Accounts receivable dashboard- Help your AR team stay on top of AR metrics

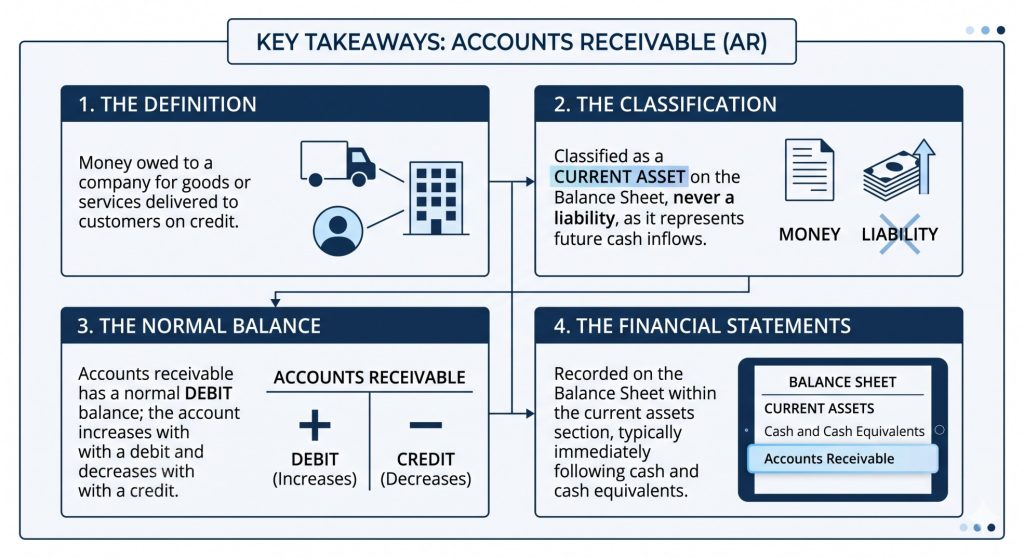

Download Now- The Definition: Accounts receivable (AR) represents the balance of money owed to a company for goods or services delivered to customers on credit.

- The Classification: AR is classified as a current asset on the balance sheet, never a liability, as it represents future cash inflows.

- The Normal Balance: Accounts receivable has a normal debit balance; the account increases with a debit and decreases with a credit.

- The Financial Statements: Accounts receivable is recorded on the balance sheet within the current assets section, typically immediately following cash and cash equivalents.

Running a business means keeping a close eye on the cash flow. But what happens when you make a sale, deliver the goods, and agree to let your customer pay you 30 days later? That money hasn't hit your bank account yet, but it's still legally yours. In the accounting world, that waiting period is where accounts receivable comes into play.

Whether you're a small business owner trying to decode your financial statements or a student brushing up on accounting principles, this guide will walk you through exactly how to handle and classify this essential account.

If you are planning to improve your cash flow by reducing AR, you can check out HighRadius Accounts Receivable (AR) Automation Software, which helps businesses automate their end-to-end AR process, ultimately reducing DSO by over 10% and significantly improving cash flow.

What is Accounts Receivable?

Accounts receivable is the balance of funds owed to a company by its customers for goods or services that have been delivered or used but not yet paid for.

When a business extends credit to a buyer, allowing them to receive products or services immediately and pay at a later date, the outstanding transaction amount is recorded in the accounts receivable account. This practice facilitates B2B (business-to-business) commerce by enabling continuous operations without requiring immediate cash settlements for every transaction.

Accounts Receivable Meaning & Definition

An account receivable can best be defined as a legally enforceable claim for payment held by a business against its customers for goods supplied or services rendered.

The standard accounts receivable meaning revolves around the extension of a short-term line of credit to a buyer. These credit agreements operate on specific payment terms - such as Net 30, Net 60, or Net 90 days - dictating the exact timeframe the customer has to settle the invoice.

What Type of Account is Accounts Receivable?

Accounts receivable is an asset account, specifically categorized as a current asset within the general ledger.

To clarify common classification questions:

Is Accounts Receivable an Asset?

Yes, accounts receivable is an asset. It is recorded as an asset because it represents a guaranteed, legal right to collect future cash, which adds tangible economic value to the business.

Is Accounts Receivable a Current Asset?

Yes, accounts receivable is a current asset. In financial accounting, an asset is designated as "current" if it is expected to be converted into cash, sold, or consumed within one year or a single standard operating cycle. Because standard invoice terms require payment within 30 to 90 days, accounts receivable is highly liquid.

Is Accounts Receivable a Liability?

