Discover Your Potential Savings With CFO-trusted ROI Calculator (Free)

Calculate Now- Mid-market finance teams do not face simpler problems than enterprise teams. They face enterprise-level cash application complexity without the lean AR team to absorb manual exceptions, the IT staff to run long implementations, or the mature process infrastructure to configure highly customizable automation from scratch.

- 44% of organizations still rely on little to no cash application automation. For mid-market AR teams with no headcount buffer, this is not a statistic. It is a daily operational constraint.

- The reason mid-market teams fall behind on automation is rarely budget. It is the time and resource cost of implementation. Pre-built ERP integrations for NetSuite and Microsoft Dynamics 365 are not a feature. They are what makes automation viable at this scale.

- HighRadius serves both mid-market and enterprise finance teams. The same AI-powered platform that processes millions of transactions for Fortune 500 companies is purpose-built to deploy without months of customization for a lean mid-market AR operation.

There is a version of cash application that actually works. Payments arrive, remittances are captured automatically, invoices are matched within seconds, and your accounts receivable (AR) team reviews only the edge cases that genuinely need human judgment. The corporate cash position is visible in real-time, and the month-end close passes without an all-hands scramble.

For many finance leaders, that reality feels out of reach.

- Mid-market teams often assume this level of automation belongs exclusively to global enterprises with massive IT budgets and armies of shared services personnel.

- Enterprise teams frequently discover that despite their seven-figure budgets and large headcounts, legacy automation solutions (like basic OCR and rigid rules engines) keep breaking under the weight of global payment complexity.

The truth is, complexity isn't a function of company size - it’s structural. A $150M distributor dealing with hundreds of customer portals faces the same data fragmentation as a $3B global enterprise. The difference lies not in the problem, but in the infrastructure available to absorb the damage.

This guide breaks down what makes modern cash application uniquely challenging across scales, what actually changes when you move past manual processes, and how to evaluate a cash application automation solution built for your specific organizational footprint.

What is Cash Application Automation?

Cash application automation uses technology to match incoming payments with invoices in an ERP or accounting system. It eliminates manual data entry by extracting payment data from bank statements, lockbox files, and remittance advice. It then applies intelligent algorithms to link payments with outstanding invoices. Cash application tools also handle complexities like partial payments, deductions, short-pays, and missing remittances by using configurable business rules and AI models.

This ensures that payments are posted faster, with higher accuracy, and minimal manual touchpoints. The result is a more streamlined and automated cash application process that frees up finance teams to focus on strategic tasks rather than clerical reconciliation.

What Are The Steps In The Cash Application Process?

Cash application is a critical process in managing accounts receivable and cash flow. It involves matching incoming payments with open invoices to ensure accurate and timely posting of payments. Cash application teams receive checks, ACH, wire, or card payments and match those payments with the outstanding invoices to mark them as paid.

However, this seemingly simple process can be complicated and error-prone due to several factors, such as incomplete or inaccurate remittance advice, discrepancies between payment amount and invoice amount, and deductions taken from payments.

Here are the six major steps that cover the cash application process flow:

- Aggregating Payment and Remittance Data

Gathering payment notifications from banks while simultaneously collecting remittance details trapped in emails, PDF attachments, and customer portals. - Linking of Payment & Remittance

Pairing disconnected bank line items with their corresponding remittances. This is a manual "detective" process that currently consumes 27% of analyst time. - Matching Payments to Open Invoices

Verifying that the payment amounts align perfectly with specific open line items in your ERP to ensure accounts are accurately credited. - Identifying & Coding Deduction

Investigating short-payments or discounts and applying the correct internal reason codes to ensure the ledger reflects why the full amount wasn't paid. - Handle Exceptions

Researching missing invoice numbers or unidentified senders to resolve "unapplied cash" and clear the "stop signs" in the reconciliation workflow. - Posting Cash to the ERP

The final transfer of verified, clean data directly into your ERP system to align your aging report with your actual bank balance in real-time.

