B2B Credit Application: The Ultimate Guide to Strengthening Customer Onboarding

Last Updated: 12 July, 2026

•

Editorial Team HighRadius

2026 Automation Benchmark Report

HighRadius 2026 Automation Benchmark Report For The Office Of The CFO

Understand if your performance is on par with top 10% of the organizations. Identify gaps, best practices and know how you can drive value through Agentic AI-Driven Automation.

In the B2B space, most businesses operate on credit; however, this system has its drawbacks. Granting credit without thoroughly assessing customers’ creditworthiness could be risky, especially for mid-sized companies. Just as a car requires fuel to run, a mid-sized business needs a healthy cash flow to survive. A single delinquent account can negatively impact your cash flow. Therefore, businesses must carefully evaluate credit applications from customers to reduce risk.

Credit applications have come a long way from paper applications to online applications, and today, many companies are choosing automated credit application software to optimize their credit management.

Continue reading to explore the B2B credit application process, common challenges within it, steps to consider before granting credit, and more. Additionally, you can try out ready-made credit application templates to expedite the customer onboarding process and explore an automated credit application for your business.

Table of Contents

Introduction

What Is a Business Credit Application?

9 Key Elements to Create the Perfect B2B Credit Application

4 Expert Tips To Create a Successful Credit Application

What To Include In a Business Credit Application?

Sample Credit Application for Business

Manual Credit Application Process Challenges

The Power of Automation in Business Credit Application Processing

Benefits of an Automated Credit Application

How HighRadius Can Help to Automate Credit Application Processing

What Is a Business Credit Application?

A business credit application is a formal document that a company submits to a creditor when applying for a line of credit. This application provides essential information about the business and its finances, helping the creditor evaluate the company’s creditworthiness and ability to repay the debt.

Still trusting credit scores alone? That’s risky.

See the 15 hidden factors that help uncover true credit risk.

The primary purpose of these credit applications is to compile necessary details from the customer, enabling an evaluation of their financials and gauging the inherent risk associated with extending credit to that particular business. Standard information included in a B2B credit application encompasses the business name, address, nature of operations, duration of business activity, financial specifics like revenue and cash flow, and credit references.

In some cases, the B2B credit application might outline credit terms and conditions, encompassing payment timelines, interest rates, and potential fees or penalties. Having the right business credit application software solution can help streamline the process and accelerate credit decisions.

9 Key Elements to Create the Perfect B2B Credit Application

Creating the perfect credit application for businesses involves including crucial elements that gather comprehensive information while being user-friendly and efficient. Here are the key elements that you must have in your application:

Date of application: Specifying the date is essential to determine when the agreement begins.

Business information section: Provides basic identification details necessary to establish the identity and legal entity of the business.

Legal name of the business

Business address (headquarters and any additional locations)

Ownership and management details: Helps understand the structure and leadership of the business, providing insight into decision-making and accountability.

Names and titles of key executives and decision-makers

Ownership structure (names of owners, percentage ownership)

Contact information for key personnel

Financial information: Assesses the financial health and stability of the business, including its ability to generate revenue, manage expenses, and meet financial obligations.

Annual revenue

Profit margins

Cash flow statements

Balance sheets

Income statements

Financial projections (if available)

Bank references

Trade references: Offers insights into the business’s payment history and relationship with other suppliers or vendors, indicating its creditworthiness and reliability.

Names and contact information of current or previous trade partners

Duration of the relationship

Payment history and credit terms

Credit request: Specifies the amount and purpose of the credit requested, guiding the creditor in assessing the appropriateness and feasibility of the credit arrangement.

Desired credit amount

Purpose of the credit (e.g., inventory purchase, equipment financing)

Proposed repayment terms (length of the credit period, interest rates)

Legal and authorization section: Ensures that the information provided is accurate and authorized by a responsible party within the business, mitigating the risk of fraud or misrepresentation.

