Month-End Close Process 2026: Steps, Checklist & the Shift to Autonomous Finance

Last Updated: 16 July, 2026

•

Nimisha Ghosh B2B Finance Content Strategist

N

Nimisha Ghosh

Nimisha specializes in Order-to-Cash (O2C) transformation, crafting strategic narratives at the intersection of B2B SaaS and FinTech. With over four years of experience, she brings deep expertise in electronic invoicing, receivables automation, and digital payments, translating complex autonomous finance capabilities into actionable insights for modern finance leaders. When she’s not analyzing trends in enterprise finance, Nimisha enjoys reading and traveling. Her approach to writing is rooted in clarity, precision, and a strong understanding of real-world financial challenges.

Analyst Recognition

HighRadius Named a Challenger in 2026 Gartner® Magic Quadrant™ for Financial Close and Consolidation Solutions

Discover how HighRadius brings practical, results-driven AI to record-to-report processes with automation, anomaly detection, and continuous close capabilities.

For finance teams, the month-end close is one of the most predictable yet demanding parts of the calendar. Every month, the same sequence of tasks needs to happen: transactions recorded, accounts reconciled, statements prepared, all within a fixed window, regardless of how smoothly (or not) the previous month went.

For some teams, this is a routine exercise that wraps up in a few days. For others, it’s a recurring scramble that stretches well into the next month, with errors carrying forward and creating more work down the line.

This guide breaks down what the month-end close process actually involves, why each step matters, the challenges that commonly slow it down, and what separates teams that close quickly and accurately from those that don’t.

Key Takeaways

Month-end close ensures financial records are accurate, complete, and ready for reporting by reconciling transactions, posting adjustments, and preparing financial statements.

A structured close improves compliance, audit readiness, cash flow visibility, forecasting, and decision-making.

Automation and continuous reconciliation help reduce manual effort, accelerate close cycles, and improve reporting accuracy.

What Is The Month-End Close Process?

The month-end close is an accounting process that finance teams run at the end of every calendar month to finalize the period’s financial records. It involves systematically collecting, verifying, and reconciling all transactions that occurred during the month, across bank accounts, accounts receivable, accounts payable, and the general ledger, and using that reconciled data to produce accurate financial statements.

The goal is to ensure that all financial transactions have been accurately recorded and that financial statements reflect the company’s actual financial position for the reporting period.

What Is the Purpose of the Month-End Close Process?

The primary purpose of the month-end close process is to ensure that financial records are accurate, complete, and ready for reporting. A well-executed month-end close gives finance teams and business leaders a reliable, up-to-date view of the company’s financial position, cash flow, liabilities, revenue, and expenses, at a fixed point in time. This becomes the foundation for budgeting decisions, forecasting, audit preparation, and board reporting.

A structured month-end close process helps organizations:

Produce accurate financial statements

Maintain compliance with accounting and regulatory requirements

Identify and correct accounting errors before they impact reporting

Improve visibility into revenue, expenses, profitability, and cash flow

Support budgeting, forecasting, and strategic planning

Simplify quarter-end and year-end reporting activities

Strengthen audit readiness and internal controls

Without it, errors from one month carry into the next, discrepancies compound, and by the time year-end arrives, the clean-up effort is significantly greater than it needed to be. The month-end close, done consistently and accurately, is what keeps the financial record trustworthy throughout the year.

6 Key Steps Involved in the Month-End Close Process

While the exact workflow varies across organizations, most month-end close processes follow a similar sequence of activities. These steps help finance teams verify financial data, reconcile accounts, prepare financial statements, and ensure reporting accuracy before the accounting period is officially closed.

