Credit Management Guide: Everything You Need to Know

11 December, 2019

11 minute read

Soumi Sarkar, Fintech content strategist

S

Soumi Sarkar

Soumi specializes in O2C, finance, and accounting transformation with a focus on bringing a domain-led perspective to accounting, finance and order-to-cash transformation. She crafts insight-driven, CFO-aligned content that helps finance teams optimize operational workflows and drive measurable outcomes. Beyond her professional work, Soumi is a published author of two books, a poetess, an avid reader, and a storyteller who enjoys exploring narratives across both B2B and creative formats.

Last updated: 13 July, 2026

Incomplete Credit Data = Higher Default Risk. Here's How Automation Improves Credit Limit Decisions And Credit Scoring

Credit management is no longer a back-office function. It directly impacts revenue, cash flow, and risk exposure. As businesses scale, extending credit becomes necessary to stay competitive, but without structured processes, it can quickly lead to delayed payments and bad debt.

Most organizations don’t struggle with defining credit policies. They struggle with executing them consistently. Disconnected systems, manual reviews, and limited visibility into customer risk slow down decisions and create avoidable exposure.

This guide breaks down how credit management works, where traditional processes fail, and what modern, data-driven credit management solutions like credit score software and credit decision tools look like.

Table of Contents

What Is Credit Management?

Where Credit Management Breaks Down

Benefits of Automated Credit Management Process

Steps Involved in the Credit Management Process

What Modern Credit Management Looks Like

Key Challenges Encountered in Credit Management Process

Why Businesses Are Moving Toward Automated Credit Management

How Does an Autonomous Credit Management Process Work and What Does It Look Like?

How The Right Credit Management Solution Transforms Businesses

How HighRadius Credit Management Solution Helps Accelerate Credit Decisioning

What Is Credit Management?

Credit management is the process of evaluating customer creditworthiness, setting credit limits, defining payment terms, and monitoring risk to ensure timely payments. It helps businesses balance revenue growth with risk control and directly impacts cash flow and bad debt.

Bad Credit Decisions Don’t Start at Collections—They Start at Workflow Gaps.

See how structured credit workflows reduce bad debt by up to 30% and improve cash flow predictability.

The supplier’s credit team typically assesses the buyer’s creditworthiness by reviewing various factors, such as their credit history, financial statements, and payment behavior. They then make a decision on whether to grant credit and, if so, what credit limit to set. Effective trade credit management can help businesses reduce the risk of non-payment and improve their cash flow.

The best way to improve credit management is to automate the process using tools like credit score ai software and credit decision tools. They not only improve credit risk monitoring continuously evaluates customer exposure, payment behavior, and external risk signals. For example, when a new customer places an order or requests a limit increase, the credit decision engine instantly determines whether the request can be approved, requires escalation, or should be declined, ensuring faster onboarding, controlled risk, and full auditability at scale.

Ebooks

Manual Credit Reviews Are Driving Up Costs—Automation Can Cut Them by 20%+.

Reduce operational overhead while improving speed, accuracy, and decision consistency.

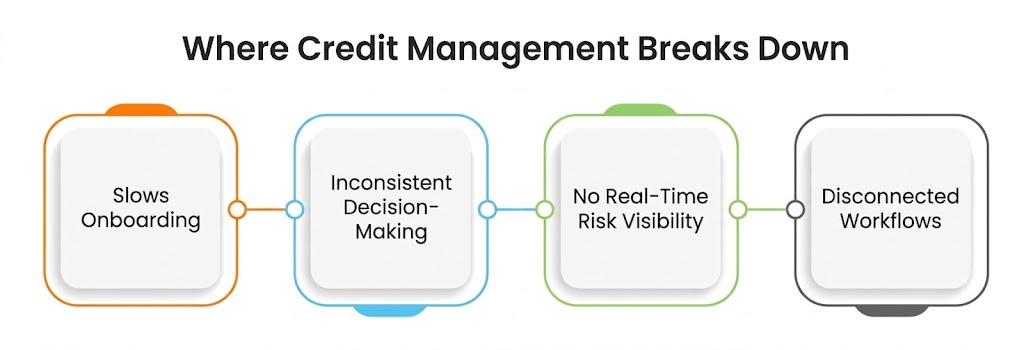

Most credit management challenges don’t come from a lack of policy. They come from inconsistent execution. On paper, credit frameworks look solid. In practice, gaps in data, process, and coordination slow decisions and increase risk exposure.

– Manual Data Collection Slows Onboarding

Teams still depend on emails, PDFs, and spreadsheets to gather customer information. This creates delays, repeated follow-ups, and incomplete applications, making it difficult to move from request to decision quickly. As volumes grow, this manual effort becomes a bottleneck for both finance and sales, especially when there is no structured credit application process in place.

