AI in Payments: How Artificial Intelligence Is Transforming Digital Payment Processing

7 April, 2026

14 minute read

Nimisha Ghosh, B2B Finance Content Strategist

N

Nimisha Ghosh

Nimisha specializes in Order-to-Cash (O2C) transformation, crafting strategic narratives at the intersection of B2B SaaS and FinTech. With over four years of experience, she brings deep expertise in electronic invoicing, receivables automation, and digital payments, translating complex autonomous finance capabilities into actionable insights for modern finance leaders. When she’s not analyzing trends in enterprise finance, Nimisha enjoys reading and traveling. Her approach to writing is rooted in clarity, precision, and a strong understanding of real-world financial challenges.

Last updated: 11 June, 2026

IDC MarketScape Names HighRadius a Leader in Embedded Payments

Organizations deploying AI in payments are reporting measurable outcomes: fraud losses reduced by up to 45%, processing cycles accelerated by 73%, and DSO shortened by three to ten days in enterprise environments. The global market for artificial intelligence in digital payments is projected to grow from $12.5 billion in 2023 to $45.2 billion by 2028, reflecting the rapid expansion of AI in payment processing across industries.

But the real transformation goes beyond market growth.

The rise of AI in payments marks a structural shift—moving payment operations from reactive transaction handling to predictive, self-optimizing systems. By embedding artificial intelligence in digital payments, organizations can proactively manage fraud risk, improve authorization accuracy, streamline workflows, and enhance liquidity outcomes. In practice, AI in payment processing is redefining how both B2C and B2B enterprises drive efficiency, control risk, and deliver faster, smarter financial performance..

Table of Contents

What Is AI in Payments?

Types of AI-led Digital Payments

Real-World Use Cases of AI in Payment Processing

Impact of Artificial Intelligence on Digital Payments

Emerging Trends in AI-Powered Digital Payments

Limitations & Challenges of AI in Payments

The Future of AI in Payment Processing

How HighRadius Is Leading the AI-in-Payments Revolution

What Is AI in Payments?

AI in payments is the use of artificial intelligence technologies, including machine learning, predictive analytics, natural language processing (NLP), and autonomous software agents, to analyze transaction data, make real-time decisions, and optimize payment processing workflows. In digital payment processing, AI reduces human errors and operational costs while improving approval rates.

Transform B2B Payments into a Strategic Cost Advantage

Recover up to 30% in interchange fees, reduce transaction costs, and ensure secure, compliant global payment processing.

Traditional rule-based systems follow a set of predefined rules, while AI-powered payment processing systems learn from historical data to predict outcomes, detect anomalies, and continuously improve performance without constant human intervention. At its core, AI transforms payments from a reactive processing function into a predictive, self-optimizing decision engine.

AI in B2C vs B2B Payments: Key Differences

While the underlying technologies remain the same, the role of AI looks significantly different depending on whether it is deployed in B2C or B2B environments. The core distinction between the two is:

In B2C environments, AI optimizes transactions.

In B2B environments, AI orchestrates and optimizes entire financial workflows.

The distinction between the two different environments is critical. Consumer payment AI focuses on real-time authorization speed and fraud mitigation. Enterprise AI in payment processing must integrate deeply with accounting systems, compliance frameworks, treasury strategy, and cross-border payment infrastructure.

As adoption matures, AI in B2B payments is evolving beyond isolated automation tools into interconnected autonomous agents capable of managing the end-to-end payment lifecycle.

Types of AI-led Digital Payments

AI in payments is not a single technology but a combination of intelligent models working together to automate, optimize, and secure payment workflows. The most impactful AI technologies in modern payment processing include:

Machine Learning (ML) - Machine learning analyzes historical transaction data to identify patterns, detect anomalies, classify risk levels, and predict future payment behavior. Payments generate large volumes of structured data. ML enables systems to move beyond static rules and adapt to evolving transaction patterns, reducing false declines while strengthening fraud prevention. In enterprise environments, ML models also forecast customer payment timing, assess counterparty risk, and improve cash flow predictability across large account portfolios.