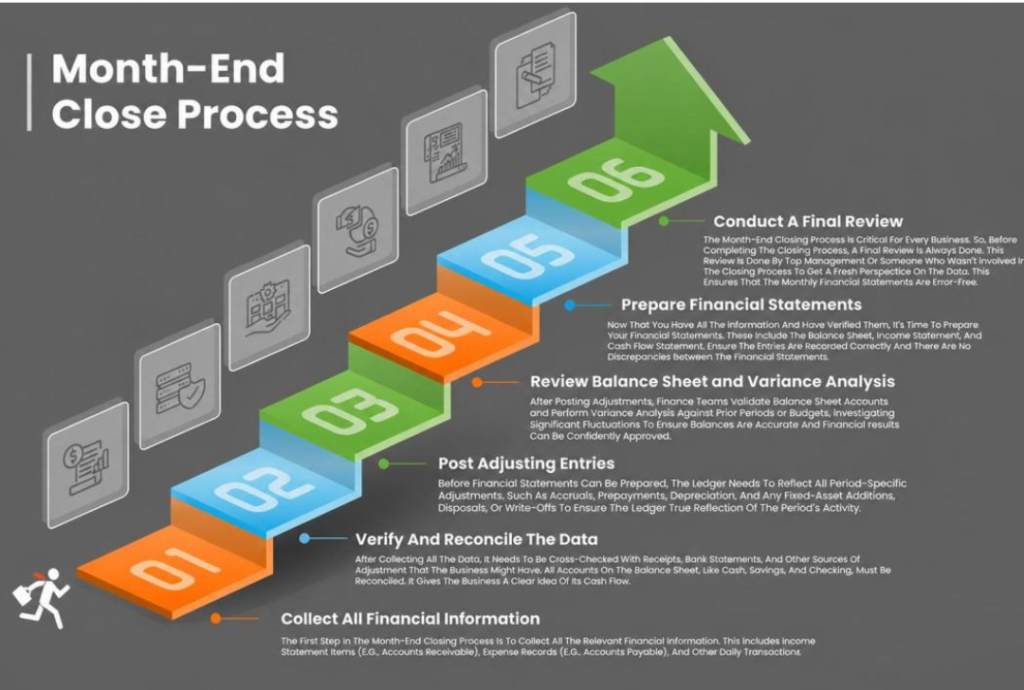

1. Collect all Financial Information

Every close begins with gathering transaction data from across the business, bank accounts, accounts receivable, accounts payable, payroll, expenses, and any other financial activity that occurred during the month. This includes pulling records from ERPs, bank portals, and any other systems where financial data lives.

This step happens to be one of the most crucial because the accuracy of everything that follows depends entirely on the completeness of what’s collected here. If data is missing or pulled from the wrong period, the reconciliations and statements built on top of it will be wrong.

If not done correctly, teams end up closing with incomplete data, discovering gaps mid-process, and having to restart parts of the reconciliation, adding days to the close.

2. Verify and Reconcile the Data

Once data is collected, it needs to be verified and matched. This means comparing internal records against external sources, bank statements against the general ledger, sub-ledgers against control accounts, intercompany transactions between entities. Any discrepancy needs to be investigated and resolved before moving forward.

This is typically the most time-intensive step in the close. It’s where the integrity of the financial record is either confirmed or called into question. If not done correctly, discrepancies go unresolved, financial statements reflect inaccurate balances, and audit risk increases significantly.

3. Post Adjusting Entries

Before financial statements can be prepared, the ledger needs to reflect all period-specific adjustments. This includes accruals for expenses incurred but not yet invoiced, prepayments for costs paid in advance that haven’t been fully used, and, for asset-heavy businesses, depreciation on fixed assets and any additions, disposals, or write-offs that occurred during the month.

These entries are what make financial statements a true reflection of the period’s activity, rather than just a record of what was invoiced or paid. If not done correctly, revenue and expenses are mismatched across periods, depreciation charges are missed or duplicated, and the P&L becomes an unreliable basis for any decision-making.

4. Review Balance Sheet and Variance Analysis

Once adjusting entries are posted, finance teams review the balance sheet to confirm all account balances are accurate, supported, and reconcile correctly across assets, liabilities, and equity.

