AI in credit risk management refers to the use of machine learning, real-time data, and automation to assess customer creditworthiness, predict default risk, and improve credit decisions. Unlike traditional models that rely on static financial data, AI enables continuous risk monitoring and more accurate decision-making across the credit lifecycle.

Table of Contents

Why Traditional Credit Risk Management Falls Short

How AI is Transforming Credit Risk Management

The Traditional Approach to Manage Credit Risk

Advantages of AI-Powered Credit Management

AI-Powered Credit Risk Management: How Does It Work?

Real-World Use Cases of AI in Credit Risk Management

How HighRadius Credit Management Solution Helps Accelerate Credit Decisioning

Why Traditional Credit Risk Management Falls Short

Manual credit risk management relies on historical data, fragmented systems, and subjective judgment. This creates:

Delayed credit decisions Multiple handoffs, manual reviews, and incomplete data slow down approvals.

Inconsistent risk assessment Different analysts apply different criteria, leading to uneven decision-making.

Limited visibility into changing customer behavior Static reports fail to capture real-time shifts in payment patterns and risk signals.

Higher exposure to bad debt Late identification of risk increases defaults and write-offs.

This is where AI-driven credit risk management changes the model.

AI-powered credit decisioning software leverages the power of artificial intelligence and machine learning algorithms to analyze vast amounts of data, identify patterns, and make accurate predictions about credit risk. By automating the credit risk assessment process, AI-powered systems can provide large enterprises with faster, more accurate, and more reliable credit risk assessments than traditional methods.

In addition, AI-led credit scoring helps large enterprises to manage credit risk effectively and efficiently. It offers a range of benefits, including improved accuracy, faster decision-making, reduced risk, and cost savings.

Not All AI Solutions Deliver Results. Most Just Add Complexity.

AI automation improves accuracy, detects risk patterns, and enables proactive credit and collections strategies at scale.

AI in credit risk management is shifting how businesses evaluate, monitor, and control customer risk. Instead of relying on static data and periodic reviews, AI enables continuous, data-driven decision-making across the credit lifecycle.

Key ways AI in credit risk management is transforming operations include:

Real-time credit risk analysis AI evaluates customer behavior continuously using transactional and behavioral data, eliminating reliance on outdated financial snapshots.

Improved prediction accuracy Machine learning models identify complex risk patterns that traditional scoring methods often miss, leading to better default prediction.

Automated credit decisioning AI applies predefined policies and risk models instantly, enabling faster, consistent credit approvals without manual intervention.

Dynamic risk monitoring Risk scores update in real time as customer behavior changes, allowing teams to proactively manage exposure and take timely action.

The Traditional Approach to Manage Credit Risk

Traditional methods of credit risk management involve a variety of manual processes, such as gathering information on potential borrowers, assessing their creditworthiness, and monitoring their credit performance over time. These processes rely heavily on human judgment and are often prone to errors, inconsistencies, and biases.

That’s why, large enterprises now leverage AI-driven solutions for credit risk management. They use advanced, autonomous AI agents to accelerate credit reviews, ensure accurate credit decisioning and leverage AI-led credit scoring models to reduce past dues and credit risks.