Signature of an authorized representative of the business

Acknowledgment of terms and conditions

Authorization for credit checks and verification of information provided

Additional documentation requested: Supplements the application with supporting documents that provide further context and verification of the business’s identity, legality, and financial status.

Business licenses or permits

Tax identification number (TIN) or employer identification number (EIN)

Articles of incorporation or partnership agreements

Personal financial statements of key executives or owners

Instructions and guidance: Helps the applicant understand the purpose of each section and how to complete the application accurately, reducing errors and delays in processing.

Clear instructions on how to complete the application

Explanation of each section and the purpose of the information requested

Contact information for assistance or inquiries

4 Expert Tips To Create a Successful Credit Application

There is nothing better than first hand experience to solidify your business credit application. So, we have brought you some tips straight from our experts to ensure you have the best credit application process for your business.

Privacy and data security compliance: Ensure compliance with data protection regulations and assure the security of sensitive information provided by the business. This demonstrates the creditor’s commitment to protecting the confidentiality and security of the applicant’s sensitive information, building trust, and compliance with data protection regulations.

Ensure scalability and flexibility in credit application process: Design the application to accommodate potential growth or changes in the business’s needs over time. This allows the application to accommodate possible changes or growth in the business, ensuring that the credit arrangement remains suitable and sustainable over time.

Utilize a user-friendly format: Present the application in a clear, organized, and easy-to-understand format to facilitate completion by the applicant. This enhances the applicant’s experience by presenting information in a clear, organized manner, reducing confusion and streamlining the application process.

Have a robust review and approval process: Outline the steps involved in reviewing and approving the credit application, including estimated timelines and communication channels for updates or inquiries. This sets expectations regarding the steps involved in evaluating the application, providing transparency and accountability in the decision-making process.

What To Include In a Business Credit Application?