Why Should Businesses Automate Cash Application?

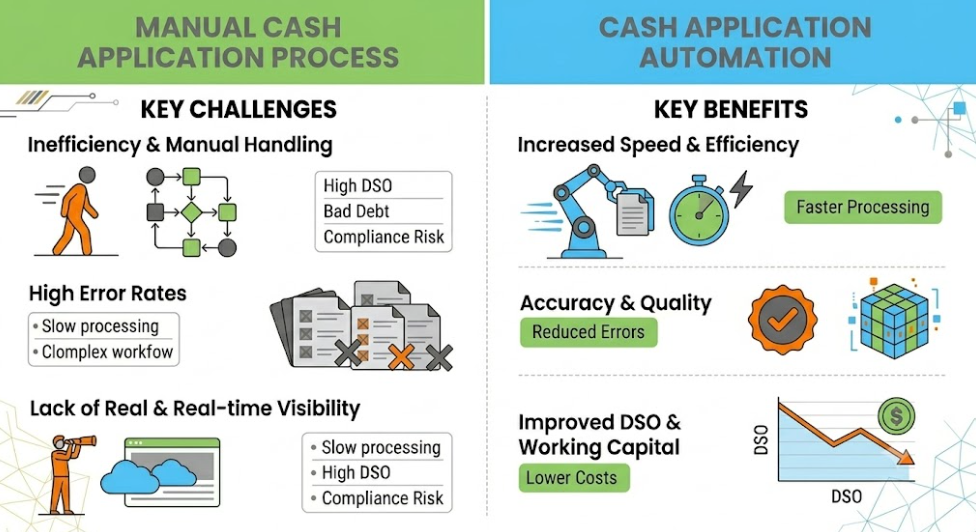

Automating the cash application process can bring significant benefits to organizations in terms of efficiency, accuracy, and cost savings. Manual cash application processes can be time-consuming and error-prone, leading to delays in posting payments and strained relationships with customers.

Additionally, organizations end up spending a lot on FTE costs, processing fees for third-party vendors, or bank lockbox key-in fees, making cash application an expensive process.

Don’t Let Manual Cash Application Drain Your Team’s Potential

See how modern finance teams achieve 90%+ automation in cash application with AI agents.

See Agents in Action1. The Remittance-to-Payment Data Gap

The most common hurdle is the lack of "clean" data for matching. While payments hit the bank via ACH or Wire, the remittance advice is often decoupled, arriving separately via email bodies, PDF attachments, or customer A/P portals. Manually aggregating these unstructured sources to identify which invoices are being settled is a repetitive task that prevents same-day cash posting.

2. High Volume of Unidentified Payments and MICR Failures

When a payment arrives without a recognizable MICR (Magnetic Ink Character Recognition) match or a valid customer reference, it falls into the "Unidentified Cash" bucket. Without cash application automation, analysts must manually cross-reference bank details with historical data or search customer portals to solve the mystery, leading to a growing backlog of unposted funds.

3. Manual Deduction Coding and Short-Pay Research

When a customer takes a trade discount or makes a short-payment, the straight-through process grinds to a halt. Analysts must stop to investigate the discrepancy and manually map the customer’s reason code to your internal ERP deduction codes. This research-heavy task is often the primary reason for a delayed month-end close.

4. Sub-ledger Latency and Re-keying Errors

Manual posting is inherently slow, creating a "data lag" in your A/R Sub-ledger. This latency means your records don't reflect the bank balance in real-time. Furthermore, manual data entry into the ERP increases the risk of transcription errors, which eventually require time-consuming course corrections during bank reconciliation.

5. Low Straight-Through Processing (STP) Rates

A manual workflow is limited by the speed of human review. Without an automated cash application, your STP rates remain low because every "exception", like a missing invoice number or a penny difference, requires a person to touch the file. Automation allows you to move to exception-based processing, where only the truly broken files need human eyes, while everything else posts touchlessly.