Feature

Traditional

AI-Based

Data

Historical

Real-time + external

Analysis

Manual

Automated

Decision Speed

Slow

Instant

Risk Monitoring

Periodic

Continuous

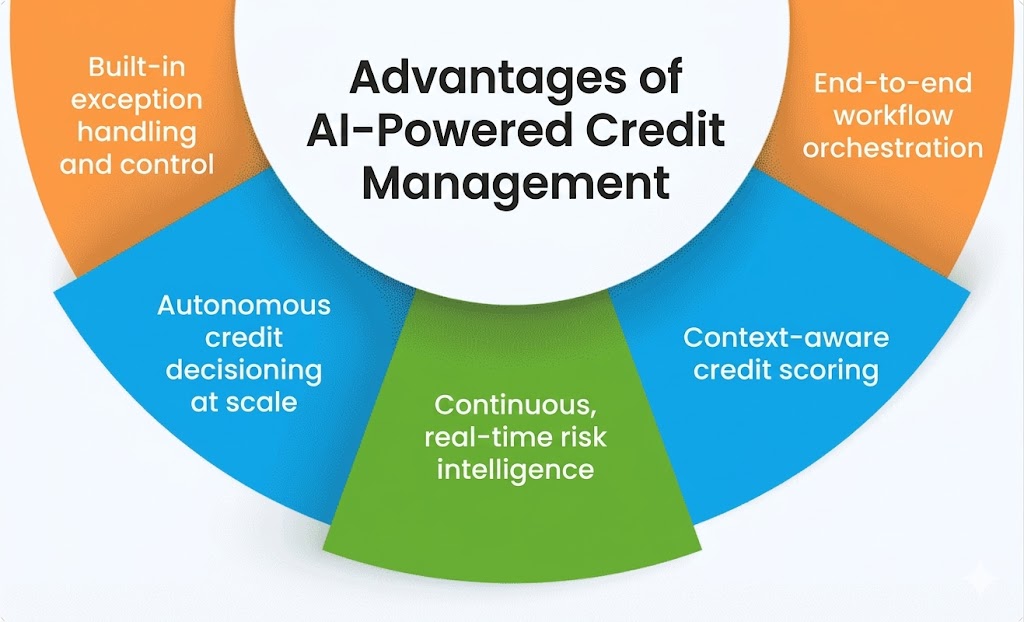

Advantages of AI-Powered Credit Management

Agentic AI is redefining credit management by moving beyond static automation to autonomous, decision-driven workflows. Instead of just analyzing data, AI agents continuously evaluate risk, trigger actions, and optimize outcomes across the credit lifecycle.

Built-in exception handling and control

High-risk or complex cases are automatically routed for review, ensuring governance while maintaining speed and efficiency.

Autonomous credit decisioning at scale

AI agents independently assess creditworthiness, apply policies, and approve or escalate decisions in real time, eliminating manual bottlenecks.

Continuous, real-time risk intelligence

Instead of periodic reviews, agentic AI monitors customer behavior, payment patterns, and external signals continuously, enabling proactive risk management.

Context-aware credit scoring

AI dynamically adjusts risk scores based on evolving data inputs, ensuring more accurate and adaptive credit decisions across changing business conditions.

End-to-end workflow orchestration

From data collection to decisioning and monitoring, AI agents automate the entire credit process, ensuring consistency across teams, regions, and portfolios.

AI-Powered Credit Risk Management: How Does It Work?

1. Multi-Language Online Credit Applications for Onboarding Customers Globally

With a configurable Online Credit Application, credit teams can onboard customers faster across the globe. Online Credit Applications can be configured and translated into any required language and based on customer segments. With pre-filled credit applications from the sales team, customers don’t need to spend a lot of time filling up the credit application.

2. Consolidated View of Credit Risk Globally

Credit teams can seamlessly integrate across multiple ERPs, and business units, and review credit risk in a standard, global currency. The senior management can review the overall credit risk exposure across geographies to develop strategies to reduce bad debt. Additionally, they can drill down to a particular geography and check the credit exposure, even in the local currency.

3. Automatically Extract Credit Data from 40+ Credit Agencies and Bureaus

Automatically extract credit reports, ratings, financials, and credit insurance information from 40+ global and local agencies such as D&B, Experian, CreditSafe, Equifax, and Serasa. With HighRadius Credit Cloud, credit teams can access a one-stop repository for all credit information required for global operations.

4. Automated Credit Scoring and Approval Workflows

Automated credit scoring is the swift evaluation of an individual’s or a business’s creditworthiness using advanced algorithms and predefined criteria. It assesses financial factors to generate a numerical score, streamlining decision-making for credit teams.

Integrated with collaborative e-workflows, these credit scoring models can be configured seamlessly across business units, geographies, or diverse customer segments.

5. Real-Time Credit Risk Monitoring

In the current economy, Real-Time Credit Risk Monitoring helps credit teams to monitor customer portfolios daily on a real-time basis. Credit analysts can receive real-time alerts related to bankruptcy, dips in credit scores, and changes in payment behavior to stay on top of risks and control overall bad debt. This way they can proactively manage the credit risk.

Templates

You’re Missing 25–40% Efficiency Gains With The Wrong Credit Risk Solution

Find out how automation scales credit operations while improving consistency and control.

Real-World Use Cases of AI in Credit Risk Management

AI in credit risk management is actively driving measurable outcomes for large enterprises by transforming how credit decisions are made, monitored, and scaled. The following examples highlight how organizations are using AI to move from manual, fragmented processes to automated, data-driven credit operations.

Mosaic’s success story

The Mosaic Company implemented an AI-driven credit risk management solution to streamline its credit approval process and improve decision efficiency across a large customer base.

By integrating data from credit bureaus, financial statements, and payment histories into a single system, the company enabled a unified and real-time view of customer risk. AI models then evaluated this data to generate consistent risk scores and drive decision-making.

The impact:

Improved consistency across credit evaluations

Reduced approval layers from nine to four, eliminating unnecessary manual intervention

Accelerated credit decision timelines without compromising risk controls

Case Studies

How this Fortune 500 company unlocked 50% credit decisions?

Here’s how AI-driven workflows helped Mosaic reduce credit delays and improve credit decision consistency.

Chevron Phillips Chemical, an American chemical manufacturer, also implemented an AI-powered credit risk management solution to automate their credit management processes.