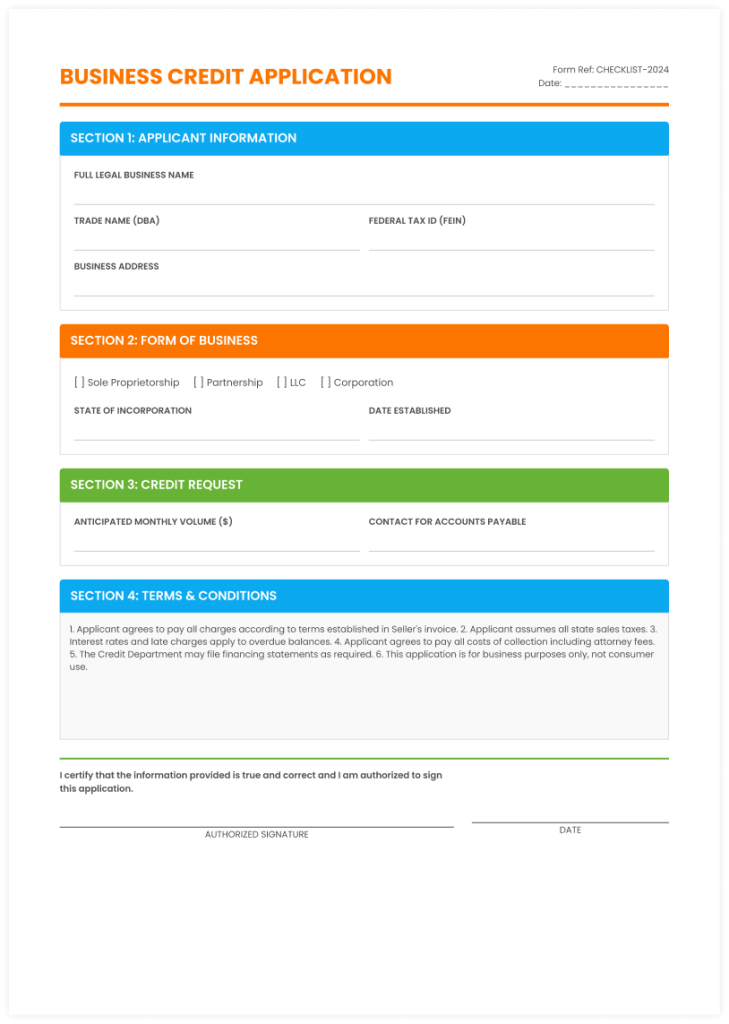

Delays in customer onboarding often arise from incomplete credit applications. Missing details, unclear terms, and inconsistent formats force teams into manual follow-ups and slow approvals. A well-structured business credit application eliminates that friction by capturing the right data upfront. Whether you’re building a credit application for business from scratch or refining an existing business credit application template, these six sections ensure consistency, speed, and better credit risk control.

1. Applicant’s Information

Capture complete and verifiable company details upfront to eliminate delays later in the process. A standard credit application form should include legal business name, registered address, tax identification numbers, and primary contact details. Getting this right ensures your team can validate the entity quickly and avoid onboarding errors.

2. Form of Business

Understand the legal structure of the applicant, whether it’s a sole proprietorship, partnership, LLC, or corporation. Every business credit application should clearly capture this, as it directly impacts liability, risk exposure, and whether personal guarantees or additional documentation are required.

3. Credit Extension

Define the specifics of the credit being requested, including the credit limit, payment terms (Net 30, Net 45, etc.), and expected purchase volume. A well-designed credit application for business uses this data to benchmark requests against internal credit policies and risk thresholds.

4. Applicant’s Certification

Require the applicant to confirm that all information provided is accurate and complete. In any sample credit application for business, this section establishes accountability and reduces the risk of misinformation, especially when decisions rely on self-reported data.

5. Applicant’s Authorization

Include explicit consent for credit checks, including pulling business and, where applicable, personal credit reports. A compliant business credit application template ensures this authorization is clearly documented, avoiding legal or operational delays during credit evaluation.

6. Terms and Conditions

Clearly outline payment expectations, late fees, interest charges, dispute handling, and consequences of non-payment. A structured credit application form standardizes these terms upfront, reducing ambiguity and ensuring enforceability before credit is extended.

Templates

Is credit application blocking your revenue cycles and delaying credit decisions?

Design your credit application with our best-in-class, free template.

A well-designed business credit application template captures comprehensive data, from legal entity structures and trade references to bank credit history, enabling suppliers to move beyond manual vetting toward a more consistent, data-driven credit evaluation process. Whether using a standardized credit application form or a sample credit application for business, this structured approach accelerates onboarding, improves credit decision accuracy, and reduces back-and-forth with customers. More importantly, a well-built credit application for business establishes clear terms, conditions, and authorizations upfront, helping mitigate the risk of bad debt, disputes, and delayed payments across the order-to-cash cycle.

Manual Credit Application Process Challenges

The world is moving rapidly today, and this means we have to keep evolving our processes to more efficient methods if we want to keep up.

Document management and verification are key challenges within the credit application process. The complexity of evaluating diverse financial documents and references can lead to delays and inaccuracies in the decision-making process. This challenge becomes particularly pronounced when handling a large number of credit applications. Here are some significant challenges:

Time-consuming – Manual credit application processes can be time-consuming, especially if companies have to manage a large volume of applications. This can lead to delays in credit decisions, which can impact business operations and customer relationships.

Inconsistent credit risk evaluation – Manual processes can lead to inconsistent assessment of credit applications, as different credit analysts may apply different criteria or weigh factors differently. This can lead to bias and result in inaccurate credit decisions.

Data entry errors – Manual data entry can result in errors, such as typos or transposed numbers, impacting credit decisions. These errors can also be time-consuming to correct and can delay credit decisions.

Limited data analysis – Manual processes can limit the amount of data analysis that can be performed, as analysts may not have access to all the information they need or may not have the tools or resources to analyze data effectively.