– Inconsistent Decision-Making

Without standardized evaluation frameworks, credit decisions vary across analysts, regions, or business units. Similar customers can receive different credit limits or terms, leading to uneven risk exposure and lack of control at a portfolio level. This is where structured credit decision making frameworks become critical to ensure consistency across the organization.

– No Real-Time Risk Visibility

Credit decisions are often based on static financial statements or outdated credit reports. Without continuous monitoring of customer behavior and external signals, businesses remain exposed to sudden changes in risk, only reacting after payments are delayed. Modern approaches like AI in credit risk scoring help address this gap by enabling real-time, data-driven risk assessment.

– Disconnected Workflows

Credit, sales, and collections teams operate in silos, using different systems and datasets. This lack of coordination leads to misaligned decisions, credit may approve accounts without full visibility, while collections deals with the downstream impact of poor upfront screening. Integrating insights from credit scoring models and aligning workflows across teams is essential to avoid these breakdowns.

Benefits of Automated Credit Management Process

Faster Customer On-boarding: By automating credit management, customer onboarding becomes faster and more efficient. Automation streamlines the credit evaluation process, eliminating manual data entry and processing, and automatically extracting data from online credit applications, financial statements, and credit bureaus. This reduction in time required to gather and evaluate information enables a seamless and swift customer onboarding experience.

Eliminate Inaccurate Manual Credit Scoring: With the help of existing credit data (gathered through the application forms) and pre-written models and algorithms configured with various industry-specific best practices, the risk scores, risk categories, and credit limits can be automatically assigned.

Standardized Credit Management: Establishing a structural workflow for credit risk management will help ensure that all the critical credit decisions are approved through a proper hierarchical channel.

Lower Bad Debts: By establishing a transparent and visible system and introducing reports and analytics, the C-Suite can keep a track of the entire process as well as monitor the status of credit risk. Real-time risk monitoring can help identify risks of bankruptcy, a downgrade of payment ratings, and other news that can help in proper decision-making to ensure lower bad debts.

Steps Involved in the Credit Management Process

Effective credit management is a comprehensive process that includes a few key steps aimed at assessing credit risk, setting credit limits, and monitoring payment behavior. Based on the 5Cs of credit (capacity, capital, conditions, character, and collateral), the key steps involved in the credit management process are as follows:

Step 1: Review the customer’s credit application

The first step in the credit management process involves reviewing new customers’ credit applications to gather detailed business information, credit references, billing and shipping information, and more. The credit application acts as a consolidated record. Existing customers may not require this step.

Step 2: Review the customer’s financial health

Credit teams download reports from credit agencies to analyze the customer’s credit ratings and payment scores. They also review public financial statements, such as cash flow statements, profit and loss statements, and balance sheets, to assess the customer’s financial health. For existing customers, credit teams review the payment behavior along with 3rd party credit ratings and financials.

Step 3: Ask for credit references

Credit teams request credit references, such as bank and trade references, to verify the buyer’s financial position and creditworthiness.

Step 4: Calculate the credit score and limit

Credit teams use sophisticated risk models to quantify the customer’s creditworthiness. These risk models are customized to the industry and the credit policy followed by the organization. Various parameters are used in these risk models, and they have different weightages across organizations.

What Modern Credit Management Looks Like

Credit management is shifting from manual reviews to a data-driven, automated model. Instead of relying on static reports and analyst judgment, modern systems use real-time data, predefined policies, and AI-driven scoring to evaluate risk consistently.

This shift enables:

Faster credit approvals

Standardized decision-making

Continuous monitoring of customer risk

Over the last decade, credit management has evolved from a reactive function to a strategic driver of cash flow and growth