Alongside this, a variance analysis is run to compare the current period’s numbers against the prior month, prior year, or budget. Any significant movement needs to be understood and explained before the close can be signed off.

This step acts as a quality check before the numbers are locked. It’s where errors that slipped through earlier in the process are most likely to surface, which is why it needs to happen before statements are prepared, not after. If not done correctly, unexplained variances make it into the final statements, and the finance team ends up fielding uncomfortable questions during board or audit reviews.

5. Prepare Financial Statements

With reconciliations complete and adjustments posted, the finance team prepares the core financial statements, the income statement, balance sheet, and cash flow statement. These are reviewed for accuracy, completeness, and consistency before being signed off.

The financial statement is the primary output of the entire close process. Everything up to this point exists to make these statements accurate and trustworthy.

6. Conduct a Final Review

Before the close is officially signed off, a final review is conducted, typically by a Controller or Finance Manager, to catch anything that may have been missed. This includes reviewing journal entries, checking for unusual variances, and ensuring all supporting documentation is in place. This is the last line of defense before the numbers are locked and reported.

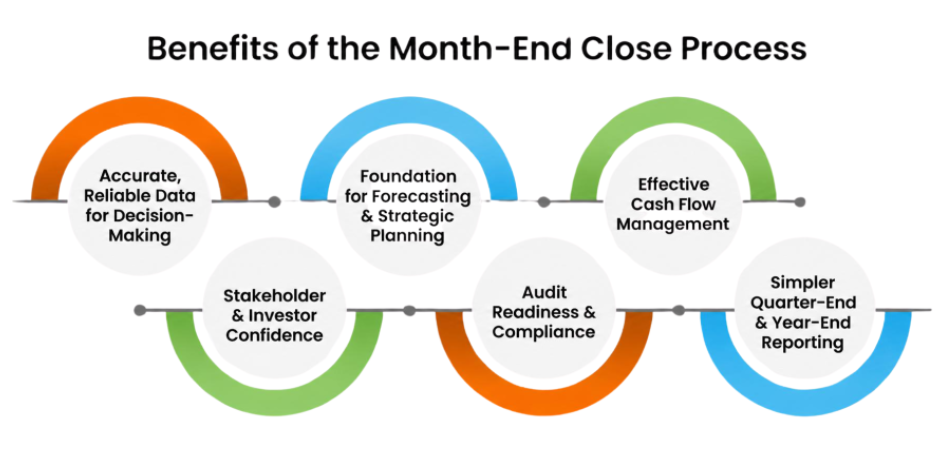

Benefits of the Month-End Close Process

A disciplined month-end close does more than keep the books tidy. It directly shapes the quality of decisions made across the business, from daily operations to long-term strategy.

1. Accurate, Reliable Data for Decision-Making

When every transaction is reconciled and every adjustment posted, leadership works from numbers they can trust. Financial statements reflect reality, not approximations, and that accuracy is what makes business decisions defensible, whether it’s a budget reallocation, a hiring decision, or a capital investment.

2. A Foundation for Forecasting and Strategic Planning

Month-end close produces the historical data that forecasting is built on. Without a clean, consistent record of how the business has actually performed, projections are guesswork. A well-run close gives finance teams the baseline they need to model scenarios, set targets, and plan with confidence.

3. Effective Cash Flow Management

Closing the books monthly gives the business a regular, accurate picture of its cash position, what’s coming in, what’s going out, and where liquidity is tight. This visibility is what allows finance teams to manage obligations proactively rather than reactively.

4. Stakeholder and Investor Confidence

Investors, lenders, and board members rely on financial statements to assess the health of the business. Consistent, accurate monthly reporting signals that the finance function is in control, which matters during fundraising, credit applications, and any external scrutiny of the business.

