What Is Trade Credit management in O2C? A Guide to Modern Credit Management System

17 July, 2024

11 minute read

Divya Verma, Finance Content Expert

D

Divya Verma

Divya Verma specializes in finance transformation strategy, bringing a content-driven perspective to the rapidly changing FinTech space. With seven years of experience navigating the B2B SaaS landscape, she understands how modern finance leaders think and delivers insights that speak directly to their priorities. When she is not analyzing the latest in enterprise finance, Divya enjoys traveling and getting lost in a good book. Her writing is rooted in sharp domain thinking and a deliberate focus on clarity that finance leaders can act on.

Last updated: 1 July, 2026

Supercharge your Credit strategy with these 23 SMART goals.

Trade credit is a core component of credit management in the order-to-cash (O2C) process, where businesses assess customer risk, define credit terms, and ensure timely payment collection. Credit departments may relate to this even better as they juggle numerous credit applications daily, deciding whether to extend credit. In such cases, even a single poor credit decision may balloon into thousands of challenges, including higher DSOs and increased past dues, which can stop the business from achieving its goal.

This guide helps credit managers understand how to effectively manage their credit process and ensure that their company’s financial operation remains fluid and resilient.

Table of Contents

What Is Credit Management In O2C?

Credit Management In O2C Process: Where Does It Fit?

Key Steps in the Credit Management Process

Importance of Credit Management System

Key Features to Look For in a Credit Management System

What Are The Challenges With Manual Credit Management In O2C Processes?

Why Businesses Are Automating Credit Management in O2C

How HighRadius Can Help Businesses Streamline Credit Management Processes?

FAQs

What Is Credit Management In O2C?

Credit management in O2C refers to the process of evaluating customer creditworthiness, setting credit limits, defining payment terms, and monitoring risk throughout the order-to-cash cycle. It sits between order placement and invoicing, ensuring that revenue is protected while enabling sales growth.

The organization’s credit team typically assesses the buyer’s creditworthiness by reviewing various factors, such as their credit history, financial statements, and payment behavior. They then decide whether to grant credit and, if so, what credit limit to set. Effective trade credit management can help businesses reduce non-payment risk and improve their cash flow.

Optimize Credit Management with Stronger Scoring Models.

Start with 15 proven scoring parameters to reduce risk and delays.

Credit Management In O2C Process: Where Does It Fit?

The O2C cycle spans the entire journey from order receipt to payment collection, including order fulfillment, invoicing, and accounts receivable management. Within this flow, credit management sits early in the process, impacting every downstream step.

Order received The O2C cycle begins when a customer places an order, triggering the need to validate whether the business can safely extend credit.

Credit evaluation At this stage, businesses assess customer creditworthiness, assign credit limits, and define payment terms. This decision directly influences order approval, risk exposure, and future collections performance.

Order fulfillment Once credit is approved, orders are processed and fulfilled. Weak credit checks at this stage can lead to downstream disputes, delays, or bad debt.

Invoicing Accurate invoicing reflects the approved credit terms. Any misalignment between credit decisions and billing creates friction in the payment cycle.

Collections and payment realization The efficiency of collections depends heavily on upstream credit decisions. Poor credit evaluation often results in delayed payments, higher DSO, and increased write-offs.

Credit management acts as the control layer in O2C, determining whether and how credit is extended before revenue is realized. It directly influences cash flow, risk exposure, and the overall efficiency of the order-to-cash cycle.

Key Steps in the Credit Management Process

The steps involved in the B2B credit management process aim to assess credit risk, set credit limits, and monitor payment behavior. Based on the 5Cs of credit, here are the key steps involved in the credit management process:

1. Review the customer’s credit application

For new customers, credit teams review the credit application to gather detailed business information, credit references, billing and shipping information, and more. Reviewing the customer’s credit application involves assessing their financial stability, credit history, and other relevant information to determine their creditworthiness and suitability for extending credit terms. Existing customers may not require this step.

2. Review the customer’s financial health

Credit teams obtain reports from credit agencies to analyze customer credit ratings and payment scores. They review public financial statements, including cash flow, profit and loss, and balance sheets, to assess financial health. existing customers, they evaluate payment behavior alongside third-party credit ratings and financial data. This comprehensive analysis informs decisions on credit limits and terms, ensuring prudent credit management practices.

3. Ask for credit references

Credit teams request credit references, such as bank and trade references, to verify the buyer’s financial position and creditworthiness. By contacting these references, the credit team can verify the customer’s payment history, reliability in meeting financial obligations, and overall financial stability.

4. Calculate the credit score and credit limit

Credit teams use comprehensive risk models to quantify the customer’s creditworthiness. These risk models are customized to the industry and the credit policy followed by the organization. Various parameters are used in these risk models, and they have different weightages across organizations. These parameters generally fall into the following buckets:

Financial Health – Income Statement, Balance Sheet, and Cash Flow Key financial ratios (some of them being industry-specific) are used in the model as financial health indicators.

