Credit risk mitigation refers to the structured set of actions businesses take to reduce the probability of customer default and minimize financial losses. It goes beyond risk assessment by focusing on proactive control mechanisms such as credit policies, monitoring, and decisioning frameworks.

For finance teams, effective credit risk mitigation is not just about avoiding bad debt. It is about improving decision accuracy, protecting cash flow, and enabling controlled revenue growth.

This article aims to comprehensively explore credit risk mitigation strategies, challenges faced by finance professionals and presents best practices to ensured informed credit decisioning.

Table of Contents

Introduction

What is Credit Risk Mitigation?

3 Critical Aspects to Consider While Formulating Credit Risk Mitigation Strategies

Credit Risk Mitigation Challenges

Key Credit Risk Mitigation Techniques

Benefits of AI-led Credit Risk Mitigation

How HighRadius’s Solution Helps in Credit Risk Management?

What is Credit Risk Mitigation?

Credit risk mitigation is the process of reducing exposure to potential losses caused by customer non-payment. It involves a combination of risk assessment, policy enforcement, and continuous monitoring to ensure that credit decisions remain aligned with business risk tolerance.

Unlike traditional credit management, credit risk mitigation focuses on ongoing control, ensuring that risks are identified early and managed proactively.

3 Critical Aspects to Consider While Formulating Credit Risk Mitigation Strategies

Before implementing credit risk mitigation strategies, organizations should consider critical aspects that significantly impact their approach. These include:

Adopting portfolio risk monitoring of your customers

Monitoring portfolio risk is pivotal for an organization’s success and risk mitigation. This approach involves identifying, assessing, measuring, and managing risks within the customer portfolio, ensuring enhanced business value delivery and risk mitigation.

Monitoring performance metrics regularly

Continuous monitoring of the receivables performance metrics such as days sales outstanding (DSO), and average days delinquent gives companies a bird’s eye view of their performance and operational efficiency. These metrics provide actionable data for companies to focus on and take corrective measures proactively.

Adopting digitalization to streamline credit operations

Credit teams are often caught up in routine tasks that can easily be automated. These include processes such as credit application process, correspondence etc. This restricts the team from investing their time and efforts in higher-value tasks such as working with sales to improve customer experience and conducting analysis to make better credit decisions.

Technology plays a vital role in building an agile credit function. By leveraging AI-led credit decisioning platforms, organizations can undergo major transformation empowering credit teams to create strategic value in the office of the CFO.

Credit Risk Mitigation Challenges

Credit risk evaluation often breaks down due to gaps in visibility, inconsistent decision-making, and external volatility. The most common challenges include:

Limited visibility into customer credit risk Credit teams rely on fragmented data across ERPs, spreadsheets, and credit reports, which makes it difficult to maintain a unified view of portfolio risk. As a result, changes in customer creditworthiness are not tracked in real time, leading to delayed or reactive decisions.

Inconsistent order release decisions under sales pressure When orders are blocked due to credit limits, sales teams often push for immediate release to avoid revenue delays. In many cases, orders are approved based on informal payment commitments, increasing exposure to default and weakening credit control.

Impact of economic volatility on creditworthiness Changes in interest rates, inflation, and market conditions directly affect customer financial stability. Without continuous monitoring, credit teams struggle to adjust risk assessments in line with evolving economic signals.

To address these challenges, businesses are increasingly adopting automated and AI-driven credit risk mitigation approaches that enable real-time visibility, consistent decisioning, and proactive risk control.