How does cash application automation work?

Cash application automation transforms the manual, error-prone task of matching payments into a touchless, high-speed digital workflow. The process follows 5 critical steps:

Step 1: Autonomous Remittance Capture

Cash application system autonomously extract data from 500+ portals, unstructured emails, and digital check images. This converts messy attachments into structured digital records, eliminating the need for manual data entry.

Step 2: Real-Time Bank Integration

The system pulls electronic bank feeds and lockbox files to identify incoming payments the moment they arrive. This ensures every credit signal is immediately available to be paired with its corresponding remittance.

Step 3: AI-Powered Multi-Way Matching

The engine performs a multi-way match between captured remittances, bank payments, and open invoices in the ERP. It identifies complex payment patterns, achieving a higher straight-through processing rate without human intervention.

Step 4: Intelligent Exception Management

For mismatches or short payments, AI provides pattern-based recommendations and automatically codes deductions. This replaces manual research, allowing analysts to resolve complex exceptions with a single click.

Step 5: Instant ERP Posting

Validated matches are posted directly to the ledger, closing open invoices and instantly refreshing customer credit lines. This provides real-time cash visibility and ensures the sub-ledger is always accurate.

Automated cash application can reduce operating costs by streamlining cash posting steps and eliminating the need for manual data entry, reconciliation, and fetching. With more than 95% straight-through cash posting rates, businesses can reduce their processing costs and improve their bottom line.

Why Businesses Are Adopting Cash App Automation in 2026

The shift toward digital AR automation has accelerated as companies face increasing transaction volumes and tighter working capital goals. In 2026, businesses can no longer afford the inefficiencies of manual processes.

According to recent market studies, over 70% of enterprise and mid-market companies are investing in AR automation, with cash application as a top priority. Companies report up to 80% faster invoice-to-cash cycles and 40–60% reductions in manual workload after adopting cash app automation system.

Beyond efficiency, the future of cash application automation lies in predictive intelligence, systems that not only match payments but also forecast potential exceptions, blocked orders, and customer payment trends. This makes cash application automation a must-have for CFOs and AR leaders aiming to stay competitive in 2026 and beyond.

Is Your Cash Application Process Leaking Capital?

Use this Excel-based ROI calculation template to quantify your potential savings through automated cash application.

Calculate ROI EstimateHow Cash Application Automation Impacts Cash App Teams' KPI?

CFOs are prioritizing implementing cash application system to accelerate cash flow, reduce errors, and free finance teams for strategic work. Automated cash application helps cash app team improve following KPIs:

1. Straight-Through Processing (STP) Rate

This is the "no-touch" metric. It measures the percentage of payments that match and post to your ERP without any human intervention.

The Impact: Most manual teams have an STP impacted by manual cash app process. With automated cash application, that number usually jumps to 90% or higher. This means 9 out of 10 payments post themselves while your team is still having their morning coffee.

2. Time to Post (The Same-Day Goal)

This tracks how long it takes from the moment money hits the bank to when it is actually applied to the customer’s account in the ERP.

- The Impact: In a manual setup, it’s common for payments to sit for 2–3 days while the team searches for remittances. Automation enables same-day cash posting, ensuring your Aging Report is always an accurate, live reflection of what is actually owed.

3. Unapplied Cash Volume

This is the total amount of money sitting in your "suspense" or unidentified accounts because it couldn't be matched to an invoice.

- The Impact: High unapplied cash makes month-end a nightmare. Automation uses AI to identify MICR matches and suggest the right reason codes for short-pays. This keeps the unidentified queue small and ensures the "mystery" payments don't pile up.

4. Cost Per Payment Processed

This is the total cost (bank fees + team labor) of processing a single check or ACH payment.

The Impact: Manual posting is expensive because of high bank "key-in" fees and the hours spent on data entry. By removing those bank fees and allowing your team to handle much higher volumes without extra help, the cost to process each payment drops significantly.

