Dynamic Scoring for Credit Review

How Fortune 1000 companies and SMEs automate credit and accounts receivable operations to improve productivity and reduce DSO and past-due A/R.

Dynamic Scoring for Credit Review

In the previous section, we discussed how inappropriate assignment of credit limits to new customers could lead to higher bad-debt and DSO. This section is about problems associated with the credit review process for existing customers. Credit analysts are assigned hundreds to thousands of accounts for reviewing credit limits, onboarding new customers, and unblocking blocked orders. Since reducing credit risk exposure is the responsibility of the credit team, credit review processes need to be airtight. However, the sheer volume of accounts makes it impossible for credit teams to successfully cover all accounts which are due for periodic reviews. Constantly chasing the backlog of accounts means that credit analysts are often unable to focus on conducting a focused and accurate credit analysis.

3.1. Top Challenges in the Credit Review Process

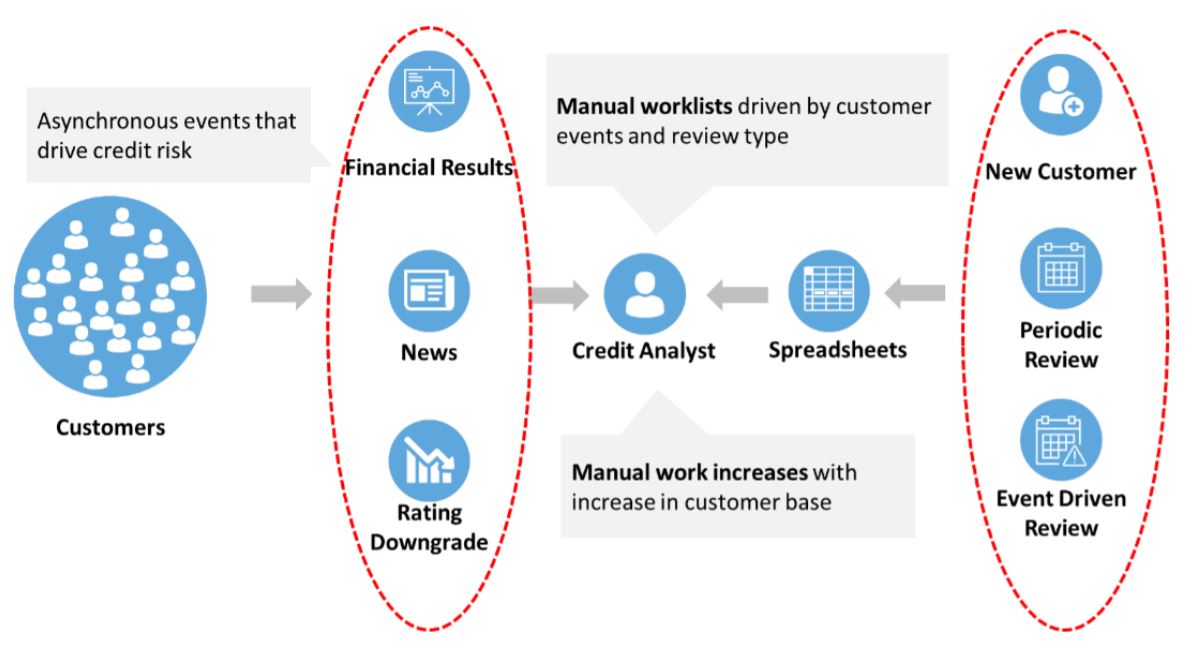

Only after an objective analysis can a credit manager make an informed decision about extending credit or continuing the existing credit to the customer. While inconsistency in periodically reviewing existing customer credit lines is an issue, asynchronous events such as financial results, rating downgrades, and M& An activity could also be responsible for escalating credit risk. Figure 4 illustrates challenges related to both asynchronous events and internal SLA requirements that create a need for credit analysts to manually prioritize accounts for credit review.