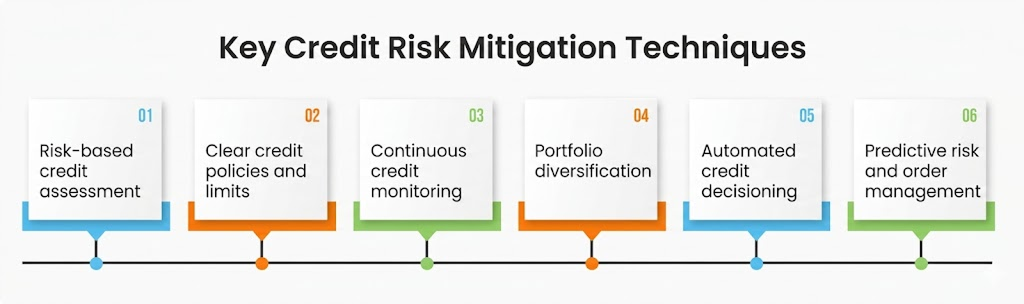

Key Credit Risk Mitigation Techniques

Effective credit risk mitigation combines structured policies, data-driven evaluation, and continuous monitoring to reduce default risk and protect cash flow.

Risk-based credit assessment

Evaluate customer creditworthiness using financial data, payment history, and external credit signals to reduce default probability at the onboarding stage. Modern systems enhance this by automating application data capture, validating inputs against third-party sources, and routing cases to the right analysts based on predefined rules, ensuring faster and more reliable initial decisions.

Clear credit policies and limits

Define credit terms, limits, and approval thresholds to ensure consistent and controlled credit exposure across all customers. These policies can be operationalized through automated workflows that enforce approval hierarchies, standardize decision criteria, and ensure that high-risk exposures are reviewed appropriately.

Continuous credit monitoring

Track customer behavior, payment trends, and risk signals in real time to identify early signs of deterioration. This includes monitoring credit agency updates, financial changes, and external events such as mergers or bankruptcy filings, enabling proactive intervention before risk escalates.

Portfolio diversification

Spread credit exposure across industries and customer segments to reduce concentration risk and improve resilience. A diversified portfolio reduces dependency on specific customers or sectors and helps absorb fluctuations caused by economic or market changes.

Collateral and guarantees

Secure high-risk exposures through collateral, guarantees, or insurance to reduce financial impact in case of default. Advanced systems also track collateral validity, expiry timelines, and coverage levels to ensure that risk exposure remains aligned with available security.

Automated credit decisioning

Use rule-based and AI-driven credit decisioning platforms to standardize decisions, reduce bias, and accelerate approvals. Automated scoring models combine internal and external data to assign risk levels, while low-risk cases can be auto-approved and higher-risk cases routed for review, improving both speed and consistency.

Predictive risk and order management

Leverage predictive analytics to identify potential blocked orders and payment delays before they occur. By analyzing purchasing behavior, payment patterns, and credit utilization, systems can recommend proactive actions such as requesting partial payments or adjusting limits to prevent revenue disruption.

Templates

Standardize Your Credit Application Process with a Free Checklist

Get the ready-to-use checklist trusted by Fortune 500 companies to evaluate new customer credit applications.

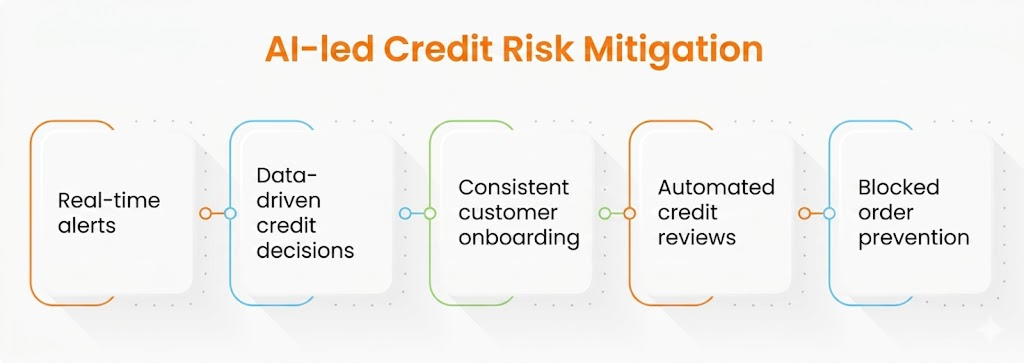

AI-driven credit risk monitoring transforms credit risk mitigation from a periodic, manual activity into a continuous, data-driven control system. By integrating internal data, external signals, and predictive models, organizations can identify risks earlier and act faster.