Why Cash Application Scales Differently (But Hurts the Same)

Most vendor content treats mid-market and enterprise cash application as entirely different sports. In reality, they are the same sport played on different field sizes. The underlying operational headaches like, missing remittances, deduction coding, and fragmented payment rails are identical.

1. Mid-Market Complexity: High Nuance, Zero Cushion

There is a persistent assumption that mid-market cash application is just a "simpler" version of enterprise AR. It isn't. A $200M consumer packaged goods (CPG) company processing trade deductions from major retailers faces the exact same deduction coding mess as a Fortune 500 brand.

What the mid-market lacks is the human cushion. Enterprise organizations can distribute exceptions across a large shared services center. Mid-market teams typically rely on two or three analysts who simultaneously handle remittance capture, collections calls, dispute resolution, and ERP troubleshooting. When processes are immature and growth outpaces headcount, manual cash application quickly consumes the team's entire day.

2. Enterprise Complexity: The Multi-ERP and Global Rail Matrix

For the enterprise, the problem isn't a lack of bodies; it’s the sheer volume of data and system fragmentation. Following years of mergers, acquisitions, and global expansion, a typical enterprise environment is a patchwork of disparate systems running instance of legacy SAP in Europe, Oracle in North America, and NetSuite for a newly acquired subsidiary.

At this scale, cash application teams are choked by:

- Global Payment Rails: Reconciling localized payment methods alongside cross-border SWIFT and SEPA formats.

- Massive Web Portal Scraping: Manually logging into dozens of different customer vendor portals daily to download decoupled remittance advices.

- Governance and Compliance: Maintaining bulletproof audit trails and strict internal controls across multiple regional business units.

3. Native ERP Limits: Why NetSuite, Dynamics, SAP, and Oracle Fall Short

Whether you are running a mid-market ERP like NetSuite or Microsoft Dynamics 365, or an enterprise tier-1 system like SAP S/4HANA, native cash application logic is fundamentally limited.

Most ERPs rely on rigid, rule-based matching. They function perfectly when a payment arrives with a clean, standard remittance referencing a single invoice. They break down completely when a customer pays across dozens of invoices, takes an unearned short-pay, or remits through a third-party portal with a reference format your ERP doesn't recognize.

The result? High-value analysts end up acting as human middleware, manually keying data to bridge the gap between bank files and the General Ledger.

The True Cost of Manual Cash Posting

The operational drag of manual processing impacts corporate finance teams differently depending on their organizational maturity:

The Mid-Market Drain: Bank Key-In Fees & Hidden Leakage

For growing mid-market companies still anchored to lockbox services, bank key-in fees are an immediate, non-trivial line-item cost. Banks typically charge anywhere from $0.50 to $2.00 per item to manually key remittance data from checks and PDFs. At a few thousand payments a month, this represents direct margin leakage that modern automation completely eliminates.

The Enterprise Drain: Shared Services Friction & Working Capital Lag

For the enterprise, the cost is measured in Days Sales Outstanding (DSO) and organizational velocity. When cash application takes 48 to 72 hours to post, credit lines remain locked unnecessarily. Collectors waste time calling customers who have already paid, damaging key client relationships. Meanwhile, the shared services center must continually scale headcount just to keep up with linear transaction growth.

What Actually Changes: Before vs. After Automation

Cash application automation shifts your accounts receivable function from a reactive, backward-looking data entry operation to an exception-based accounting workflow.