5. Audit Readiness and Compliance

A structured month-end close means documentation is current, reconciliations are complete, and supporting records exist for every material entry. When an audit arrives, internal or external, there’s nothing to scramble for. The work has already been done.

6. Simpler Quarter-End and Year-End Reporting

Organizations that maintain accurate financial records throughout the year spend less time correcting errors, chasing documentation, and resolving discrepancies during quarter-end and year-end close periods. Instead of treating reporting as a large, once-a-year exercise, they maintain the integrity of their financial data month by month, so quarter-end and year-end become a consolidation of clean records, not a cleanup operation.

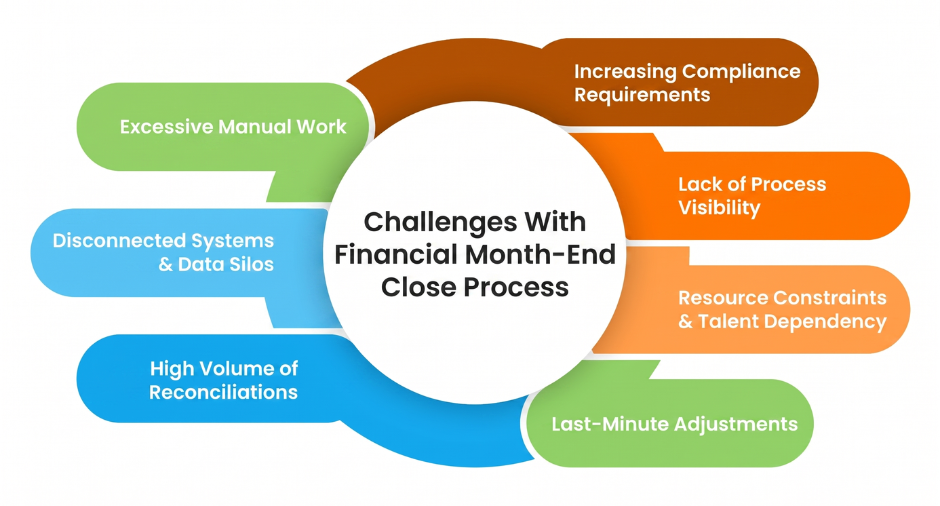

Challenges With Financial Month-End Close Process

For most finance teams, the month-end close is one of the most demanding recurring activities of the calendar. The pressure is structural, a hard deadline, a high volume of tasks, and consequences for getting it wrong. These are the challenges that make it difficult.

1. Excessive Manual Work

A significant portion of the month-end close still runs on manual effort, data entry, copy-pasting between systems, formatting spreadsheets, chasing approvals over email. Each manual touchpoint is a potential error, and the cumulative effect across an entire close cycle is substantial. Teams spend time on repetitive tasks that add no analytical value, leaving less bandwidth for the work that actually requires human judgment.

2. Disconnected Systems and Data Silos

Most finance teams don’t work out of a single system. Data lives across multiple ERPs, bank portals, subsidiary ledgers, and spreadsheets, often with no automated connection between them. Pulling it together at month-end means manual exports, file transfers, and reconciling records that were never designed to talk to each other. Every handoff between systems is an opportunity for data to be lost, duplicated, or mismatched.

3. High Volume of Reconciliations

The sheer number of accounts, transactions, and entities that need to be reconciled each month is one of the most consistent bottlenecks in the close. For organizations operating across multiple legal entities, currencies, or business units, the volume compounds quickly. Even well-organized teams can find themselves buried in reconciliation work that stretches across the entire close window.

4. Last-Minute Adjustments

Accrual data, vendor invoices, and intercompany entries frequently arrive late, sometimes days into the close cycle. These late-arriving items force teams to reopen reconciliations they’ve already completed, post adjustments at the eleventh hour, and recheck statements that were nearly finalized. The result is a close that never really has a clean finishing line.