Proactive risk detection and real-time alerts

AI systems continuously monitor customer behavior, credit agency updates, and external events to identify changes in risk profiles. Automated integrations with multiple data sources enable instant alerts for critical triggers such as payment delays, credit rating changes, or financial deterioration, allowing teams to act before risk materializes.

Data-driven credit decisions that support revenue growth

With real-time visibility into customer creditworthiness, AI models enable more precise credit control decisions. Credit teams can dynamically adjust limits, extend terms to low-risk customers, and align closely with sales to unlock additional revenue while maintaining risk thresholds.

Faster and more consistent customer onboarding

AI automates credit application processing, including data capture, validation, and workflow routing. It also streamlines bank and trade reference verification through automated requests and data extraction, reducing onboarding delays and improving decision consistency.

Automated credit reviews and decisioning workflows

AI-driven credit scoring models combine internal metrics such as payment behavior and credit utilization with external financial and bureau data to generate dynamic risk scores. Low-risk cases can be auto-approved, while high-risk cases are escalated through predefined approval hierarchies, ensuring both speed and control.

Predictive risk and blocked order prevention

Advanced models analyze purchasing patterns, payment trends, and credit exposure to predict potential blocked orders and payment risks. This enables proactive actions such as requesting partial payments or adjusting credit limits before orders are impacted.

By embedding AI across credit risk monitoring, organizations move from reactive risk management to proactive credit risk mitigation, improving cash flow, reducing bad debt, and enabling scalable credit operations.

Traditional vs Modern Credit Risk Mitigation

Feature

Traditional Approach

Modern Approach

Risk assessment

Periodic

Real-time

Data sources

Limited

Internal + external

Decisioning

Manual

Automated

Monitoring

Reactive

Continuous

Accuracy

Variable

High

How HighRadius’s Solution Helps in Credit Risk Management?

HighRadius Credit Management helps finance teams automate credit decisioning, standardize risk evaluation, and gain real-time visibility into customer exposure. By combining AI-driven scoring with automated workflows, it enables faster approvals, reduces manual effort, and improves control over credit risk.

With AI-based blocked order management, you can auto-predict blocked orders based on the customers’ credit limit utilization and payment history. You can leverage AI-based release or partial payment recommendations for faster credit decisions, reducing the need for manual intervention.

With real-time credit risk analysis software and credit decisioning software, you can receive alerts for any changes in your customers’ credit profile and make data-driven credit decisions from unlimited credit reports. Our software integrates with your ERP system and can start monitoring your customers in just 30 days.

We offer configurable credit scoring software and approval workflows that can be customized based on geography, customer segments, business units, and other factors. You can fast-track credit approvals through complex corporate hierarchies, making the credit application process more efficient and streamlined.

Our highly configurable online credit application allows you to onboard customers across the globe with multi-language, customized credit applications embedded on your website. You can automatically capture financials, personal guarantees, and check bank references, reducing the need for manual data entry.

Our software also automatically extracts credit data from over 40+ global and local agencies, including credit ratings, financials, and credit insurance information. You can configure the auto-extracted data in your preferred currency, making it easier to analyze and interpret.

Learn more about HighRadius' Credit Management Software

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Improve onboarding time for your new customers with fully completed credit applications, tailored to your customer branding & requirements.

Credit Workflow Management

Reduce bad debt with a prioritized worklist of high-impact customer accounts demanding immediate attention.

Credit Agency Integration

Identify risky customers by getting alerts on mergers and bankruptcies from credit agencies.

Frequently Asked Questions (FAQs)

1. What are the key components of credit risk management?

The key components of credit risk management involve a streamlined customer onboarding process, efficient credit data aggregation from various sources, implementation of a best-in-class credit scoring model, standardized approval workflows, and regular periodic credit reviews, with credit teams serving as the primary defense against financial risks to the business.

