Customer Onboarding and Credit Approval Process

How Fortune 1000 companies and SMEs automate credit and accounts receivable operations to improve productivity and reduce DSO and past-due A/R.

Customer Onboarding and Credit Approval Process

Customer onboarding is the first and one of the most important steps to reduce DSO. Most organizations ignore this step and take the word of the sales representatives or the customers to decide on credit limit assignments. Wrongly estimated credit limits could lead to bad-debt write-offs and high DSO.

1.1. The Credit Application Process

According to a survey by NACM 33% of organizations are pressed for time to perform due diligence on prospective customers. This is because companies typically assign credit limits based on credit agency data, financials, credit insurance, and bank guarantees. All the manual processes including paper-based credit applications, gathering data from third-party agencies including D&B and Experian and credit reviews make it increasingly difficult for credit analysts to find time and onboard new customers.

Figure 1: Current Credit Application Process

1.2. Top Challenges in the Credit Application Process

The top bottlenecks for organizations in the credit application process are:

- The volume of paper that they need to process and maintain each month

- Incomplete and inaccurate financial documents that they receive from customers

- Manual data entry into spreadsheets and ERP systems leading to errors and wastage of time

- Downloading credit reports from leading 3rd party agencies including Experian and D&B

- Calculating credit scores in excel spreadsheets

- Obtaining approvals on emails

1.3. How Leading Organizations Handle Credit Applications

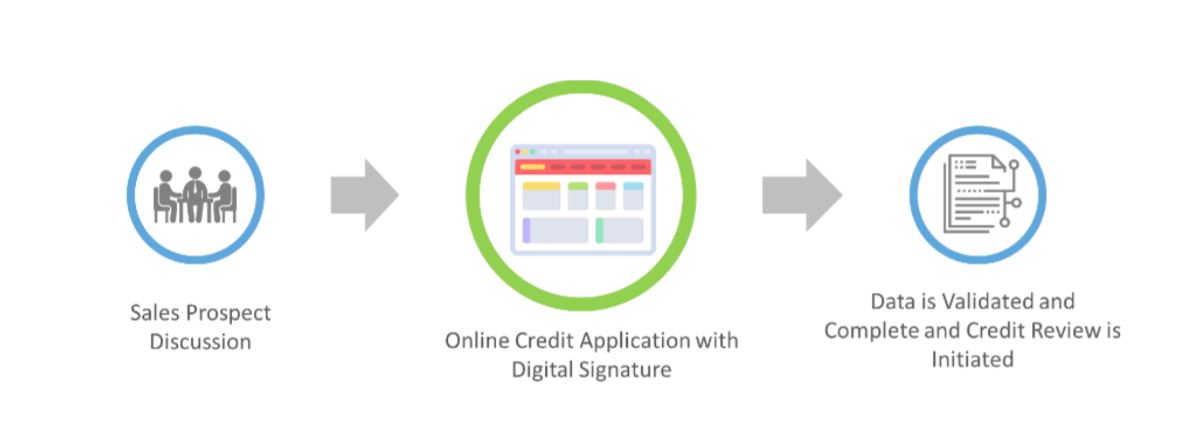

Figure 2: The Online Credit Application Process

Moving credit application online, integrating it with credit agencies and securing it with digital signature technology helps in eliminating manual work and incomplete documentation. It replaces a paper intensive credit management process with an electronic one to enable better credit portfolio and risk management and to quickly onboard new customers. Credit score and credit limits are calculated automatically while workflows are assigned to relevant credit managers to review and approve the assigned credit limits.

Figure 3: Credit Review and Customer Onboarding Process

Assigning the right credit limit to the customers helps firms to collect the payment on time thus, reducing DSO.

1.4. Online Credit Application Success Story: The adidas Group

The adidas group has about 10 different types of credit application formats which are filled by customers for requesting lines of credit from its various business divisions across geographies. In what was a very manual paper-based process, the credit team at the adidas Group took more than four days to process a single credit application. In essence, what this meant was that the credit team was mostly focused on tactical activities while trying to get a complete credit application rather than spending it strategically on the credit review process. The Adidas group started deploying credit applications one by one at each of their business units. After deploying the HighRadius online credit application, the team was able to bring the new customer onboarding time to less than 2 days with more than 90% credit applications received with complete data, right on the first attempt. The end result was that the team was able to review more credit applications per given while using accurate data to reduce the credit risk exposure and alleviate the risk of high DSO due to wrongly estimated credit limits.

Recommendations