Discover Your Potential Savings With CFO-trusted ROI Calculator (Free)

Calculate Now- Manual cash application slows down working capital optimization by creating delays in payment matching, reconciliation, and ERP posting.

- AI-powered cash application automation improves productivity by eliminating manual remittance aggregation, invoice matching, and exception handling

- Faster and more accurate cash posting directly improves collections efficiency, customer experience, and downstream AR operations.

- HighRadius enables touchless cash application through AI-driven OCR, remittance capture, ERP integration, and automated invoice matching.

- Automation-driven cash application transformation can significantly reduce operational costs, improve DDO, and accelerate cash posting at scale.

In today’s uncertain economic climate, finance teams can no longer afford to operate reactively. The organizations that are pulling ahead are the ones shifting their cash application operations from manual, transactional work toward strategic decision-making.

This blog helps you understand the role of technology in eliminating manual, tedious tasks, improving FTE productivity, and applying cash faster.

- Understand the challenges of the manual cash application process

- The role technology plays in streamlining the cash application process

- Leverage AI in Cash Application- what is it and some real-life use cases

What Is Cash Application?

Cash application is the process of applying incoming payments to the appropriate customer accounts in an accurate and timely manner. In simple terms, it is the process of matching the payments received from customers to the invoices or outstanding balances they are intended for.

Cash application involves verifying the payment details, such as the amount and the customer’s account information, and then recording and allocating the payment accordingly. This process helps maintain accurate and up-to-date financial records and allows for effective management of cash flow within a business.

Example:

For instance, in a B2B environment, let’s consider the scenario where Penta Corp purchases goods on credit from ABC Corp. ABC Corp delivered the goods or services to Penta Corp last month on credit. As part of the credit purchase, ABC Corp provided an invoice, which serves as the original bill for the payment. Now, suppose Penta Corp submits a payment today along with the remittance.

A cash application specialist utilizes the remittance advice to determine which invoices are being paid using the funds transferred by the buyer, considering Penta Corp’s regular credit purchases. Let’s delve deeper into the cash application process flowchart to understand the challenges involved and how an automated cash application solution like HighRadius helps tackle them.

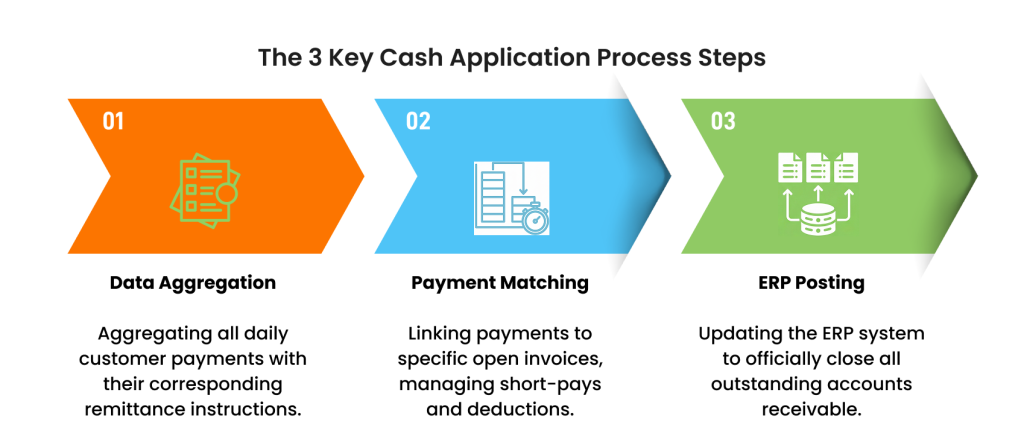

Steps Involved in the Cash Application Process

To ensure efficient and accurate processing, the cash application team typically follows specific internal controls established by cash application leaders. The typical cash application process cycle includes the following steps:

Step 1: Payments and Remittances Aggregation

Payment from customers comes with remittance advice, indicating which invoice(s) the payment is for. Payments can be made through checks or electronic methods (such as ACH, credit cards, SEPA, BACS, etc.), with remittances sent separately through email, EDI, or A/P portals. Remittance slips list invoice numbers, dates, and relevant information, including discounts taken by the customer.

Step 2: Invoice Matching and Deduction Coding

Once the payment is received, cash application analysts proceed to match the payments with their corresponding open invoices. However, even with the remittance attached, this process can be complex. A single payment may cover multiple invoices or not precisely match the amount of any invoice due to factors such as short payments, discounts, or issues related to the order. In such cases, the accounts receivable team investigates further to ensure accurate allocation and resolution.

Step 3: Cash Posting to the ERP

Once invoice matching is done, cash is applied to the ERP, and open AR is closed. Without an integrated system, manual posting involves Excel and ERP, risking inefficiencies and errors.

Cash Application & Working Capital

Cash Is King- Now More than Ever!

It may sound cliché, but it holds true: cash is king and will continue to reign supreme. While cash application may appear as a back-office, Excel-based process, its significance in optimizing working capital cannot be underestimated. In today’s dynamic business landscape, working capital is paramount for CFOs who consistently face CEO inquiries, such as: “What is the current state of our working capital?” Now, let’s delve deeper into the critical connection between cash application management and working capital.

The answer is simple: Faster cash application results in working capital optimization. That’s why daily cash application is essential to ensure that every payment is promptly applied and accurately reflected in the books as cash inflows. By diligently managing cash applications, businesses can maintain a healthy flow of working capital, enabling greater financial stability and growth.