Inadequate credit monitoring – Manual application processes can make it challenging to monitor credit risk effectively, as analysts may not have timely access to information about changes in a customer’s credit profile or payment behavior. This can lead to missed opportunities to identify potential credit problems early on and take appropriate measures to mitigate risk.

These challenges can result in inaccurate credit decisions, delays in credit decisions, and increased credit risk. Amidst these challenges, the need for a streamlined and automated credit application process becomes evident. Transitioning to an automated digital solution can help B2B companies mitigate these obstacles and enhance their credit risk management strategies.

The Power of Automation in Business Credit Application Processing

Automation in the credit application process refers to the use of technology and software systems to streamline and expedite the various stages involved in assessing, approving, and managing credit applications. This automation entails leveraging advanced algorithms, data analysis, and digital workflows to replace manual tasks and decision-making processes traditionally performed by humans. The adoption of automation in credit application processing offers numerous benefits for both creditors and applicants, revolutionizing the efficiency, accuracy, and overall effectiveness of the credit approval process.

Benefits of an Automated Credit Application

Automating the credit application process offers a wide range of benefits for both creditors and applicants. Let’s explore.

Enhanced efficiency: Automation streamlines the credit application process, reducing manual tasks, paperwork, and processing time.

Improved accuracy: Automated systems ensure consistent data collection, validation, and analysis, minimizing errors and discrepancies in applicant information. This leads to more accurate credit decisions and reduces the risk of fraudulent or incomplete applications.

Cost savings: By eliminating manual labor and reducing administrative overhead, automated credit application processes result in cost savings for creditors. They require fewer resources to manage and process applications, leading to increased operational efficiency and lower overhead costs.

Improved customer experience: Automation provides a smoother and more streamlined experience for applicants, with faster response times and more straightforward communication throughout the application process. This enhances customer satisfaction and loyalty, fostering positive relationships between creditors and applicants.

Increase in scalability: Automated systems are scalable and can handle a large volume of credit applications without sacrificing speed or accuracy. This scalability allows creditors to efficiently manage fluctuations in application volumes and accommodate business growth without additional strain on resources.

Improves regulatory compliance: Automated credit application systems can incorporate regulatory requirements and compliance checks into the application process, ensuring adherence to legal and industry standards. This reduces the risk of non-compliance penalties and enhances regulatory oversight and reporting capabilities.

Access to data analysis and insights: Automated systems generate valuable data and insights from credit application data, including trends, patterns, and performance metrics. This data can be used to optimize processes, identify opportunities for improvement, and make strategic decisions to drive business growth.

Effortless integration: Automated credit application systems can integrate with other enterprise systems, such as customer relationship management (CRM) software, accounting systems, and loan origination platforms. This integration enables seamless data exchange and workflow coordination, improving overall operational efficiency and collaboration.

By leveraging technology to streamline and optimize credit application processes, creditors can achieve greater productivity, profitability, and competitiveness in the marketplace.

Ebooks

Slow credit onboarding delays sales cycles — not just credit decisions.

Here are 3 tips for faster credit reviews and decisions.

How HighRadius Can Help to Automate Credit Application Processing

HighRadius offers innovative AI-powered credit management software designed to revolutionize the way businesses manage credit applications. With a specific focus on online credit applications, our software harnesses the power of artificial intelligence and machine learning to automate and optimize the entire credit application lifecycle.

With real-time credit risk analysis software and credit decisioning software, you can receive alerts for any changes in your customers’ credit profile and make data-driven credit decisions from unlimited credit reports. Our software integrates with your ERP system and can start monitoring your customers in just 30 days.

We offer configurable credit scoring software and approval workflows that can be customized based on geography, customer segments, business units, and other factors. You can fast-track credit approvals through complex corporate hierarchies, making the credit application process more efficient and streamlined.