Figure 4: Challenges with a Manual Credit Analyst Driven Process

3.2. How Top Organizations Handle the Credit Review Process

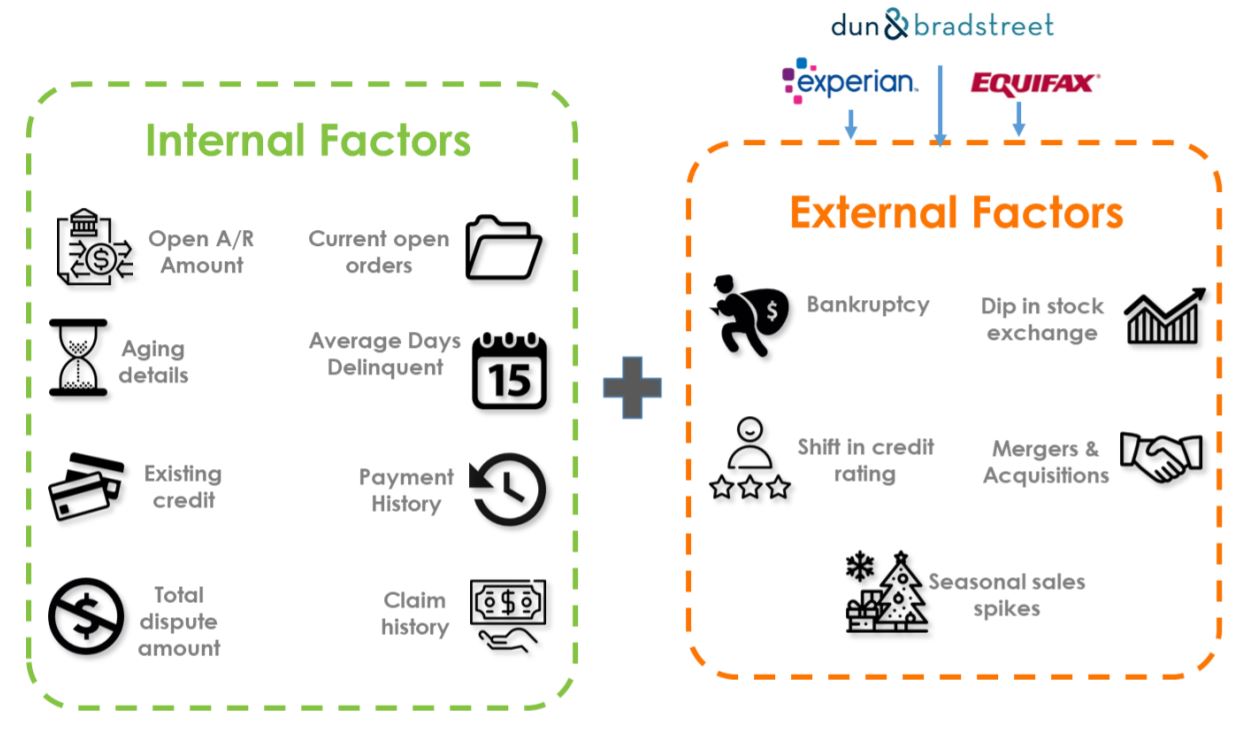

This is where best-in-class companies leverage artificial intelligence to remove subjectivity from the process and help the analysts prioritize their worklist and simplify the review by suggesting credit scores based on several internal factors (including open A/R amount, aging details, ADD, dispute amount among others) and external factors (including dip in stock exchange, shift in credit rating, seasonal spikes, M&As among others) Based on these factors, the system calculates a safe credit limit for the account and suggests it to the analyst along with all the documents used for research. Hence, empowering the analysts to make more informed decisions. At the same time, it also automates credit review for all the small customers while triggering a credit review for customers accounts with troubled financials or credit ratings.

Figure 5:Internal and External Factors Used by Artificially Intelligent System

Figure 5 illustrates what all factors are considered the dynamic credit review of a customer account.

3.3. Credit Management Success Story: TechData

Tech Data Corporation, currently ranked #108 in Fortune 500, is one of the world’s largest wholesale distributors of technology products. The credit team at Tech Data dealt with legacy systems and manual processes for credit reviews. With a large portfolio of customers worldwide, the team had to log in daily to multiple portals for each region to fetch data from credit agencies. The team automated credit data aggregation and workflows to achieve a productivity boost of 120% in the credit review process and also saved $160,000 annually through improved efficiency.

Recommendations