Payment Behaviour – For existing customers, their payment history acts as a proxy for predicting future payment behavior. KPIs such as average days late (ADL) is used to quantify payment behavior.

Operational Indicators – Age of business, length of customer relationship, number of employees, number of customers, etc.

Environmental Factors – Sometimes, it is essential to consider environmental factors such as the country of operation of the customer (factor in political and regulatory risk), the region of operation (if it is prone to natural calamities).

3rd Party Credit Agency Rating –The D&B Paydex and Experian FICO scores have relevant weightage in credit scoring models.

Upon calculating the credit score, a credit limit corresponding to that score is assigned to the customer.

5. Get credit approvals

Once the credit limit is assigned, it has to be approved by various stakeholders. For instance, a credit analyst might have the authority to approve credit up to $10k, beyond which the credit manager, VP of credit, and other stakeholders get involved. This hierarchical approval ensures that significant credit exposures are carefully reviewed and authorized by those with appropriate oversight and decision-making authority.

Templates

Want to Enhance Your Credit Evaluations?

Use our credit scoring template with D&B, Experian, and NACM data to streamline your credit evaluations,

Traditional credit management relies on manual processes—spreadsheets, emails, and subjective assessments—that are time-consuming, error-prone, and difficult to scale. Decisions are often based on incomplete or outdated data, leading to inconsistent risk evaluation and slower onboarding.

A modern credit management system addresses these gaps by automating decision-making, standardizing workflows, and enabling real-time visibility into customer risk.

Key Benefits of a Credit Management System

Operational efficiency at scale Eliminates repetitive tasks, enabling credit teams to handle higher volumes without increasing effort. risk strategies, and enhancing overall credit management practices.

Faster customer onboarding Automates data collection and validation, reducing delays and minimizing manual back-and-forth.

Accurate credit risk evaluation Uses real-time data and automated scoring models to improve consistency and decision quality.

Real-time risk monitoring Continuously tracks customer behavior, payment patterns, and financial signals to detect risk early.

Centralized data management Integrates multiple data sources into a single view, improving visibility and reducing fragmentation.

Templates

Leverage Customizable Credit Policy Template

Develop or update your credit management practices effectively with the help of a free credit policy template.

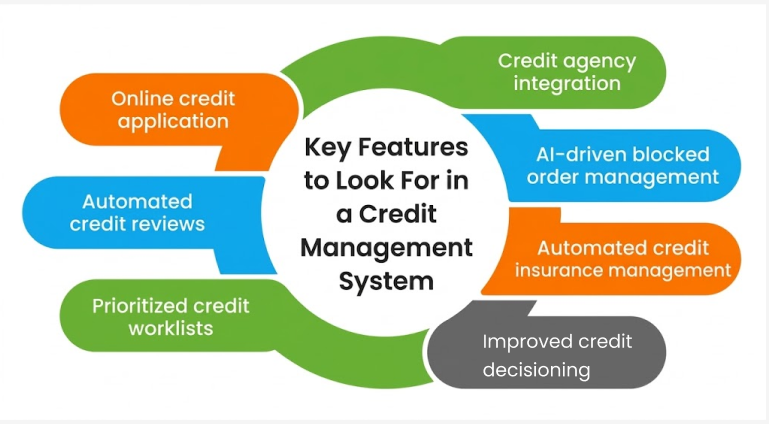

Key Features to Look For in a Credit Management System

When evaluating a credit management system, it’s essential to consider features that enhance the effectiveness and efficiency of your credit risk management. Here are six crucial features in the software to look for:

1. Online credit application

A system offering customizable templates for different industries or regions, efficient document uploads, and trade reference management to expedite the credit application process.

2. Automated credit reviews

Utilize pre-built and configurable credit risk scoring algorithms for faster evaluations, real-time risk alerts, and automated decision-making, especially for low-risk customers.

3. Prioritized credit worklists

This feature uses intelligent algorithms to prioritize customers based on various criteria, such as blocked orders and risk alerts, improving credit decision-making efficiency.

4. Credit agency integration

Automated gathering of credit reports from several agencies, tailored to regional and industry-specific needs, enhances the accuracy of credit risk assessments.

5. AI-driven blocked order management

This feature predicts upcoming blocked orders, recommends order release decisions, and streamlines the approval process.

6. Automated credit insurance management

Automate insurance management for high-risk accounts with integrations to major insurance agencies, providing coverage against commercial debt.

7. Improved credit decisioning

AI-led credit decisioning platforms help businesses not only accelerate credit reviews but also set accurate credit limits for vendors. It eliminates review queues that delay orders and reduces past-due risk.

Ebooks

5 Essential Workflows to Streamline Your Credit Management

Discover essential workflows that can transform your credit management process and boost efficiency.

What Are The Challenges With Manual Credit Management In O2C Processes?

If you are handling credit, you must be aware that credit management is challenging, and it’s crucial to understand these challenges. With that in mind, here are some key credit management challenges every credit team should be aware of:

1. Time-consuming customer onboarding process

Traditionally, credit applications are often paper-based and require manual data entry by the customer, leading to missing or incomplete business information. As a result, too much back-and-forth happens between credit teams and customers to capture the correct and complete information. This introduces delays in credit reference verifications and the entire customer onboarding process, which can negatively impact the customer experience.