Our highly configurable online credit application allows you to onboard customers across the globe with multi-language, customized credit applications embedded on your website. You can automatically capture financials, personal guarantees, and check bank references, reducing the need for manual data entry.

Our software also automatically extracts credit data from over 40+ global and local agencies, including credit ratings, financials, and credit insurance information. You can configure the auto-extracted data in your preferred currency, making it easier to analyze and interpret.

With AI-based blocked order management, you can auto-predict blocked orders based on the customers’ credit limit utilization and payment history. You can leverage AI-based release or partial payment recommendations for faster credit decisions, reducing the need for manual intervention.

HighRadius AI-based Credit Risk Management Software simplifies the credit application process, mitigates risk with real-time credit visibility, and manages global portfolios through comprehensive workflows.

By partnering with us, you can streamline your credit application process, reduce manual interventions, and ultimately provide a better customer experience.

Struggling With Incomplete Credit Applications?

Explore the #1 software that makes onboarding customer faster and easier

Accelerate payment recovery from delinquent customers and boost cash flow through automated collection workflows.

Cash App

Achieve same day cash application with automated remittance aggregation

Credit

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Deductions

Reduce Revenue Leakage with AI Prediction models that identify valid and invalid deductions.

Online Credit Application

Onboard customers seamlessly with a configurable online credit application. Cut down on back-and-forth and collect all customer details in one go.

Frequently Asked Questions (FAQs)

1. What is credit application for business

A credit application for business is a formal document that collects financial, legal, and trade reference information to assess a customer’s creditworthiness before extending payment terms. It standardizes risk evaluation and ensures consistent credit decisions across the business.

A credit application for business is a formal document that collects financial, legal, and trade reference information to assess a customer’s creditworthiness before extending payment terms. It standardizes risk evaluation and ensures consistent credit decisions across the business.

2. What are some tips for determining creditworthiness?

Assess factors like credit history, income stability, debt-to-income ratio, payment history and verify employment and review assets. Consider credit scores and past financial behavior to gauge creditworthiness accurately.

Assess factors like credit history, income stability, debt-to-income ratio, payment history and verify employment and review assets. Consider credit scores and past financial behavior to gauge creditworthiness accurately.

3. How can a business credit application form help mitigate risk?

A business credit application form helps mitigate risk by gathering essential information about potential clients, enabling thorough assessment of their creditworthiness. It allows businesses to evaluate factors like financial stability, payment history, and credit utilization, aiding in informed decision-making and reducing the likelihood of default or late payments.

A business credit application form helps mitigate risk by gathering essential information about potential clients, enabling thorough assessment of their creditworthiness. It allows businesses to evaluate factors like financial stability, payment history, and credit utilization, aiding in informed decision-making and reducing the likelihood of default or late payments.

4. What are the steps of the credit application process?

The steps of the credit application process typically include submission of application, verification of information, credit analysis, decision-making, approval or denial, and establishment of credit terms.

The steps of the credit application process typically include submission of application, verification of information, credit analysis, decision-making, approval or denial, and establishment of credit terms.

5. What are the red flags on a credit application?

Red flags on a credit application include inconsistent information, gaps in employment history, high debt-to-income ratio, recent delinquencies or bankruptcies, and frequent changes in residence or contact information.

Red flags on a credit application include inconsistent information, gaps in employment history, high debt-to-income ratio, recent delinquencies or bankruptcies, and frequent changes in residence or contact information.

6. Why do we need a credit application?

A credit application is essential for assessing the creditworthiness of potential customers or clients, mitigating risk, establishing credit terms, and ensuring responsible lending practices. It helps businesses make informed decisions about extending credit and managing cash flow effectively.

A credit application is essential for assessing the creditworthiness of potential customers or clients, mitigating risk, establishing credit terms, and ensuring responsible lending practices. It helps businesses make informed decisions about extending credit and managing cash flow effectively.