Examples - Fraud detection, Authorization optimization, Risk scoring, Payment behavior prediction, and Chargeback probability modeling.

Natural Language Processing (NLP) - NLP enables systems to read, interpret, and extract meaning from unstructured text such as invoices, contracts, remittance advice, and email communications. A significant portion of payment-related data exists in unstructured formats. NLP reduces manual data entry, accelerates reconciliation, and minimizes processing errors. In B2B ecosystems, where invoices and remittance formats vary widely across vendors and geographies, NLP becomes critical for scaling reconciliation and exception handling.

Examples - Invoice data extraction, remittance matching, contract and payment term interpretation, dispute and query classification.

Robotic Process Automation (RPA) - RPA automates repetitive, rule-based tasks by mimicking human actions across systems. RPA eliminates manual workload and reduces operational bottlenecks in high-volume payment processes. When integrated with AI models, RPA supports straight-through processing in complex, multi-system enterprise payment environments.

Examples - Data entry, Payment posting, Reconciliation workflows, and Exception routing.

Predictive Analytics - Predictive analytics uses historical and real-time data to forecast future outcomes, such as payment timing, risk exposure, or liquidity positions. Because payments directly impact liquidity, predictive insights allow organizations to plan more accurately and reduce financial uncertainty. In enterprise settings, predictive models improve treasury planning and working capital optimization across large, global customer bases.

Examples - Cash flow forecasting, DSO prediction, Payment default probability, and working capital modeling.

Generative AI - Generative AI creates contextual outputs such as summaries, payment explanations, anomaly reports, and financial insights. It accelerates decision-making by transforming complex transaction data into actionable insights. In enterprise finance teams, generative AI supports faster resolution of disputes, clearer reporting to stakeholders, and improved audit documentation.

Examples - Exception summaries, Dispute communication drafts, Financial reporting, and Payment trend analysis.

Agentic AI - Agentic AI systems act autonomously, making decisions, triggering workflows, and optimizing outcomes without constant human oversight. Agentic AI shifts payment systems from automation to orchestration, coordinating decisions across multiple systems and continuously learning from outcomes. In complex enterprise environments, autonomous agents can manage end-to-end payment lifecycles, integrating with ERPs, treasury systems, banks, and compliance frameworks.

Together, these AI technologies move payment systems from static rule-based processing to adaptive, self-learning, and increasingly autonomous financial orchestration.

Justify Payments Automation with Real Business Outcomes

Reduce processing costs, eliminate manual reconciliation, and build a compelling business case for automation investment.

AI in payment processing delivers value when it is embedded into day-to-day financial operations. Across both B2C and B2B environments, intelligent models are transforming how transactions are authorized, routed, reconciled, and secured.

1. Fraud Detection and Anomaly Prevention

Machine learning models analyze transaction behavior in real time to detect anomalies, flag suspicious activity, and prevent fraud before settlement.

In consumer environments, this reduces card fraud and chargebacks.

In enterprise ecosystems, AI identifies invoice fraud, business email compromise (BEC), duplicate payments, and vendor risk patterns.

By learning from evolving behavioral signals rather than relying solely on static rules, AI reduces false positives while strengthening fraud defenses.

2. Intelligent Payment Routing

AI dynamically selects the most cost-effective and reliable payment rail based on transaction size, geography, currency, approval probability, and fee structures. This results in lower cost of acceptance and higher payment success rates.

In B2C payments, this improves authorization rates and reduces checkout friction.

In B2B payments, it optimizes interchange fees, cross-border FX costs, and settlement timing.

3. Automated Reconciliation and Cash Application

Reconciliation remains one of the most manual processes in finance. AI models use pattern recognition and NLP to match remittances to invoices, interpret unstructured payment references, and auto-apply cash across accounts. In high-volume B2B environments, this reduces unapplied cash, accelerates closing cycles, and improves DSO performance.

4. Predictive Payment Timing and Working Capital Optimization

AI analyzes historical payment behavior, credit risk signals, and macro patterns to predict when customers are likely to pay. This enables finance teams to forecast cash flow more accurately, prioritize collections strategically, and manage liquidity with greater precision.