5. Lack of Process Visibility

In many organizations, there’s no single place to see the status of the close in real time. Task ownership is unclear, progress is tracked in spreadsheets or communicated over email, and managers spend time chasing updates rather than reviewing work. When something slips, it’s often discovered too late to fix without impacting the close date.

6. Resource Constraints and Talent Dependency

Month-end close is time-intensive, and most finance teams are lean. The workload is concentrated into a short window, creating pressure that is difficult to absorb without errors or overtime. Compounding this, close processes often depend heavily on a small number of experienced team members who know the nuances of the company’s systems and entries. When those people are unavailable, due to leave, turnover, or competing priorities, the close is immediately at risk.

7. Increasing Compliance Requirements

Regulatory and reporting requirements continue to evolve. New accounting standards, audit requirements, and internal controls add steps to an already demanding process. For organizations operating across multiple jurisdictions, compliance complexity multiplies, and keeping up with it while maintaining close speed is a growing challenge for finance teams.

Why Does Month-End Close Still Take So Long?

Uncover the hidden bottlenecks, process gaps, and manual dependencies that delay financial close and keep finance teams stuck in firefighting mode.

Best Practices For Improving the Month-End Close Process

A faster, more accurate close isn’t about working harder during the last week of the month. It’s about how the process is designed and maintained throughout the month. These practices separate finance teams that consistently close on time from those that don’t.

1. Standardize Every Step of the Close

Ad hoc processes don’t scale. Finance teams that close consistently well operate from a defined playbook, documented workflows, assigned owners, and a checklist that follows the same sequence every month. Standardization removes ambiguity, reduces the risk of steps being missed, and makes onboarding new team members significantly easier.

2. Start Earlier Than You Think You Need To

Most close delays are caused by work that could have been done before the period ended. Reconciling high-volume accounts continuously throughout the month, rather than waiting until day one of the close, means the bulk of the work is already done when the period closes. The close becomes a verification exercise rather than a scramble.

3. Establish Clear Ownership and Deadlines

Every task in the close should have a named owner and a due date. When ownership is ambiguous, tasks fall through the cracks, and managers spend time chasing updates instead of reviewing work. A simple task tracker, even a well-maintained spreadsheet, is significantly better than no system at all.

4. Build In a Review Layer Before Final Sign-Off

Errors found during the close are far cheaper to fix than errors found after. Building a structured review step, where a senior team member checks reconciliations and journal entries before statements are prepared, catches the majority of issues while there’s still time to correct them cleanly.

5. Treat Every Close as an Opportunity to Improve the Next One

After each close, take fifteen minutes to document what caused delays, what required rework, and what went smoothly. Over time, this creates a clear picture of where the process has systemic weaknesses, and gives the team a concrete basis for making each close incrementally better than the last.

Ebooks

Build a More Accurate Month-End Close

A practical look at the habits, controls, and workflows that help finance teams improve close accuracy month after month

A month-end close checklist is a structured list of tasks that finance teams work through before the accounting period is officially closed. It ensures nothing is missed, creates accountability across the team, and gives everyone involved a clear picture of where the close stands at any given point.

The most effective checklists follow the same sequence as the close itself, tasks are ordered the way they actually need to be executed, not grouped arbitrarily. For example, recording bank transactions should always appear before reconciling bank accounts. The sequence matters because each step builds on the one before it. Here are the core tasks that a month-end close checklist should cover:

1. Record All Transactions – Ensure all transactions across bank accounts, accounts receivable, accounts payable, and credit cards are accurately recorded for the period. This is the foundation on which everything else is built on.

2. Post Month-End Journal Entries – Record all necessary adjustments – prepaid expenses, accrued expenses, accrued payroll, depreciation, and any other period-specific entries that need to be posted before the close.

3. Reconcile Bank Accounts and Credit Cards – Compare all bank and credit card transactions against their respective statements. Identify and resolve any discrepancies before moving forward.