No, accounts receivable is never a liability. A liability represents an obligation or money that a company owes to external parties (such as loans or unpaid vendor bills). Because accounts receivable represents money owed to the company, it functions as the exact opposite of a liability.

Accounts Receivable on the Balance Sheet

On the balance sheet, accounts receivable is positioned in the upper section under the "Current Assets" category, usually directly below "Cash and Cash Equivalents."

The accounts receivable balance sheet entry reflects the total outstanding invoices owed to the business at a specific point in time. Frequently, it is reported as "Accounts Receivable, Net," indicating that the total figure has been adjusted to account for an Allowance for Doubtful Accounts (an estimate of invoices that may ultimately go unpaid).

Is Accounts Receivable a Debit or Credit?

Accounts receivable has a normal debit balance. Because it is an asset account, it increases with a debit and decreases with a credit.

When determining if accounts receivable is a debit or credit for a specific transaction, standard double-entry bookkeeping rules apply:

- Debit accounts receivable when a new sale is made on credit, which increases the total asset balance.

- Credit accounts receivable when a customer pays their outstanding invoice, which decreases the total asset balance.

Accounts Receivable Journal Entries & Accounting Entries

Accounts receivable accounting entries require a debit to the accounts receivable account when a sale is made on credit, and a credit to the account when the customer pays the invoice.

Below are the standard accounts receivable journal entries for the two primary stages of the billing lifecycle.

1. Recording a Sale on Credit

When a company provides $5,000 worth of services to a client on Net 30 terms, the revenue must be recognized and the asset created.

| Date | Account Name | Debit ($) | Credit ($) |

| MM/DD | Accounts Receivable | 5,000 | |

| Service Revenue | 5,000 |

- Impact: Current assets increase by $5,000 (debit), and revenue increases by $5,000 (credit).

2. Recording the Customer's Payment

When the client sends a $5,000 wire transfer 30 days later, the business must record the cash inflow and remove the outstanding receivable.

| Date | Account Name | Debit ($) | Credit ($) |

| MM/DD | Cash | 5,000 | |

| Accounts Receivable | 5,000 |

- Impact: The cash account increases by $5,000 (debit), and the accounts receivable balance decreases to zero (credit).

Accounts Receivable Optimization Via Tools

Accounts receivable automation software is a digital platform that streamlines and automates the entire process of invoicing, tracking, and collecting payments from customers.

As businesses scale, manually tracking hundreds of journal entries, sending payment reminders, and reconciling bank transfers becomes prone to human error and delays. Implementing an AR automation solution (like HighRadius) helps finance teams by:

- Reducing Manual Entry: Automatically matching incoming payments to open invoices (cash application).

- Accelerating Cash Flow: Sending automated dunning emails and payment reminders to reduce Days Sales Outstanding (DSO).

- Predicting Bad Debt: Utilizing AI to assess credit risk and predict which customers are likely to default on their payments.

Frequently Asked Questions (FAQs)

1. What is accounts receivable is it an asset?

Accounts receivable is an asset. Specifically, it is a current asset that represents future cash inflows owed to a company by its customers for goods or services purchased on credit.

2. What are some accounts receivable examples?

Common accounts receivable examples include a landscaping company billing a corporate client for monthly services on Net 30 terms, or a wholesale manufacturer delivering inventory to a retail store with payment due in 60 days.

3. What is accounts receivable on a balance sheet?

On a balance sheet, accounts receivable is a line item listed under the Current Assets section. It shows the total aggregate amount of unpaid customer invoices that the company expects to collect within the next 12 months.

4. What is Accounts Receivable position?

The accounts receivable position is the current total balance of a company’s outstanding, unpaid invoices at a specific point in time. Monitoring this position is critical for assessing a company’s cash flow and collection efficiency.

5. What is accounts receivable in accounting?

In accounting, accounts receivable is the general ledger asset account used to record, track, and manage all short-term credit extended to customers. It acts as the central record for who owes the company money and the amount owed.

6. What is accounts receivable assets or liabilities?

Accounts receivable falls strictly under assets. It is not a liability. Assets represent items of value owned by the company (the right to collect cash), whereas liabilities represent debts owed by the company to others.

7. What Is accounts receivable debit or credit?

Accounts receivable is an asset account with a normal debit balance. According to accounting principles, you debit the account to increase its balance and credit the account to decrease its balance.

8. What is accounts receivable vs accounts payable?

Accounts receivable is money owed to a company by its customers (classified as a current asset). Accounts payable is money the company owes to its suppliers or vendors (classified as a current liability).