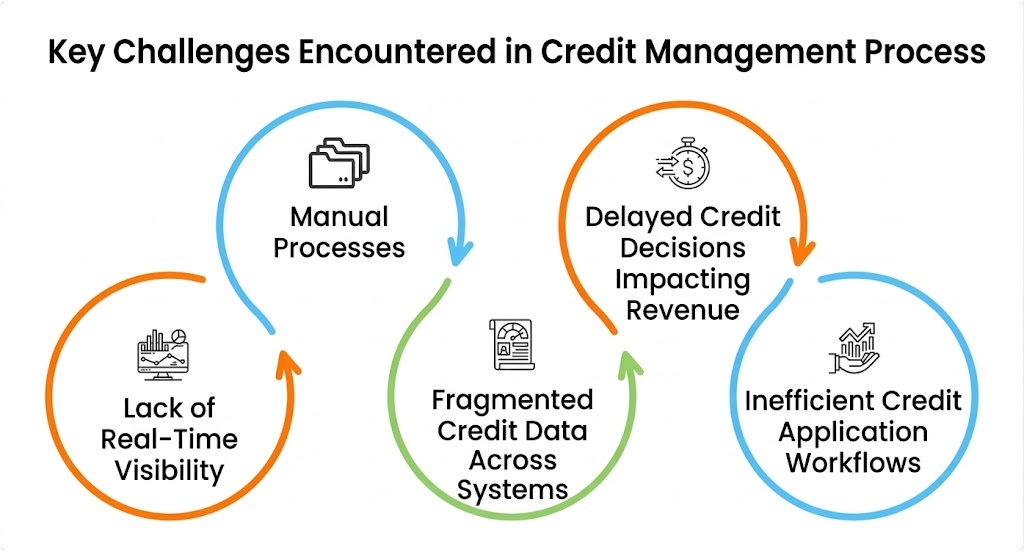

Key Challenges Encountered in Credit Management Process

Even with defined policies in place, many organizations struggle to execute credit management effectively. Operational inefficiencies, limited visibility, and fragmented processes make it difficult to balance growth with risk control.

1. Lack of Real-Time Credit Risk Visibility

Credit decisions are often based on static financial data and periodic credit reports that quickly become outdated. Without continuous visibility into customer behavior, payment patterns, and external risk signals, finance teams are forced to react to issues after they occur rather than proactively managing risk.

2. Heavy Reliance on Manual Processes

Many credit teams still depend on spreadsheets, emails, and manual reviews to evaluate applications and approve credit. This not only slows down decision-making but also increases the likelihood of errors, inconsistencies, and missed risk indicators—especially as transaction volumes scale.

3. Fragmented Credit Data Across Systems

Critical customer data is often spread across ERPs, credit bureaus, emails, and internal files, making it difficult to get a unified view of risk. This fragmentation forces teams to spend time gathering and reconciling data instead of focusing on analysis and decision-making.

4. Delayed Credit Decisions Impacting Revenue

Slow credit approvals can delay customer onboarding and order processing, directly affecting revenue realization. In competitive markets, delays in extending credit can also lead to lost business, as customers move to faster, more responsive suppliers.

5. Inefficient Credit Application Workflows

Unstructured or incomplete credit applications create repeated back-and-forth between teams and customers. Missing information, unclear formats, and lack of standardization slow down the entire process, increasing onboarding time and reducing operational efficiency.

Why Businesses Are Moving Toward Automated Credit Management

As transaction volumes increase and customer risk becomes more dynamic, manual credit processes fail to keep pace. Businesses are adopting automated credit management to reduce delays, improve consistency, and gain real-time visibility into customer risk.

Automation enables faster onboarding, better risk control, and more predictable cash flow—without increasing operational overhead.

Templates

Finance Teams Waste 50%+ Time on Manual Credit Tasks. What’s It Costing You?

Use this credit ROI calculator to find out how much can you save with automated credit management processes

How Does an Autonomous Credit Management Process Work and What Does It Look Like?

With the Credit Risk Management Software, you can lower bad debt and improve analyst productivity. Sounds intriguing, right? Let us understand how that is possible.

Faster customer onboarding with online credit application

Implementing a configurable online credit application can significantly reduce the time and effort required for customer onboarding. Online credit applications can be customized based on customer segments and configured in multiple languages. Pre-filled credit applications from the sales team can further streamline the process, allowing customers to complete the application quickly and easily.

Automated credit data aggregation

Leverage technology and auto-capture credit ratings, financials, and credit insurance information from 40+ global and local agencies in one go.

Automated credit scoring and approval workflows:

Automating credit scoring and approval workflows can help credit teams fast-track credit decisions and improve the efficiency of the credit management process. Configurable credit scoring models can be customized based on customer segments or business units, helping credit teams make consistent and informed credit decisions.

Real-time credit risk monitoring:

Regular monitoring of customer portfolios can provide credit teams with real-time visibility into changes in credit profiles, payment behavior, and financial filings. With significant macroeconomic fluctuations, regular monitoring can help credit teams identify at-risk customers and take timely action to mitigate credit risk.

Automating credit management can help you in so many ways, from acquiring customers faster to fueling revenue growth. Let’s explore a success story to understand how businesses leverage the benefits of automating account credit management and how it can revolutionize your business.

Templates

Poor Vendor Selection Drives Hidden Costs Across Credit Operations.

Use a structured scorecard to identify the right-fit solution, reduce inefficiencies, and improve long-term ROI.