4. Reconcile Sub-Ledgers to the General Ledger – Ensure accounts receivable, accounts payable, and other sub-ledgers are in agreement with the general ledger. Any mismatches need to be investigated and corrected.

5. Review Balance Sheet Accounts – Check that all balance sheet accounts are accurate, supported by documentation, and reconciled. Flag any unusual or unexplained balances for investigation.

6. Prepare and Review Financial Statements – Prepare the income statement, balance sheet, and cash flow statement. Review for completeness, accuracy, and consistency before sign-off.

7. Conduct Variance Analysis – Compare current period results against prior month, prior year, and budget. Document explanations for any significant variances.

8. Produce Internal Management Reports – Finalize reporting packages for leadership and stakeholders, providing a clear and accurate view of the company’s financial performance for the period.

9. Archive and Document – Ensure all workpapers, reconciliations, journal entries, and supporting documentation are saved, organized, and accessible, both for internal review and audit purposes.

Templates

The Blueprint for a Smoother Month-End Close

See how leading finance teams bring structure and accountability to month-end close with a proven checklist template.

A month-end close checklist does more than keep the close organized. It creates a repeatable process that the entire team can follow consistently, regardless of who is doing the work. Over time, a well-maintained checklist becomes a living record of how the close actually runs, making it easier to identify bottlenecks, onboard new team members, and improve the process with each passing month.

For finance teams managing multiple entities, tight deadlines, or lean resources, a month-end close checklist is one of the simplest and most effective tools available. It doesn’t eliminate every challenge in the close, but it ensures that the right work gets done in the right order, every single time.

The Shift to Autonomous Finance

The month-end close has traditionally been a manual and largely reactive process. Finance teams wait for the accounting period to end, gather data from multiple systems, work through reconciliations under tight deadlines, and resolve issues as they surface. This approach has been the default for decades, largely because the tools available didn’t offer much of an alternative.

That’s changing. A growing number of finance teams are shifting toward what’s often called autonomous finance, where systems continuously ingest and reconcile data throughout the month, flag anomalies as they occur, and prepare much of the groundwork for the close before the period even ends. Instead of the close being a distinct, high-pressure event, it becomes the final step of a process that’s been running continuously.

This shift doesn’t happen all at once, and it doesn’t mean removing finance teams from the process. What it changes is where their time and judgment get applied, away from manual data-gathering and routine matching, and toward reviewing exceptions, investigating genuine anomalies, and analyzing what the numbers mean for the business.

At its core, autonomous finance shifts close activities from a periodic exercise to a continuous process. Tasks that were historically concentrated into a few days at month-end begin happening throughout the accounting period, reducing the workload that accumulates during close and improving visibility into financial data.

What This Shift Looks Like in Practice

Close Activity

The Traditional Approach

The Autonomous Approach

Recording Transactions

Data is manually pulled from multiple systems at the start of the close, often with a lag

Data is continuously synced from source systems throughout the month

Reconciliations

Accounts are matched manually, line by line, once the close begins

Most matching happens automatically and continuously; teams review only exceptions

Journal Entries

Accruals and adjustments are calculated and entered manually each month

Recurring entries are generated automatically and routed for review

Variance Analysis

Variances are identified and investigated after statements are drafted

Anomalies are flagged in real time as they occur, before they reach the statements

Close Management

Progress tracked through spreadsheets, emails, and status meetings

Centralized workflows provide real-time visibility into task ownership, status, and bottlenecks

Reporting

Reports are compiled manually, often in spreadsheets, close to the deadline

Reports are generated directly from reconciled, continuously updated data

For finance teams managing high transaction volumes, multiple entities, or increasingly complex reporting requirements, this shift represents more than a technology upgrade. It fundamentally changes how the close is managed, reducing time spent on administrative work and allowing finance professionals to focus on analysis, controls, forecasting, and strategic decision-making.

Ebooks

Unlock the Potential of Close Automation

Discover practical use cases that show how automation streamlines complex close activities and eliminates manual bottlenecks.