2. Manual credit data aggregation, credit scoring, and approvals

Credit teams must manually download credit reports from D&B, Experian, and other credit agencies for each customer. This takes a significant amount of time and effort, particularly with large customer portfolios. Credit analysts must then manually review the credit ratings and financials and calculate the credit score. Thus, credit approvals become slow and tedious due to multiple stakeholders involved.

3. Lack of real-time visibility into portfolio risk

Most credit teams only conduct periodic credit reviews, making it difficult to identify at-risk customers promptly. However, the credit risk of a portfolio can change at any time. With thousands of customer portfolios, it is challenging to review and track frequent changes in their credit profiles regularly and involve significant manual intervention. Consequently, the credit team spends a lot of time on clerical tasks instead of focusing on core credit decisions. These challenges can lead to delays in credit approvals, increased risk of bad debt, and a negative impact on the customer experience.

Why Businesses Are Automating Credit Management in O2C

As O2C processes scale, manual credit evaluation becomes increasingly inconsistent, time-intensive, and difficult to govern. Different analysts apply varying judgment, data remains fragmented across systems, and decisions are often based on outdated financials, introducing risk into every stage of the order-to-cash cycle.

To address this, businesses are shifting to automated credit management solutions that standardize decision-making through predefined policies, real-time data, and integrated workflows. This enables faster credit approvals, improves risk visibility, and ensures consistency across customer portfolios, without increasing operational overhead.

More importantly, automation transforms credit management from a reactive checkpoint into a proactive control function within O2C, supporting both revenue growth and risk mitigation.

Feature

Manual Credit Management

Automated Credit Management

Decision Speed

Delayed due to manual reviews and approvals

Real-time or near real-time decisioning

Accuracy

Varies based on analyst judgment and data quality

High, driven by standardized rules and models

Risk Control

Limited visibility and reactive monitoring

Policy-driven with continuous risk tracking

Scalability

Constrained by team capacity

Easily scales across large customer portfolios

Data Utilization

Fragmented across systems

Unified, real-time data integration

Consistency

Inconsistent across teams and regions

Standardized across all decisions

Templates

Choose the Right Vendor for Credit Management

Use our Excel scorecard to make smarter, data-driven vendor decisions and reduce bad debt by 20%.

How HighRadius Can Help Businesses Streamline Credit Management Processes?

HighRadius Credit Management helps finance teams automate credit decisioning, standardize risk evaluation, and gain real-time visibility into customer exposure. By combining AI-driven scoring with automated workflows, it enables faster approvals, reduces manual effort, and improves control over credit risk.

With AI-based blocked order management, you can auto-predict blocked orders based on the customers’ credit limit utilization and payment history. You can leverage AI-based release or partial payment recommendations for faster credit decisions, reducing the need for manual intervention.

With real-time credit risk analysis software and credit decisioning software, you can receive alerts for any changes in your customers’ credit profile and make data-driven credit decisions from unlimited credit reports. Our software integrates with your ERP system and can start monitoring your customers in just 30 days.

We offer configurable credit scoring software and approval workflows that can be customized based on geography, customer segments, business units, and other factors. You can fast-track credit approvals through complex corporate hierarchies, making the credit application process more efficient and streamlined.

Our highly configurable online credit application allows you to onboard customers across the globe with multi-language, customized credit applications embedded on your website. You can automatically capture financials, personal guarantees, and check bank references, reducing the need for manual data entry.

Our software also automatically extracts credit data from over 40+ global and local agencies, including credit ratings, financials, and credit insurance information. You can configure the auto-extracted data in your preferred currency, making it easier to analyze and interpret.

Learn more about HighRadius’ Credit Management Software

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Improve onboarding time for your new customers with fully completed credit applications, tailored to your customer branding & requirements.

Credit Workflow Management

Reduce bad debt with a prioritized worklist of high-impact customer accounts demanding immediate attention.

Credit Agency Integration

Identify risky customers by getting alerts on mergers and bankruptcies from credit agencies.

FAQs

1. What is credit management in order-to-cash?

Credit management in the order-to-cash (O2C) process involves assessing customer creditworthiness, setting credit limits, defining payment terms, and monitoring risk before approving orders. It ensures revenue is protected while enabling smooth order processing and timely cash flow.

2. What role does credit management play in the O2C cycle?

Credit management acts as a control point in O2C, determining whether a customer order can be approved based on risk. It influences onboarding speed, order fulfillment, invoicing accuracy, and collections efficiency, directly impacting cash flow and bad debt levels.

3. What are the 5 C’s of credit management?

The 5 C’s of credit management are Character (credit history), Capacity (ability to repay), Capital (financial strength), Collateral (assets pledged), and Conditions (economic and industry factors). Together, they help businesses evaluate credit risk and make informed lending decisions.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.