The key components of credit risk management involve a streamlined customer onboarding process, efficient credit data aggregation from various sources, implementation of a best-in-class credit scoring model, standardized approval workflows, and regular periodic credit reviews, with credit teams serving as the primary defense against financial risks to the business.

2. How to onboard customers faster?

Implementing online credit application forms, supported by e-workflows for automatic approvals based on specified criteria, accelerates customer onboarding by replacing manual processes and enhancing the overall experience through efficient automation.

Implementing online credit application forms, supported by e-workflows for automatic approvals based on specified criteria, accelerates customer onboarding by replacing manual processes and enhancing the overall experience through efficient automation.

3. What are the essential fields in a credit application form?

The essential fields in a credit application form include the type of business, requested credit extension, applicant’s certification, applicant’s authorization, and terms & conditions.

The essential fields in a credit application form include the type of business, requested credit extension, applicant’s certification, applicant’s authorization, and terms & conditions.

4. What are the top information sources for credit risk assessment?

The top information sources for credit risk assessment include third-party credit rating agencies and bureaus such as Equifax, FICO, D&B, and Experian, which provide authenticated and accurate information about companies.

The top information sources for credit risk assessment include third-party credit rating agencies and bureaus such as Equifax, FICO, D&B, and Experian, which provide authenticated and accurate information about companies.

5. How to build the perfect credit scoring model?

To build the perfect credit scoring model, employ a flexible approach that considers the diverse characteristics of your customer base, and utilizes real-time data from credible sources such as bank and trade references, public financial statements, credit agency information, and financial stress prediction, while avoiding a one-size-fits-all model that may lead to inefficient and inaccurate credit scores.

To build the perfect credit scoring model, employ a flexible approach that considers the diverse characteristics of your customer base, and utilizes real-time data from credible sources such as bank and trade references, public financial statements, credit agency information, and financial stress prediction, while avoiding a one-size-fits-all model that may lead to inefficient and inaccurate credit scores.

6. What are the major factors to consider for credit scoring?

Major factors to consider for credit scoring include the delinquency score, Paydex score, average days beyond the term, predictive scoring based on historical trade data, failure score indicating the probability of bankruptcy, and the number of years in business. All of these together provide a comprehensive view of effective credit risk management and decision-making.

Major factors to consider for credit scoring include the delinquency score, Paydex score, average days beyond the term, predictive scoring based on historical trade data, failure score indicating the probability of bankruptcy, and the number of years in business. All of these together provide a comprehensive view of effective credit risk management and decision-making.

7. Why is periodic credit review important to stay on top of high-risk customer accounts?

Periodic credit reviews are crucial for staying on top of high-risk customer accounts as they involve constant monitoring of financial health, updating credit data and scores at specific intervals, tracking parameters such as payment behavior and order size, allowing for timely adjustments to credit terms and monitoring the likelihood of delinquency.

Periodic credit reviews are crucial for staying on top of high-risk customer accounts as they involve constant monitoring of financial health, updating credit data and scores at specific intervals, tracking parameters such as payment behavior and order size, allowing for timely adjustments to credit terms and monitoring the likelihood of delinquency.

8. How does standardized credit management workflows help fast-track approvals?

Standardized credit management workflows, facilitated by electronic forms and automation systems, help fast-track approvals by eliminating miscommunications, reducing delays caused by incomplete data, and ensuring a more efficient credit approval process in mid-sized businesses.

Standardized credit management workflows, facilitated by electronic forms and automation systems, help fast-track approvals by eliminating miscommunications, reducing delays caused by incomplete data, and ensuring a more efficient credit approval process in mid-sized businesses.

9. How to improve correspondence with clients?

To improve correspondence with clients, organizations should transition from time-consuming and expensive paper-based methods to efficient electronic channels such as emails and app notifications, utilizing ready-to-use templates for streamlined communication and cost savings.

To improve correspondence with clients, organizations should transition from time-consuming and expensive paper-based methods to efficient electronic channels such as emails and app notifications, utilizing ready-to-use templates for streamlined communication and cost savings.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.