7. What happens when you submit a credit application?

When you submit a credit application, the lender will review your application to assess your creditworthiness and ability to repay the loan. They will typically check your credit report, income, employment history, and other financial information to make a decision. Once the lender has reviewed your application, they will either approve or deny your request for credit.

When you submit a credit application, the lender will review your application to assess your creditworthiness and ability to repay the loan. They will typically check your credit report, income, employment history, and other financial information to make a decision. Once the lender has reviewed your application, they will either approve or deny your request for credit.

8. How long does it take for a credit application to be reviewed?

Generally, it can take anywhere from a few days to a few weeks for a credit application to be reviewed and a decision to be made. However, with the use of automated credit application processing systems, lenders can drastically reduce the time it takes to review credit applications and provide faster, more efficient service to customers.

Generally, it can take anywhere from a few days to a few weeks for a credit application to be reviewed and a decision to be made. However, with the use of automated credit application processing systems, lenders can drastically reduce the time it takes to review credit applications and provide faster, more efficient service to customers.

9. What are quick steps to consider before granting credit?

Follow these structured steps to make an informed decision: Create a credit policy: Establish a clear policy to outline terms and agreements. Perform a credit check: Review the customer’s financial background for insights. Sign an agreement: Formalize the commitment to payment. Set credit limits: Align limits with credit scores for reduced risk

Follow these structured steps to make an informed decision: Create a credit policy: Establish a clear policy to outline terms and agreements. Perform a credit check: Review the customer’s financial background for insights. Sign an agreement: Formalize the commitment to payment. Set credit limits: Align limits with credit scores for reduced risk

10. What is an example of business credit?

An example of business credit is a trade credit arrangement where a supplier allows a business to purchase goods or services on credit terms, such as net 30 days, allowing the business to pay for the purchases later after receiving the goods or services.

An example of business credit is a trade credit arrangement where a supplier allows a business to purchase goods or services on credit terms, such as net 30 days, allowing the business to pay for the purchases later after receiving the goods or services.

11. What is the difference between B2B credit applications vs. B2C credit applications?

B2B credit applications involve businesses extending credit to other businesses, focusing on trade credit terms and commercial financial information. B2C credit applications pertain to businesses offering credit to individual consumers, emphasizing personal credit history and consumer financial behavior.

B2B credit applications involve businesses extending credit to other businesses, focusing on trade credit terms and commercial financial information. B2C credit applications pertain to businesses offering credit to individual consumers, emphasizing personal credit history and consumer financial behavior.

12. What’s Included in a Business Credit Application?’

Business Information: Company name, address, contact details, and legal structure.

Financial Data: Revenue, profit margins, assets, liabilities, and credit history.

Trade References: Details of previous credit relationships with suppliers or vendors.

Ownership Details: Names, titles, and ownership percentages of company principals.

Industry Sector: Description of the company’s industry, market position, and competitive landscape.

Bank Information: Bank account details and references.

Tax ID: Business tax identification number.

Purpose of Credit: Intended use of credit and desired credit limit.

Guarantees: Personal guarantees or collateral provided to secure credit.

Signature: Authorization and consent for credit checks and terms acceptance.

Business Information: Company name, address, contact details, and legal structure.

Financial Data: Revenue, profit margins, assets, liabilities, and credit history.

Trade References: Details of previous credit relationships with suppliers or vendors.

Ownership Details: Names, titles, and ownership percentages of company principals.

Industry Sector: Description of the company’s industry, market position, and competitive landscape.

Bank Information: Bank account details and references.

Tax ID: Business tax identification number.

Purpose of Credit: Intended use of credit and desired credit limit.

Guarantees: Personal guarantees or collateral provided to secure credit.

Signature: Authorization and consent for credit checks and terms acceptance.

Resource Library

Resource Hub

ASSETS

12 Collection Strategies for Every Aging Bucket (FREE)

Optimize collections across aging buckets with data-driven strategies that reduce costs and improve recovery rates.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.