| Operational Metric | Before Automation | After Automation (Mid-Market) | After Automation (Enterprise Global Shared Services) |

| Morning Cash Routine | 2 to 4 hours of manual downloads and data matching. | 15 to 20 minutes spent reviewing local edge cases. | Exception-only queues routed automatically by business unit or language. |

| Unapplied Cash Balance | Stagnates and grows throughout the month. | Cleared systematically within 24 hours. | Near-zero balances across multi-currency accounts globally. |

| Month-End Close | A 3-to-5-day manual reconciliation crisis. | Continuous, real-time posting simplifies close to hours. | Sub-ledger reconciliation completed seamlessly across all global ERP instances. |

| Direct Costs / Resource Allocation | Heavy bank key-in fees; analysts buried in manual input. | Lockbox key-in fees eliminated; lean team pivots to proactive collections. | Shared services headcount optimized; manual FTE capacity reallocated to high-value dispute resolution. |

| ERP Data Velocity | 24 to 48-hour data lag across the business. | Real-time cash visibility for cash forecasting. | Instantaneous global visibility into working capital positions |

What are the best Practices for Cash Application Automation?

Achieving a straight-through processing (STP) rate north of 90% requires looking beyond technology features to focus on deployment and configuration strategy.

1. Account for Your ERP Write-Back Blueprint

The single most critical technical consideration is how automation communicates with your systems of record.

- For Mid-Market Teams: Prioritize pre-built, certified connectors for NetSuite or Microsoft Dynamics 365. Custom API development can easily derail a project if your organization lacks a dedicated corporate IT team to maintain it.

- For Enterprise Teams: Ensure iy can orchestrate multi-ERP write-backs simultaneously. The automation must be capable of clearing open items in SAP, Oracle, and legacy systems natively without creating data discrepancies across subsidiaries.

2. Standardize Remittance Ingestion Streams Upfront

Automation is only as good as the data it ingests. Before flipping the switch on a new automation, audit your top 20% of customers by transaction volume to map out how they send remittance data (e.g., email PDFs, EDI 820, or web portals). Modern automation leverage Vision Language Models (VLMs) and advanced AI to read these documents natively, removing the need for fragile OCR templates that break the moment a customer alters their billing layout.

3. Design Dynamic Exception Routing

Do not treat exceptions as an afterthought. Prior to launch, establish clear operational guardrails:

- Define exact thresholds for small-balance write-offs.

- Automate the routing of unidentified payments above specific currency thresholds directly to designated supervisors.

- Establish how short-payments are flagged so collections teams can act on disputes immediately.

Why Cash Application Automation is a Pain for CPG Industries?

Consumer packaged goods (CPG) and manufacturing companies face a distinct cash application challenge: high-volume trade deductions.

When a major retailer pays a CPG supplier, they rarely pay the full invoice amount. The payment arrives short, accompanied by a complex remittance detailing promotional allowances, slotting fees, shortages, or compliance penalties.

Standard cash application automation often stumbles here, simply matching the cash and leaving the remaining balance as an open, unapplied item. A truly robust automation goes further:

- Captures deduction reason codes directly from the retailer's remittance sheet or portal.

- Maps those external retailer codes to your company’s internal ERP reason codes.

- Executes Split-Posting: Posts the cash to clear the base invoice while simultaneously creating a structured deduction claim file, routing it to your disputes team for resolution day one.

Why HighRadius is a Good Fit for both Mid-Market and Enterprise Finance Teams?

A common question finance leaders ask is whether a unified platform like HighRadius can effectively serve both the agile mid-market and the complex global enterprise.

The answer lies in how the core AI architecture is deployed. HighRadius handles the cash application needs of global Fortune 500 corporations while offering a highly accelerated, out-of-the-box deployment model designed specifically for mid-market finance departments.

The Underlying Engine is Identical: Whether you are a three-person AR team running NetSuite or a global shared services operation running a multi-instance SAP landscape, you leverage the exact same AI agents for remittance capture, payment matching, and exception resolution.

The variation lies entirely in deployment scope:

- The Mid-Market Framework: Leverages pre-built ERP connectors (NetSuite, Dynamics 365), pre-configured workflow best practices, and an implementation scope engineered to deliver immediate time-to-value without consuming internal IT hours.

