Effective Cost of Robotic Process Automation Could Be 10x More Than You Think

- 3-10 times is the extent to which Robotic Process Automation cost can increase owning from the implementation of third-party software

- ~50% of the Robotic Process Automation projects fail due to unsatisfactory ROI

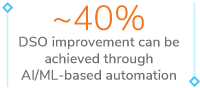

- ~40% DSO improvement can be achieved through Artificial Intelligence/ML-based automation

The Effective Cost of Robotic Process Automation is Realized During Implementation and Could Lead to Technical Debt

In recent times, RPA has been popularly hailed as the next-generation technology that will revolutionize SSCs, promising benefits, such as ‘bot for every desktop.’ To some extent, RPA has been successful in automating routine and repetitive human tasks, including scanning information, storing and updating customer data, approving customer orders, and validating payments.

RPA is considered low-cost, flexible, and easy to deploy, however, it only offers a rule-based automation and lacks intelligence and decision-making capabilities needed for complex and varying situations in real-time. RPA’s limitations could make it a liability in the long term, increasing the overall cost of adapting to the automated process that only solves a part of a problem instead of addressing end-to-end O2C processes. This is evident from the following examples:

- RPA may require additional support from third-party software, such as, AI or ML, which adds to the cost of RPA, which can increase by 3 – 10 times12. For Example, RPA can be used to pull in data and documents using web

aggregation from various sources, such as TPM, carrier portals, and customer portals for deductions analysis, but it cannot validate a deduction. That is where native AI-workflows can be used to analyze the deduction and identify the invalid deductions upfront

- RPA technology can fail to do the required task even if there is the slightest of variations in the predefined process. Consider an example of a paper-based invoice reconciliation process. A bot can analyze an invoice only if it is first digitized or scanned, which requires another digital technology or human intervention. Moreover, if the invoice format has fields placed in different areas or the cheque line items are interchanged compared to the set rule, the bot may interpret the information incorrectly

- RPA is not a self-learning solution. So, it will continue to repeat the same tasks unless a manual change in the programming is made to adapt to evolving processes. This results in a reduced shelf life of the deployed solution. For example, with growing digitization, customers are adopting various payment modes in addition to traditional wire transfers or credit card payments. The RPA technology defined and deployed for the payment reconciliation process will need an overhaul to make it compatible with these changing modes

Al and ML-based Automation Offers More Intelligent Solutions for the Order-to-Cash Process

a payment for the first time, using the account of person ‘B.’ On the next payment again, B’s account was used. So, in the future, AI can predict and expect that payment will be from B’s account, but an RPA solution cannot generate this insight or take a decision based on this information.

- Credit Management

- AI can be used to automate complex tasks, such as assessing the creditworthiness of customers, establishing new links between data and evaluating cases based on past trends, and enabling credit controllers or decision-makers with data-backed insights on credit risk

- AI-driven automation can measure credit risk across business units by identifying the common high-risk customers. As the risk increases, the consequent reduction in the exposure to business can be measured

- AI finds application in proactive credit reviews as it can process both large sets of structured and unstructured data. An AI-enabled system could consider both, internal and external, factors to get a micro and macro-economic view of a customer’s account. Then, it could automatically set the credit review period and trigger credit reviews for troubled accounts. This lets the credit team know about a stressed account even before an incident happens. This way, the A/R, credit and sales team can work in tandem to drive recovery and collections from such identified at-risk accounts

- AI goes a step further to automate the entire credit review process and predicts with a certain level of confidence the probability of an order getting blocked. There are several machine learning algorithms to predict blocked orders but one of the most reliable ones is the learning algorithm, such as regression and classification, which rely on Decision Trees and Random Forest methods. These algorithms are specifically suited for the prediction of blocked orders as they can achieve high classification performance with a set of decision trees that grow using randomly selected subspaces of data. This way, the collections and cash application teams can proactively act to see that orders that should not be blocked are taken care of

- Cash Posting: Cash posting exception process can be automated through machine learning that reads the existing patterns of manually handling exceptions, since ~80% of the exceptions are repetitive

- Collections and Disputes: AI-based deductions can proactively predict the validity of disputes and fast-track the recovery rate of invalid disputes by triggering an automated workflow to collectors, notifying them about the invalid deductions. This enables collections’ teams to focus specifically on valid deductions and spend time on reducing write-offs

- Billing: Automation can create an integrating billing process in which data from different processes can be leveraged, such as contractual discounts or historic payment patterns. Also, these patterns can be analyzed to establish credit terms

- Reconciliations: Automation with machine learning capability can create an automated cash application process that can reconcile unstructured data and different payment formats. Further, automation can predict a customer’s preferred payment method to speed up the reconciliation process

Therefore, AI/ML-based automation results in better visibility and clarity across all the O2C processes. Unlike RPA, this not only makes the O2C activities more streamlined and efficient but also generates real-time insights that the stakeholders can use to generate business value. For example, credit risk insights help a sales representative specifically focus on customers at risk of order blocks and similarly, a collections representative gets a better clarity about prioritizing customers for payment collection.