How HighRadius Helps Finance Teams Run a Faster, More Accurate Close

The shift toward autonomous finance described above isn’t theoretical; it’s the foundation on which HighRadius’s Record-to-Report suite is built on. Rather than addressing the close as a single end-of-month event, HighRadius connects each part of the process, reconciliation, matching, journal entries, and reporting, into one continuously running system, so the close becomes a final check rather than a sprint.

Reconciliation is typically where most of the close’s manual effort concentrates, so it’s where automation makes the most immediate difference. HighRadius’s Account Reconciliation software continuously matches high-volume accounts throughout the month, flags only genuine exceptions for review, and maintains a running audit trail, which means by the time the period closes, most reconciliations are already done rather than just beginning. For finance teams dealing with large transaction volumes across multiple systems, Transaction Matching software extends this further, comparing transactions far faster than manual line-by-line review and surfacing only the discrepancies that actually need human attention.

The same continuous approach applies to journal entries, one of the most common sources of late-cycle corrections. Journal Entry Automation generates and validates recurring and accrual-based entries automatically, routing them for approval well before the close window opens, reducing both the manual workload and the risk of errors carrying into financial statements.

Bringing all of this together, Financial Close Software gives finance teams a single, real-time view of where the close stands, task ownership, status, and dependencies, all visible in one place. This is what directly addresses the visibility gap that makes the close stressful for so many teams: instead of chasing updates across spreadsheets and email, managers can see exactly what’s done, what’s pending, and what needs attention.

The result of connecting these pieces is a close that looks fundamentally different in practice. Reconciliation work that used to consume the first week of the month happens continuously instead; journal entries are largely prepared and reviewed before the close even begins, and the final days are spent on genuine analysis rather than data wrangling. For finance teams managing multiple entities, high transaction volumes, or lean headcount, this isn’t just faster, it’s a close that’s more accurate, less stressful, and far easier to stand behind when questions come from leadership or auditors.

Take a deep dive into HighRadius’ R2R solutions

Getting granular visibility and control into your accounting process is just a click away.

Achieve up to 90% transaction auto-match with out-of-the-box matching rules

Financial Close Management

Reduce days to close by 30% with a detailed checklist for month-end close

Anomaly Management

Resolve 80% of anomalies with auto-suggested actions.

Frequently Asked Questions (FAQs)

1. What are month-end reports?

Month-end reporting involves preparing and analyzing financial reports at the end of each month to summarize a company’s financial performance. It includes reviewing financial statements, such as income statements, balance sheets, and cash flow statements, and identifying key performance indicators.

Month-end reporting involves preparing and analyzing financial reports at the end of each month to summarize a company’s financial performance. It includes reviewing financial statements, such as income statements, balance sheets, and cash flow statements, and identifying key performance indicators.

2. What is the month-end close policy?

It is the process of reviewing, reconciling, and verifying that all financial transactions and aspects of the company’s ledgers from the past fiscal year add up. This involves calculating the business expenses, income, revenue, assets, investments, equity, and more.

It is the process of reviewing, reconciling, and verifying that all financial transactions and aspects of the company’s ledgers from the past fiscal year add up. This involves calculating the business expenses, income, revenue, assets, investments, equity, and more.

3. What does the month-end close process look like?

The month-end close process involves recording, reconciling, and reviewing all financial transactions to ensure accuracy. It includes steps like recording journal entries, reconciling accounts, reviewing transactions, generating financial statements, making adjusting entries, analyzing variances, ensuring compliance, and preparing reports.

The month-end close process involves recording, reconciling, and reviewing all financial transactions to ensure accuracy. It includes steps like recording journal entries, reconciling accounts, reviewing transactions, generating financial statements, making adjusting entries, analyzing variances, ensuring compliance, and preparing reports.

