might miss and is a control that auditors specifically look for.

5. Investigate before adjusting

Don’t just force two numbers to match. Trace every discrepancy to its root cause first, timing difference, missing entry, or actual error, since the correct fix depends entirely on which one it is. Adjusting without investigating hides the underlying problem instead of fixing it.

6. Document everything

Every reconciliation should leave a trail: what was compared, what didn’t match, why, and what was done about it. This documentation is what makes a reconciliation audit-ready, not just internally complete.

7. Review and update the process periodically

As the business grows, adds entities, or changes systems, the reconciliation process should be revisited, as new accounts, new data sources, and new risks all change what “standard” should look like.

8. Keep communication open across teams

Discrepancies often trace back to another department, a sales team booking revenue early, or an AP team missing an invoice. Reconciliation works best when finance has a clear channel to flag and resolve these issues with the teams that caused them, rather than adjusting around the problem repeatedly.

Ebooks

Turn Reconciliation Best Practices Into Better Close Outcomes

Explore how leading finance teams use standardized processes, real-time data, and AI to improve close accuracy and strengthen financial controls.

Signs Your Reconciliation Process Needs an Upgrade

Even teams following good practices can outgrow a manual process. Here are the signs it’s time to look at how your reconciliation actually gets done.

1. Close takes longer every cycle

If reconciliation is consistently the bottleneck at month-end and it’s taking longer this quarter than it did last quarter, despite no major change in the business, that’s usually a sign the process hasn’t kept pace with transaction volume.

2. The same discrepancies keep reappearing

If you’re resolving the same type of mismatch every single period, the process is treating a symptom rather than fixing the root cause. Recurring discrepancies usually point to a broken upstream process (like the invoice-closing gap in the AR example earlier), not a one-off error.

3. Reconciliations rely on one person’s institutional knowledge

If only one team member really knows how a particular account gets reconciled, which spreadsheets to pull, which quirks to expect, that’s a documentation gap, not a resourcing win. It becomes a real risk the moment that person is out or leaves.

4. Spreadsheets are the system of record

Manual, spreadsheet-based reconciliation works at small scale, but it doesn’t scale cleanly with more accounts, more entities, or more transaction volume, and it leaves little audit trail beyond whatever version of the file happens to survive.

5. Auditors are asking more questions than they used to

An increase in audit follow-up questions, especially around documentation or timing of reconciliations, is often the first external signal that the process isn’t keeping up with the business’s growth or complexity.

6. The team spends more time matching than investigating

If most of the reconciliation cycle goes into manually matching line items rather than actually investigating the discrepancies that matter, the team’s time is going to the wrong part of the process.

None of these signs mean the underlying practices are wrong; they usually mean the process has outgrown manual execution. That’s typically where automation and reconciliation software come in, which is what the next section covers.

Manual vs Automated General Ledger Reconciliation

Aspect

Manual General Ledger Reconciliation

Automated General Ledger Reconciliation

Accuracy

Prone to human error, missed entries, and duplicates

Unlock 30% Faster General Ledger Reconciliation With HighRadius

General ledger reconciliation is the control tower of financial accuracy. Without it, businesses risk misstated earnings, hidden fraud, and audit exposure. Yet legacy tools and manual processes simply can’t keep up with the pace and scale of modern finance. Fragmented spreadsheets, siloed systems, and late-cycle scrambles slow down your close, compromise accuracy, and leave your business exposed.

HighRadius General Ledger Reconciliation Software changes that. It is built on an agentic AI-powered platform designed for speed, scale, and precision. It comes with 22 pre-built AI agents purpose-built for R2R reconciliation and for anything unique to your business. The R2R Agent Builder lets you upload your own Excel-based processes and convert them into custom agents tailored to your specific close and consolidation needs. The result: reconciliation shifts from a manual grind into a proactive, largely automated process, giving your finance team end-to-end control, eliminating repetitive busywork, and freeing them up to deliver the insights that actually move the business forward.

Here’s how HighRadius gets you to a 30% faster close, with up to 99% accuracy:

AI-Powered Matching – Auto-match GL balances against sub-ledgers, bank statements, AR/AP, and credit card data, in real time, with zero manual chasing.

Anomaly Detection – Catch outliers before they ever hit your trial balance, cutting review cycles and eliminating month-end surprises.

Journal Entry Automation – Generate, validate, and post recurring entries automatically, with approvals and audit trails built right in.

A Unified Dashboard – See every reconciliation, every exception, and every owner across every entity, in one place.

Built-In Compliance – Automate SOX controls with embedded documentation, approvals, and substantiation, so you’re always audit-ready.

The results speak for themselves: a 90% transaction auto-match rate. 95% journal posting automation. Teams that used to spend days chasing discrepancies now spend that time on strategy instead.

Account Reconciliation made easy with HighRadius

Do more with less effort. Achieve a 90% transaction auto-match rate and a 95% journal posting automation.

Match transactions in a jiffy with our AI-based flexible rule engine.

Reconciliation Control Tower

Monitor, control, and reconcile with automated reconciliation checklists.

Journal Entry Automation

Automate 95% of journal entries with an AI-based Excel-like interface.

Substantiation

Cover 100% GL accounts with automated data ingestion from the system of records.

Maker Checker Workflow

Gain visibility and control over the reconciliation process.

Frequently Asked Questions (FAQs)

1. What is the difference between bank reconciliation and general ledger reconciliation?

Bank reconciliation is a subset of general ledger reconciliation. While general ledger reconciliation verifies all balances and transactions in the general ledger, bank reconciliation specifically compares cash transactions recorded in the books with those appearing on bank statements. In short, bank reconciliation focuses on one account, while general ledger reconciliation covers all accounts for accuracy and completeness.