5. Dynamic Fee Optimization and Surcharge Management

In complex payment ecosystems, fee structures vary across processors, card networks, geographies, and transaction types. AI evaluates interchange categories, routing paths, and surcharge rules in real time to minimize processing costs while remaining compliant with regional regulations. This is especially impactful in large B2B transactions where marginal fee differences materially affect profitability.

6. Dispute and Exception Resolution

Generative AI and NLP systems summarize disputes, classify exception types, draft responses, and provide contextual explanations to stakeholders. Instead of manually reviewing transaction histories, finance teams receive structured summaries and recommended actions, accelerating resolution timelines and improving audit traceability.

Case Studies

Konica Minolta's B2B Payments Transformation

Learn how a manufacturing leader unlocked $30Mn in working capital by transforming its payments process.

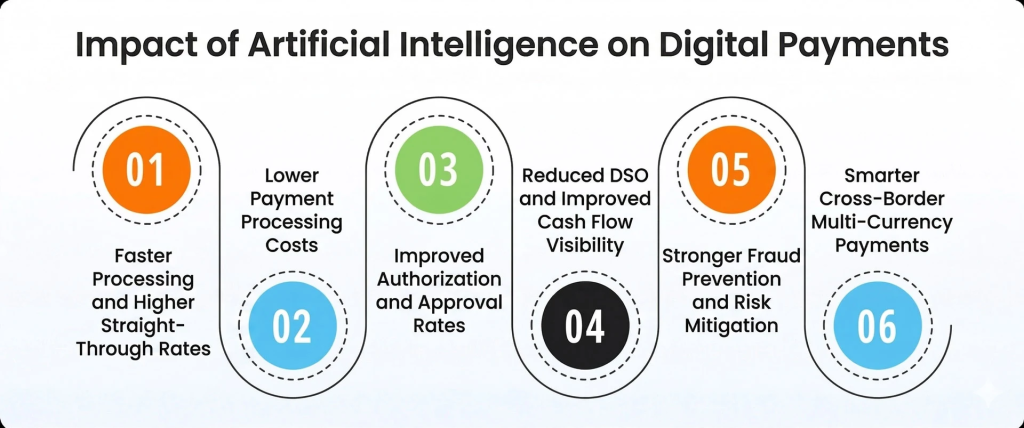

Impact of Artificial Intelligence on Digital Payments

Artificial intelligence is fundamentally reshaping digital payment infrastructure, not only by automating tasks but by improving financial performance, operational efficiency, and strategic decision-making. The impact is measurable across cost, speed, risk, and liquidity.

1. Faster Processing and Higher Straight-Through Rates - AI enables straight-through processing by automating validation, routing, and reconciliation. This reduces manual touchpoints, accelerates settlement cycles, and shortens payment timelines across both consumer transactions and complex enterprise payment environments.

2. Lower Payment Processing Costs - AI optimizes payment routing, evaluates fee structures, and selects cost-effective rails in real time. Organizations implementing AI-powered B2B payment solutions report reductions in payment acceptance costs of up to 80%, particularly in high-value transactions where interchange and processing fees materially impact margins.

3. Improved Authorization and Approval Rates - Machine learning models distinguish legitimate transactions from fraud more accurately than static rules. This reduces false declines, and businesses report measurable improvement in approval rates, resulting in higher revenue capture without increased risk exposure.

4. Reduced DSO and Improved Cash Flow Visibility - In B2B environments, AI predicts payment timing, prioritizes collections, and improves cash forecasting accuracy. Organizations implementing AI-powered payment solutions have reduced DSO by up to 3–10 days, strengthening liquidity and improving significant working capital efficiency.

5. Stronger Fraud Prevention and Risk Mitigation - AI continuously analyzes transaction behavior, vendor patterns, and anomalies to detect fraud in real time. Adaptive models reduce fraud losses while limiting false positives that disrupt legitimate payments.

6. Smarter Cross-Border and Multi-Currency Payments - AI evaluates FX exposure, settlement paths, and regulatory constraints dynamically. By optimizing speed, cost, and compliance simultaneously, organizations improve efficiency and margin predictability in global payment operations.