The solution continuously analyzed customer data and identified early risk signals, enabling the credit team to act before issues escalated. Automated workflows ensured consistent credit reviews across accounts without manual intervention.

Key outcomes:

Automated credit reviews, improving speed and consistency

How HighRadius Credit Management Solution Helps Accelerate Credit Decisioning

HighRadius Credit Management helps finance teams automate credit decisioning, standardize risk evaluation, and gain real-time visibility into customer exposure. By combining AI-driven scoring with automated workflows, it enables faster approvals, reduces manual effort, and improves control over credit risk.

With real-time credit risk analysis software and credit decisioning software, you can receive alerts for any changes in your customers’ credit profile and make data-driven credit decisions from unlimited credit reports. Our software integrates with your ERP system and can start monitoring your customers in just 30 days.

We offer configurable credit scoring software and approval workflows that can be customized based on geography, customer segments, business units, and other factors. You can fast-track credit approvals through complex corporate hierarchies, making the credit application process more efficient and streamlined.

Our highly configurable online credit application allows you to onboard customers across the globe with multi-language, customized credit applications embedded on your website. You can automatically capture financials, personal guarantees, and check bank references, reducing the need for manual data entry.

Our software also automatically extracts credit data from over 40+ global and local agencies, including credit ratings, financials, and credit insurance information. You can configure the auto-extracted data in your preferred currency, making it easier to analyze and interpret.

With AI-based blocked order management, you can auto-predict blocked orders based on the customers’ credit limit utilization and payment history. You can leverage AI-based release or partial payment recommendations for faster credit decisions, reducing the need for manual intervention.

Struggling With Incomplete Credit Applications?

Explore the #1 software that makes onboarding customer faster and easier

Accelerate payment recovery from delinquent customers and boost cash flow through automated collection workflows.

Cash App

Achieve same day cash application with automated remittance aggregation

Credit

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Deductions

Reduce Revenue Leakage with AI Prediction models that identify valid and invalid deductions.

Online Credit Application

Onboard customers seamlessly with a configurable online credit application. Cut down on back-and-forth and collect all customer details in one go.

Frequently Asked Questions (FAQs)

1. What is the role of AI in credit risk management?

AI plays a pivotal role in credit risk management by employing advanced algorithms to swiftly analyze vast datasets. It enhances decision-making accuracy, identifies patterns, and assesses creditworthiness, ultimately providing a more comprehensive and efficient approach to managing credit risks.

AI plays a pivotal role in credit risk management by employing advanced algorithms to swiftly analyze vast datasets. It enhances decision-making accuracy, identifies patterns, and assesses creditworthiness, ultimately providing a more comprehensive and efficient approach to managing credit risks.

2. What are the main benefits of using AI in credit risk management?

With AI-Powered Credit Management Software, credit teams can achieve 100% real-time credit risk monitoring to ensure lower bad debt by tracking changes in customer credit risk and payment behavior. AI can be leveraged to predict blocked orders based on past order volumes and payment patterns.

With AI-Powered Credit Management Software, credit teams can achieve 100% real-time credit risk monitoring to ensure lower bad debt by tracking changes in customer credit risk and payment behavior. AI can be leveraged to predict blocked orders based on past order volumes and payment patterns.

3. How AI is used in risk management in banks?

AI is employed in banks’ risk management by utilizing ML algorithms to analyze extensive financial data. It enhances fraud detection, assesses credit risks, and automates compliance processes. This technology improves decision-making, reduces operational risks, and strengthens risk management.

AI is employed in banks’ risk management by utilizing ML algorithms to analyze extensive financial data. It enhances fraud detection, assesses credit risks, and automates compliance processes. This technology improves decision-making, reduces operational risks, and strengthens risk management.

4. What is the role of AI in credit lending?

AI plays a crucial role in credit lending by automating credit scoring processes. It swiftly analyzes borrower data, assesses creditworthiness, and streamlines decision-making. This improves efficiency, reduces risks, and enables lenders to make more informed and accurate lending decisions.

AI plays a crucial role in credit lending by automating credit scoring processes. It swiftly analyzes borrower data, assesses creditworthiness, and streamlines decision-making. This improves efficiency, reduces risks, and enables lenders to make more informed and accurate lending decisions.

5. What is credit risk monitoring?

Credit risk monitoring involves continuous assessment and surveillance of borrowers’ credit profiles. It utilizes data analysis and key indicators to track changes in creditworthiness, helping lenders identify potential risks and make informed decisions to mitigate financial losses.

Credit risk monitoring involves continuous assessment and surveillance of borrowers’ credit profiles. It utilizes data analysis and key indicators to track changes in creditworthiness, helping lenders identify potential risks and make informed decisions to mitigate financial losses.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.