How The Right Credit Management Solution Transforms Businesses

The Chevron Phillips case study

Chevron Phillips, a leading chemical manufacturer, transformed its credit process to achieve 61% faster customer onboarding while strengthening alignment between credit and sales to drive growth.

Challenges they faced

Delayed onboarding slowed revenue Manual, paper-based credit applications led to incomplete data and multiple back-and-forths, stretching onboarding timelines to ~7 days and impacting customer experience.

No prioritization across customer risk High-value accounts required complex reviews, while low-risk accounts consumed equal effort—creating inefficiencies and slowing decision-making.

No centralized customer data Disconnected systems and manual data handling made it difficult to access accurate, real-time credit information, increasing risk exposure.

Complex customer structures created confusion Joint venture accounts made it hard to assess credit limits and risk at both entity and group levels.

How HighRadius Helped

61% faster onboarding with digital credit applications Standardized, mandatory data capture eliminated delays and reduced back-and-forth.

Automated approval workflows Enabled faster, policy-driven decisions across different risk tiers.

Centralized credit data and real-time visibility Provided a single source of truth with continuous risk monitoring.

Simplified credit management for complex hierarchies Enabled clear visibility into credit exposure across joint ventures.

Case Studies

From 7-Day Onboarding to 61% Faster Customer Activation.

See how automation eliminated manual bottlenecks and enabled 2X faster credit decisions at scale.

How HighRadius Credit Management Solution Helps Accelerate Credit Decisioning

HighRadius Credit Management helps finance teams automate credit decisioning, standardize risk evaluation, and gain real-time visibility into customer exposure. By combining AI-driven scoring with automated workflows, it enables faster approvals, reduces manual effort, and improves control over credit risk.

With real-time credit risk analysis software and credit decisioning software, you can receive alerts for any changes in your customers’ credit profile and make data-driven credit decisions from unlimited credit reports. Our software integrates with your ERP system and can start monitoring your customers in just 30 days.

We offer configurable credit scoring software and approval workflows that can be customized based on geography, customer segments, business units, and other factors. You can fast-track credit approvals through complex corporate hierarchies, making the credit application process more efficient and streamlined.

Our highly configurable online credit application allows you to onboard customers across the globe with multi-language, customized credit applications embedded on your website. You can automatically capture financials, personal guarantees, and check bank references, reducing the need for manual data entry.

Our software also automatically extracts credit data from over 40+ global and local agencies, including credit ratings, financials, and credit insurance information. You can configure the auto-extracted data in your preferred currency, making it easier to analyze and interpret.

With AI-based blocked order management, you can auto-predict blocked orders based on the customers’ credit limit utilization and payment history. You can leverage AI-based release or partial payment recommendations for faster credit decisions, reducing the need for manual intervention.

Struggling With Incomplete Credit Applications?

Explore the #1 software that makes onboarding customer faster and easier

Accelerate payment recovery from delinquent customers and boost cash flow through automated collection workflows.

Cash App

Achieve same day cash application with automated remittance aggregation

Credit

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Deductions

Reduce Revenue Leakage with AI Prediction models that identify valid and invalid deductions.

Online Credit Application

Onboard customers seamlessly with a configurable online credit application. Cut down on back-and-forth and collect all customer details in one go.

Frequently Asked Questions (FAQs)

1. What does HighRadius Credit Management do?

HighRadius Credit Management automates credit decisioning, scoring, and approvals using AI-driven workflows. It centralizes customer data, standardizes risk evaluation, and enables faster, policy-driven credit decisions—helping finance teams reduce manual effort and improve cash flow predictability.

HighRadius Credit Management automates credit decisioning, scoring, and approvals using AI-driven workflows. It centralizes customer data, standardizes risk evaluation, and enables faster, policy-driven credit decisions—helping finance teams reduce manual effort and improve cash flow predictability.

2. What are the benefits of AI-powered credit and collections software?

AI-powered credit and collections software improves decision speed, accuracy, and scalability. It automates data collection, scoring, and customer communication—reducing manual work, minimizing errors, and enabling proactive risk management across the credit-to-cash lifecycle.

AI-powered credit and collections software improves decision speed, accuracy, and scalability. It automates data collection, scoring, and customer communication—reducing manual work, minimizing errors, and enabling proactive risk management across the credit-to-cash lifecycle.

3. Is HighRadius suitable for enterprise credit and collections teams?

Yes, HighRadius is designed for enterprise finance teams managing large customer portfolios. It supports complex credit policies, integrates with ERP systems, and enables scalable automation across credit, collections, and cash application processes.

Yes, HighRadius is designed for enterprise finance teams managing large customer portfolios. It supports complex credit policies, integrates with ERP systems, and enables scalable automation across credit, collections, and cash application processes.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.