Emerging Trends in AI-Powered Digital Payments

Artificial intelligence in digital payments is evolving rapidly. As adoption matures, organizations are moving beyond isolated automation toward interconnected, intelligent financial ecosystems. Several key trends are shaping the next phase of AI-driven payment innovation.

1. Embedded and Invisible Payments

Payments are increasingly embedded directly into ERP, procurement, and e-commerce workflows. AI enables payments to trigger automatically based on contract terms, delivery confirmation, or predefined business rules, reducing manual intervention and shortening payment cycles. The transaction becomes seamless, contextual, and often invisible to end users.

2. Rise of Agentic AI in Finance

The shift from rule-based automation to autonomous decision-making is accelerating. Agentic AI systems do not simply execute tasks. They evaluate conditions, trigger workflows, optimize outcomes, and continuously learn from results. In complex B2B ecosystems, this enables intelligent orchestration across payments, reconciliation, compliance, and treasury functions.

3. Real-Time Payment Rails Powered by AI

With the expansion of real-time payment infrastructures globally, AI is playing a critical role in routing, risk assessment, and liquidity management. Intelligent models evaluate settlement speed, fee structures, and fraud risk dynamically, ensuring that real-time payments remain both fast and secure.

4. Embedded Compliance and Continuous Risk Monitoring

Regulatory complexity continues to increase across geographies. AI-driven systems now run sanctions screening, AML checks, tax validation, and vendor risk assessments continuously within the payment flow rather than as post-processing controls.

5. End-to-End AP and AR Intelligence

AI adoption is expanding beyond payments into full procure-to-pay and order-to-cash cycles. Accounts Payable, Accounts Receivable, treasury, and payments are increasingly interconnected through shared data models and autonomous workflows, thus reducing silos and improving financial visibility across the enterprise.

6. Outcome-Based Pricing Models

As AI generates measurable financial outcomes, pricing models in digital payments are evolving to reflect performance rather than access alone. Instead of traditional subscription-based structures, some providers are aligning fees with quantifiable results such as cost reduction, DSO improvement, or higher approval rates. In certain models, implementation and subscription costs are deferred until predefined performance benchmarks are achieved, aligning vendor incentives with business impact and reducing upfront risk for enterprises.

Limitations & Challengesof AI in Payments

While artificial intelligence is transforming digital payments, implementation is not without complexity. In enterprise environments, especially, AI must operate within regulatory, operational, and data constraints that require careful governance and oversight.

1. Data Quality and Fragmentation

AI models are only as reliable as the data they learn from. In B2B environments, payment data is often fragmented across ERPs, banks, gateways, treasury systems, and legacy infrastructure. Inconsistent formats, incomplete remittance data, and historical inaccuracies can limit model effectiveness. Without structured, unified datasets, even advanced AI systems struggle to deliver optimal predictions.

2. Regulatory and Compliance Constraints

Payments operate within strict regulatory frameworks across jurisdictions. Cross-border transactions introduce AML, KYC, data residency, and reporting requirements. AI systems must remain explainable and auditable, particularly when influencing fraud decisions, payment routing, or credit-related outcomes. Black-box models can create compliance risk if decisions cannot be justified.

3. Model Bias and False Positives

While AI reduces fraud and risk exposure, poorly calibrated models can increase false positives, delay legitimate payments, or create friction in vendor relationships. In high-value B2B environments, unnecessary payment blocks can disrupt supply chains and damage trust. Continuous monitoring and retraining are required to maintain balance between risk prevention and operational efficiency.

4. Integration Complexity

Enterprise payment ecosystems are deeply interconnected. AI must integrate with ERPs, treasury management systems, bank APIs, compliance tools, and reconciliation platforms. Implementation requires orchestration across multiple stakeholders - finance, IT, treasury, compliance, and banking partners.

5. Human Oversight and Governance

Despite advances in automation, AI does not eliminate the need for human judgment. Strategic financial decisions, exception management, regulatory review, and complex dispute resolution still require oversight.