Bank reconciliation is a subset of general ledger reconciliation. While general ledger reconciliation verifies all balances and transactions in the general ledger, bank reconciliation specifically compares cash transactions recorded in the books with those appearing on bank statements. In short, bank reconciliation focuses on one account, while general ledger reconciliation covers all accounts for accuracy and completeness.

2. How do you balance a general ledger account during reconciliation?

Balancing a general ledger account requires reviewing all posted transactions, classifying them as debits or credits, and verifying totals. During the general ledger reconciliation process, adjusting entries may be posted to correct errors or timing differences. Once adjustments are complete, the account should show matching debit and credit balances, ensuring accuracy for reporting.

Balancing a general ledger account requires reviewing all posted transactions, classifying them as debits or credits, and verifying totals. During the general ledger reconciliation process, adjusting entries may be posted to correct errors or timing differences. Once adjustments are complete, the account should show matching debit and credit balances, ensuring accuracy for reporting.

3. How do you reconcile a general ledger in Excel?

General ledger reconciliation in Excel typically uses formulas like VLOOKUP, SUMIF, and COUNTIF. These help locate missing entries, flag mismatched amounts, and detect duplicates. Many businesses use a general ledger reconciliation template in Excel to standardize the process, reduce manual errors, and ensure consistent financial reporting.

General ledger reconciliation in Excel typically uses formulas like VLOOKUP, SUMIF, and COUNTIF. These help locate missing entries, flag mismatched amounts, and detect duplicates. Many businesses use a general ledger reconciliation template in Excel to standardize the process, reduce manual errors, and ensure consistent financial reporting.

4. What is general ledger reconciliation with an example?

General ledger reconciliation means comparing GL balances against external records. For example, if your GL shows a bank account balance of $100,000 but the bank statement shows $95,000, you investigate differences like outstanding checks or deposits in transit. After adjustments, both balances should match, providing accurate reporting.

General ledger reconciliation means comparing GL balances against external records. For example, if your GL shows a bank account balance of $100,000 but the bank statement shows $95,000, you investigate differences like outstanding checks or deposits in transit. After adjustments, both balances should match, providing accurate reporting.

5. Is there a general ledger reconciliation template?

Yes, many organizations use a general ledger reconciliation template, often in Excel. These templates provide structured fields for account details, balances, supporting documents, and reviewer approvals. Using a template standardizes reconciliation, reduces errors, and ensures compliance with audit requirements.

Yes, many organizations use a general ledger reconciliation template, often in Excel. These templates provide structured fields for account details, balances, supporting documents, and reviewer approvals. Using a template standardizes reconciliation, reduces errors, and ensures compliance with audit requirements.

6. How is general ledger reconciliation different from account reconciliation?

General ledger reconciliation focuses on verifying overall GL balances against supporting records, while account reconciliation drills down into individual accounts, making it a more granular subset of the broader GL reconciliation process.

General ledger reconciliation focuses on verifying overall GL balances against supporting records, while account reconciliation drills down into individual accounts, making it a more granular subset of the broader GL reconciliation process.

7. What do you do when the same discrepancy shows up in both account reconciliation and GL reconciliation?

When the same discrepancy appears in both account reconciliation and GL reconciliation, trace the transaction back to its source first. For example, if a vendor payment reflects differently across both, verify whether it was posted correctly on both sides and resolve it at the root rather than adjusting each reconciliation independently.

When the same discrepancy appears in both account reconciliation and GL reconciliation, trace the transaction back to its source first. For example, if a vendor payment reflects differently across both, verify whether it was posted correctly on both sides and resolve it at the root rather than adjusting each reconciliation independently.

8. How do you manage GL reconciliation and account reconciliation when multiple entities are closing at the same time?

Managing GL reconciliation and account reconciliation across multiple entities simultaneously can get overwhelming without a clear plan. Prioritize high-risk or high-value accounts first, assign clear ownership to each entity, and use a centralized tracker to monitor GL reconciliation and account reconciliation progress and avoid bottlenecks during simultaneous closes.

Managing GL reconciliation and account reconciliation across multiple entities simultaneously can get overwhelming without a clear plan. Prioritize high-risk or high-value accounts first, assign clear ownership to each entity, and use a centralized tracker to monitor GL reconciliation and account reconciliation progress and avoid bottlenecks during simultaneous closes.

Resource Library

Resource Hub

ASSETS

Cash Flow Calculator (FREE)

Track operating and net cash flow while forecasting balances to maintain liquidity and financial control.

HighRadius Named a Challenger In 2025 Gartner® Magic Quadrant™ for Financial Close and Consolidation Solutions

HighRadius stands out as a challenger by delivering practical, results-driven AI for Record-to-Report (R2R) processes. With 200+ LiveCube agents automating over 60% of close tasks and real-time anomaly detection powered by 15+ ML models, it delivers continuous close and guaranteed outcomes—cutting through the AI hype. On track for 90% automation by 2027, HighRadius is driving toward full finance autonomy.

HighRadius Named ‘Rising Star’ in 2024 ISG Provider Lens™ Finance and Accounting Platforms Report

HighRadius leverages advanced AI to detect financial anomalies with over 95% accuracy across $10.3T in annual transactions. With 7 AI patents, 20+ use cases, FreedaGPT, and LiveCube, it simplifies complex analysis through intuitive prompts. Backed by 2,700+ successful finance transformations and a robust partner ecosystem, HighRadius delivers rapid ROI and seamless ERP and R2R integration—powering the future of intelligent finance.

HighRadius Named As A Major Player For Treasury & Risk Management Software By IDC

HighRadius is redefining treasury with AI-driven tools like LiveCube for predictive forecasting and no-code scenario building. Its Cash Management module automates bank integration, global visibility, cash positioning, target balances, and reconciliation—streamlining end-to-end treasury operations.