Remote Deposit Capture 2.0: Next Generation Remote Deposit Capture

This e-book will walk you through the options for processing checks on the parameters of processing cost, check float reduction and resource requirement.

Remote Deposit Capture 2.0: Next Generation Remote Deposit Capture

To address the challenge of traditional Remote Deposit Capture, companies have started using traditional RDC in conjunction with Artificial Intelligence enabled cash application, in what has been termed as RDC 2.0. RDC 2.0 integrate remote check deposit with straight-through cash application.

RDC Integrated with Cash Application

Step 1. Scanning Unlike traditional RDC scanners, RDC 2.0 is able to scan checks and remittances together in one batch. Each batch is capable of scanning up to 100 checks at one go. Once the checks get scanned, the solution captures data with high accuracy and precision with its inbuilt Magnetic strip based MICR capture and OCR based data capture. Step 2. Transmission of the enriched file With the scanned data, the solution creates an enriched electronic file consisting of the payment details in a bank-compatible ICL (Image Cash Letter) format for transmission to banks. The solution also creates a processed electronic index file of the payments received for internal cash application. This omits the need to key-in payment data by the analysts into a spreadsheet. Step 3. Real-time cash application

Step 1. Scanning Unlike traditional RDC scanners, RDC 2.0 is able to scan checks and remittances together in one batch. Each batch is capable of scanning up to 100 checks at one go. Once the checks get scanned, the solution captures data with high accuracy and precision with its inbuilt Magnetic strip based MICR capture and OCR based data capture. Step 2. Transmission of the enriched file With the scanned data, the solution creates an enriched electronic file consisting of the payment details in a bank-compatible ICL (Image Cash Letter) format for transmission to banks. The solution also creates a processed electronic index file of the payments received for internal cash application. This omits the need to key-in payment data by the analysts into a spreadsheet. Step 3. Real-time cash application

- †The received electronic index file of the payments gets auto-matched with the scanned remittance information

- The open A/R invoice details get pulled from the supplier?s ERP system

- The payment details are individually linked with the line-items in the open A/R

- Cash gets auto-posted in the ERP

All of this happens entirely straight-through without the need for any manual intervention.

Benefits of RDC 2.0

- Straight-through process: The solution is capable of capturing checks payment and remittance accurately and handling exceptions. The solution achieves a posting hit rate of more than 95%.

- Cost-Effectiveness: RDC 2.0 is feasible for SMBs because of its high cost-savings. The areas where RDC cut costs are:

- An RDC scanner is a one-time investment and very cheap to procure. It can also be availed at monthly subscriptions instead of up-front payment.

- Expensive lockbox services. This could generate up to five-digit dollar savings.

- Costs required for resources just for keying-in data

- Transportation and manual handling costs

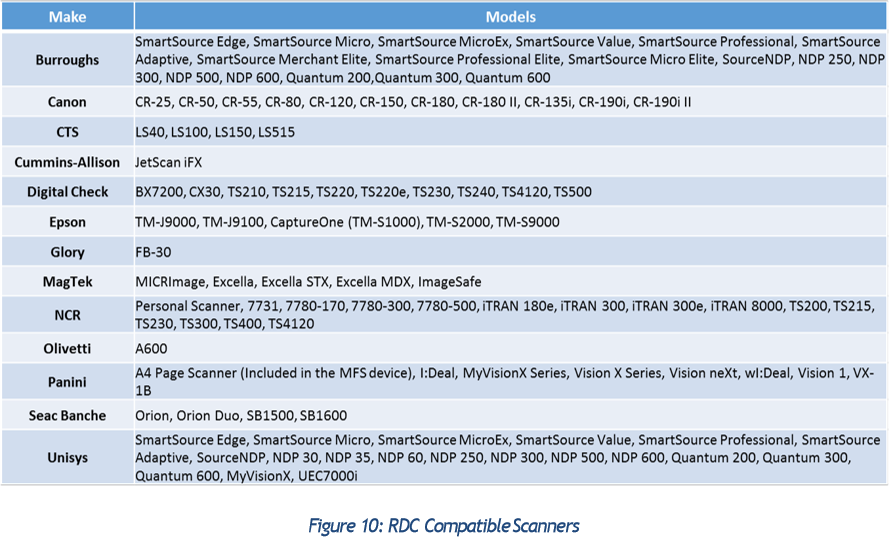

- Compatibility: Since RDC 2.0 solutions rely on the integration of regular RDC scanners with Artificial Intelligence-enabled cash application solutions, they are inherently compatible with most popular RDC scanners available on the market, including the one on your desk.

- Bank and ERP Agnostic: The solution is independent of the type of Bank or ERP the supplier uses. This enables business scaling in terms of operations and geographies.

- Real-time Cash Application: The moment the checks hit the company, they get scanned, processed and posted into the ERP

RDC 2.0 – Speed, Cost and Resource Requirement Analysis

Speed

Everything happens in real-time. As soon as the checks are scanned, they are deposited in the bank and processed for cash application and posting.

Cost

It eliminates the costs required for lockbox services, or for in-house data keying-in and manual reconciliation of payments and remittances, resulting in big savings.

Resource Requirement

It is a straight-through process, providing end-to-end automation, thereby enabling your team to focus on high-impact work across credit and collections.

Recommendations