- The Enterprise Framework: Accommodates highly customized, global multi-ERP clearing workflows, cross-border localized configurations, sophisticated parent-child customer hierarchies, and enterprise-grade compliance governance.

By anchoring your cash application on an enterprise-grade AI foundation tailored to your team's size, you ensure your technology infrastructure scales effortlessly alongside your business, eliminating manual bottlenecks today while future-proofing your cash operations for tomorrow.

Frequently Asked Questions (FAQs) for Cash Application Automation

1. What is cash application automation for mid-market companies?

Cash application automation for mid-market companies is the use of AI and machine learning to automatically capture remittance data, match incoming payments to open invoices, and post cash to an ERP without manual intervention for the majority of transactions. For mid-market finance teams typically running 2 to 5 AR professionals on NetSuite or Microsoft Dynamics, automation converts a daily 90-minute manual process into a 15-minute exception review. The challenge for mid-market teams is not that automation is unavailable to them. It is finding an automation that deploys without the IT resources and implementation infrastructure that enterprise deployments assume. Hi

2. How long does it take to implement cash application automation for a mid-market team?

For a mid-market company with a single ERP environment and standard payment volumes, implementation using a automation with pre-built ERP connectors typically takes 4 weeks. This compares to 4 to 6 months for complex enterprise multi-ERP deployments. The primary variable is ERP integration method: pre-built certified connectors for NetSuite and Dynamics 365 compress timelines significantly versus custom API integrations that require dedicated IT resource. Companies that complete a remittance audit and configure exception routing rules before go-live consistently achieve higher first-month straight-through processing rates.g

3. Does mid-market cash application face the same complexity as enterprise?

Yes, in most of the ways that matter operationally. Mid-market companies receiving payments from hundreds of customers across ACH, wire, check, and multiple customer portals face the same remittance fragmentation as enterprise AR teams. CPG and distribution companies at $200M to $500M revenue face the same deduction complexity as their Fortune 500 counterparts. What differs is not the complexity of the problem but the resources available to manage it: smaller IT teams, less mature processes, and no dedicated implementation staff. This is why the right cash application automation for a mid-market team must be designed to work within those constraints, not assume they do not exist.

4. Can HighRadius cash application automation work with NetSuite or Microsoft Dynamics 365?

Yes. Modern cash application automation including HighRadius integrate directly with NetSuite and Microsoft Dynamics 365 via certified pre-built connectors. For mid-market teams, the critical validation questions are whether the integration is pre-built or custom, how the automation handles ERP write-back errors, and how close to real-time the ERP is updated after a payment is matched. An automation that requires custom API development to connect to your ERP is a significant resource commitment for a mid-market IT team and should be treated as a project cost in your evaluation, not a standard implementation step.

5. What is the difference between cash application automation for mid-market vs. enterprise?

The underlying technology is the same: AI-powered remittance capture, payment matching, and ERP posting. The operational complexity faced is also more similar than most vendor content acknowledges. The differences are in deployment scope and infrastructure assumptions. Enterprise cash application automation involves multi-ERP environments, global payment rails, multi-currency reconciliation, and hundreds of customer portal connections, with a dedicated IT team and implementation resources to match. Mid-market automation is configured for a single ERP environment, with pre-built connectors and a faster implementation timeline that does not require internal project resourcing to execute. Outcome metrics including straight-through processing rate and analyst productivity improvement are comparable across both segments.

6. Is HighRadius suitable for a mid-market company with a small AR team?

Yes. Mid-market companies with 2 to 5 AR professionals and $100M to $1B in revenue use the same AI-powered cash application automation as Fortune 500 companies, configured for their ERP, transaction volume, and remittance mix. For a 3-person AR team, the most significant day-one impact is the elimination of the morning remittance-to-payment linking routine: the task that currently consumes the majority of analyst time before any actual cash posting begins. Deployment uses pre-built NetSuite and Dynamics 365 connectors, which means implementation does not require custom integration work or dedicated IT project resources to complete.