The Future of AI in Payment Processing

Artificial intelligence in payments is still in its optimization phase. Most deployments today focus on improving fraud detection accuracy, reducing processing costs, accelerating reconciliation, and forecasting cash flow more precisely. But the trajectory points toward something far more transformative: autonomous financial orchestration.

As AI models mature, payment systems are increasingly moving from assisting decisions to executing them within predefined guardrails. Instead of merely recommending the most cost-effective routing path, intelligent systems will dynamically select rails, rebalance liquidity, manage FX exposure, and adjust risk thresholds in real time, all without requiring constant human intervention.

Risk management is also evolving. Rather than reacting to fraud signals after they emerge, AI systems will simulate potential attack patterns, anticipate anomalies before funds move, and continuously recalibrate controls based on behavioral shifts.

At a macro level, the most significant change may be structural. Payment systems are transforming from static transaction processors into adaptive decision engines, systems that continuously balance cost, speed, risk, compliance, and liquidity objectives in real time.

In the future, the competitive advantage does not lie in simply adopting AI, but in understanding how to intelligently harness AI for optimal results and implementing them. Organizations that build toward autonomous, self-learning payment infrastructure will gain tighter control over liquidity, lower structural cost, and greater resilience in increasingly complex global markets.

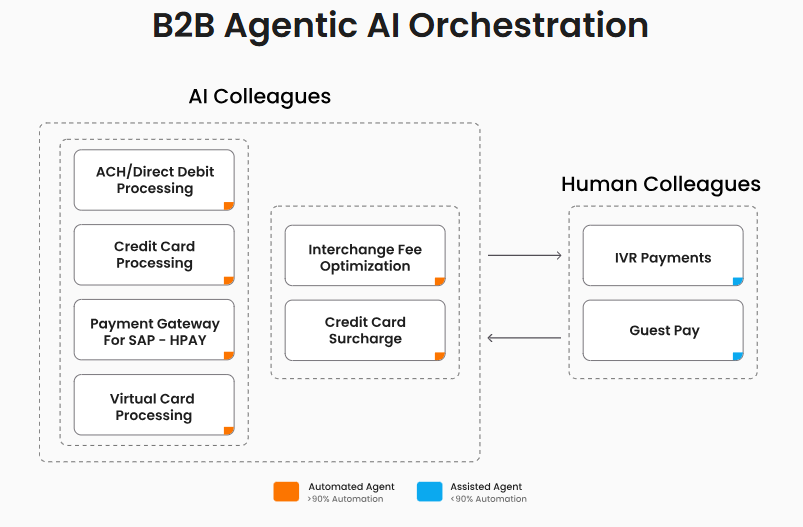

How HighRadius Is Leading the AI-in-Payments Revolution

AI in digital payments is moving businesses from automation to orchestration, but the implementation of AI remains a big challenge. HighRadius addresses this gap with its B2B Payments software. Its AI-powered payment platform is built to reduce acceptance costs, improve cash flow, and optimize payment performance at scale.

Rather than applying AI to isolated steps, HighRadius embeds artificial intelligence across the entire payment lifecycle. The result is measurable: enterprises using its AI-powered payment gateway have reduced payment acceptance costs by up to 80%, cut DSO by 3–10 days, and automated up to 90% of payment workflows, from authorization and remittance capture through to reconciliation and cash application.

Its cross-border capabilities span 100+ payment methods and 150+ currencies, with AI dynamically evaluating FX exposure, settlement paths, regulatory requirements, and local rails to optimize cost, speed, and compliance simultaneously. Across ACH payments, credit cards, virtual cards, and global direct debits, the platform automates up to 90% of payment workflows, connecting authorization, remittance capture, reconciliation, and cash application into a unified, intelligent payment infrastructure.

What sets it apart is not the breadth of features but the depth of integration - payments, AR, ERP, and treasury connected through a fully integrated payment infrastructure rather than a patchwork of tools.

Recognized as a Leader in the IDC MarketScape for Embedded Payment Applications, and now offering outcome-based pricing tied to realized results, HighRadius removes both the implementation risk and the performance uncertainty that typically slow enterprise AI adoption.

Learn More About HighRadius’s B2B Payment Software

Achieve seamless payment processing and cost control with just one click

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.