4. How often should you review your month-end close process?

You should review your month-end close process quarterly or biannually to ensure it stays efficient and aligned with evolving business needs. Regular updates to your accounting monthly close process help identify bottlenecks and optimize month-end regulatory accounting ethics.

You should review your month-end close process quarterly or biannually to ensure it stays efficient and aligned with evolving business needs. Regular updates to your accounting monthly close process help identify bottlenecks and optimize month-end regulatory accounting ethics.

5. Why is a month-end close checklist important?

A month-end close checklist helps keep financial tasks organized and accurate. It makes sure nothing is missed, speeds up the close, cuts down errors, and gives managers clear reports for better decisions.

A month-end close checklist helps keep financial tasks organized and accurate. It makes sure nothing is missed, speeds up the close, cuts down errors, and gives managers clear reports for better decisions.

6. What should be included in a month-end close checklist?

A month-end close checklist lists the key tasks to wrap up your books each month. It usually includes:

Record all transactions (bank, A/R, A/P, credit cards)

Post journal entries for accruals, payroll, depreciation, etc.

Reconcile bank, credit card, and other account balances

Update workpapers to support account balances

Review reports like Balance Sheet, Income Statement, and Cash Flow

Prepare a simple management report for stakeholders

A month-end close checklist lists the key tasks to wrap up your books each month. It usually includes:

Record all transactions (bank, A/R, A/P, credit cards)

Post journal entries for accruals, payroll, depreciation, etc.

Reconcile bank, credit card, and other account balances

Update workpapers to support account balances

Review reports like Balance Sheet, Income Statement, and Cash Flow

Prepare a simple management report for stakeholders

7. How long should a typical month-end close take?

A typical close takes 5 to 10 days. Leading organizations aim for a “Fast Close” of under 5 days by automating data collection and reconciliations to eliminate manual bottlenecks and accelerate financial reporting.

A typical close takes 5 to 10 days. Leading organizations aim for a “Fast Close” of under 5 days by automating data collection and reconciliations to eliminate manual bottlenecks and accelerate financial reporting.

8. What are the most common month-end closing errors?

Common pitfalls include manual data entry errors, missed accruals, and reconciliation discrepancies. These typically occur when teams rely on disconnected spreadsheets rather than a centralized, automated financial system that ensures data integrity.

Common pitfalls include manual data entry errors, missed accruals, and reconciliation discrepancies. These typically occur when teams rely on disconnected spreadsheets rather than a centralized, automated financial system that ensures data integrity.

Resource Library

Resource Hub

ASSETS

Cash Flow Calculator (FREE)

Track operating and net cash flow while forecasting balances to maintain liquidity and financial control.

HighRadius Named a Challenger In 2025 Gartner® Magic Quadrant™ for Financial Close and Consolidation Solutions

HighRadius stands out as a challenger by delivering practical, results-driven AI for Record-to-Report (R2R) processes. With 200+ LiveCube agents automating over 60% of close tasks and real-time anomaly detection powered by 15+ ML models, it delivers continuous close and guaranteed outcomes—cutting through the AI hype. On track for 90% automation by 2027, HighRadius is driving toward full finance autonomy.

HighRadius Named ‘Rising Star’ in 2024 ISG Provider Lens™ Finance and Accounting Platforms Report

HighRadius leverages advanced AI to detect financial anomalies with over 95% accuracy across $10.3T in annual transactions. With 7 AI patents, 20+ use cases, FreedaGPT, and LiveCube, it simplifies complex analysis through intuitive prompts. Backed by 2,700+ successful finance transformations and a robust partner ecosystem, HighRadius delivers rapid ROI and seamless ERP and R2R integration—powering the future of intelligent finance.

HighRadius Named As A Major Player For Treasury & Risk Management Software By IDC

HighRadius is redefining treasury with AI-driven tools like LiveCube for predictive forecasting and no-code scenario building. Its Cash Management module automates bank integration, global visibility, cash positioning, target balances, and reconciliation—streamlining end-to-end treasury operations.