Recommendations for Finance & Technology Leaders to Capitalize on AI/ML

Most of the customers are unaware of the weakness of RPA and the potential benefits of AI- and ML-based solutions. Business leaders should focus on building the product development strategies to capitalize on the opportunity:

- Solutions With Ready-to-use, Industry Best-practice Workflow for a Specific Business Process: Having knowledge of good and bad business processes of one’s organization and its external partner’s business can be an advantage. Communication should emphasize that solutions incorporate industry best-practice workflows that

- Integrated ML Models that Enhance the Solution’s Ability to Process Complex Workflows: To differentiate from simple RPA workflows that use simple “if, then” logic, finance and technology leaders must highlight prebuilt ML models that improve business outcomes as they learn more about the customer. To differentiate from complex RPA workflows that integrate third-party ML models, messaging should focus on lower bundled costs, simpler maintenance and better usability. Concerns about data privacy should be minimized by informing customers that the ML model is auditable. This way, customers have transparency on what the solution is learning and how this benefits them

Case Study: The AB InBev AI-driven Success

AB InBev, a global brewer, with operations in 15 countries in Europe, wanted to digitally transform its operations as the existing operations were complex, siloed, and used different languages, sales channels, and payment methods. The company was using the SAP ERP platform to manage its O2C processes, but it did not provide complete visibility of the process and easy collaboration between various O2C teams. The existing automation process focused mainly on replacing manual processes but was unable to generate real-time insights to enable business discussions. Also, the sales team, the collection team, and customers faced issues related to visibility across the process and could not derive any intelligent insights. For example, the collections team had a list of slow-paying customers, but they did not know whom to prioritize, or whether it is a one-time payment issue or a habitual payment pattern.

The company wanted to transform its credit management and collections landscape in Europe by setting up location-based credit policies as it did not have any policy to control the customer overdue. The company had already undergone two phases of process transformation via the SAP ERP platform:

- In the first phase, the company established an O2C SSC, covering three locations, by establishing the credit and collection teams that developed credit policies for the company. However, the company did not witness any significant change in its operations due to high commercial losses and overdue deductions. To maintain the cash flow, it accessed the credit risk of the customers and defined credit limits and policies for new customers. It also benchmarked its business units to identify the underperforming ones

- In the second phase, the company incorporated operations from other countries by establishing zones/region-based functions, such as sales and operations. The entire credit management team moved under these functions. The company was able to achieve standardization but still, there were process inefficiencies, missing real-time insights and intelligent alerts across teams and customers. Some of the concerns of the team were:

Sales Team:

- Team only had a list of escalation cases of bad paying customers. They did not have visibility over the journey of a customer to a bad paying customer that led to an increase in debt, etc.

- Lacked visibility over good paying customers to increase business with them, and credit risk of customers

Collection Team:

- Lacked visibility over on blocked orders and size of customers (small-sized vs. big-sized)

- Majority of the time was spent on follow-ups

- Manual process was needed to log all the actions taken by the team

Customer:

- Invoice copies were missing

- Contradictory information received from different departments

- Lacked information on blocked orders

Another challenge that the company faced was language dependency, which restricted the company from hiring executives based on language proficiency. It was required that the platform should remove the language dependency so that they can focus on talent rather than language.

The company decided to digitally transform its business to bring in process efficiencies by automating manual transaction processes and incorporating AI to drive analytics-based business decisions. Solutions deployed included an automated cash applications module, predictive model for order blocking, automated collections platform and AI-driven predictive deduction status and resolution, and providing end-to-end automation. This enabled departments to work in partnerships and have complete visibility of the process. It created an environment where collectors were working with the sales team by assisting them with their analysis of customers’ credit histories and potential customers to make a sale. This also helped the sales team to treat customers differently. A customer who is paying on time and has a good credit risk should be treated differently as compared to bad paying customers.

Some of the key benefits from the transformation were:

- Cost-saving through better resource utilization and decommissioning of inefficient legacy solutions

- Better employee engagement through utilizing them in analytics work rather than manual work

- Faster order block processing through AI-based automation

- Increased visibility over the process through integration of processes

- Increase in cash flow through faster processing and visibility over block orders

- Increased customer satisfaction through overall process improvisation

The above eBook was just a glimpse out of an extensive Thought Leadership Whitepaper titled:

Future of Shared Service Centers for Order-to-Cash

Key Highlights of the Whitepaper

- SSCs for O2C have evolved to become a part of the core business operations and play a critical role in the overall digital transformation of businesses.

- 70% of digital transformations fail due to lack of discipline, visibility and tracking of business outcomes and KPIs.

- The best-in-class approach includes adopting digitization as a part of the DNA with continuous improvement and benchmarking.

- RPA was good while it lasted but the next generation technology is AI-native.

- Cloud-based integrated O2C platforms are digitally transforming SSCs.

Recommendations