Challenges That the Cash App Analysts Face

In many organizations, cash application within accounts receivable (A/R) is a labor-intensive process. Analysts heavily rely on Excel sheets to carry out their daily cash application entries. Unfortunately, manual cash application activities not only result in reduced productivity but also impact the overall cost aspect of A/R operations. Now that we have gained an overview of the cash application process let’s delve into the challenges commonly encountered in this crucial process:

- Lockbox Fees Leading to a Higher Cost of Doing Business

Bank lockbox services collate all the checks from a customer in a single place, reducing the check float time. Lockbox teams process every check and key in the information in an electronic file shared with the cash application team. Lockbox key-in services are charged based on keystrokes. However, considering that they charge $1-3 per check, cash application becomes an expensive process.

Moreover, sometimes the lockbox key-in data is incomplete, and analysts fill in the missing information manually by going through the scanned check images. Apart from the high lockbox key-in fees, it requires several man-hours to re-process a check processed by the lockbox services.

- Manual Payment-Remittance Linking

For electronic payments, customers typically send remittances through emails, EDI, or A/P (Accounts Payable) portals. However, matching these remittances with incoming payments can be time-consuming and prone to errors.

Cash application teams are required to manually extract or download remittances from different sources, often in various file formats, and then map them to the corresponding payments. This manual effort not only reduces the efficiency of cash application analysts but also increases the risk of mistakes.

- Manual Invoice Matching and Exception Handling

Cash application analysts are responsible for manually matching invoices with payments based on the information provided in the remittance, such as invoice numbers, purchase orders, or shipment details. However, this process can be challenging when the remittance contains incorrect or truncated invoice numbers, making it difficult for analysts to match invoices with payments accurately. In such situations, payments are often applied at an account level rather than the individual invoice level.

Additionally, there are instances where customers fail to include the necessary remittance advice, requiring cash application analysts to proactively reach out to customers to request the missing information. These types of exceptions, along with countless others, result in delays in cash posting daily.

- Short Payments and ERP Posting

One of the most common issues that most cash application analysts frequently encounter is short payments, such as trade promotions, early payment discounts, or disputes regarding goods. When customers send the remittance, they typically indicate the reason for the short payment. However, cash application analysts must manually identify these short payments and accurately map the customer-specific reason codes to the specific reason codes used in their ERP system. Only after this mapping can they proceed to post the cash to the ERP system.

Complicating matters further, many companies utilize multiple ERP systems, including SAP, JD Edwards, Microsoft, or legacy systems, each with its own unique configurations. Consequently, analysts must effectively handle exceptions before posting them to the ERP system to ensure accurate and timely processing.

- Downstream Impact on Collections

One of the critical challenges associated with slow cash application is its negative impact on other accounts receivable (AR) processes, such as credit and collections.

For example, when payments are not applied on the same day they are received, a collector may not be aware that the customer has already made a payment and might mistakenly contact the customer with an incorrect dunning notice. This not only results in a poor customer experience but also creates unnecessary confusion and frustration.

Benefits of Automated Cash Application

- Elimination of 100% lockbox key in fees: Leverage technology to auto aggregate noise free and accurate checks.

- Apply cash faster and accurately: With the auto-aggregation of remittances and automated invoice matching, cash app teams can apply cash faster.

- Improved analyst productivity: Cash app teams can eliminate tedious manual tasks and instead focus on high-value tasks like exception handling and recovering faster.

- Better team collaboration: With real-time insights and data, cash app teams can better collaborate with deductions teams for short payments. Collections can also reach out to customers who have raised invalid disputes.

What Does An Autonomous Cash Application Process Look Like?

With the HighRadius Cash Application tool, you can achieve 90% straight-through cash posting. Sounds intriguing, right? Let us understand how that is possible.

Use Case 1: Automated Remittance Aggregation

- AI-based E-Mail Remittance Capture: The touchless E-Mail Processing Module automatically reads and extracts relevant remittance information from email bodies and attachments. The solution can read all attachments type, like Excel, CSV, pdf, word, etc. It can read emails in 20+ languages.

For example, customers may attach a pdf copy of the entire statement when they pay the previous month’s invoices, and the solution can read the invoice and payment information from the statement’s tabular format.

- AI-based Check Remittance Capture: The multiple Optical character recognition (OCR) engines read information from every check received. It then assembles them into a tabular structure. It identifies the invoice information like Invoice numbers, Amounts Paid, etc., and also classifies rows into Invoices being paid vs. other data such as subtotals and deductions/discounts.

For example, A Customer could include a line in the check saying “Apply to Invoice 90937432(109.12), 90965411(800.03)” in the check stub, and the system would recognize the two invoices based on the past invoice reference patterns.

- Aggregate Remittances from Websites & Customer portals: This module automates the process of retrieving remittance information hosted on portals by certain large Customers like Walmart, Target, etc.

For example, Walmart pays for 100s of invoices in a single payment. They allow users to export remittance data into Excel from their website. The electronic data capture module can extract the relevant information and any deductions to post the payment automatically.

Use Case 2: AI-Powered Invoice Matching

HighRadius offers various pre-built algorithms that can match invoices to remittances based on several parameters, including Invoice#, PO#, Item#, and Part#, etc. Through AI, the system can also identify situations where Customers provide only a portion of the Invoice # (such as the last seven digits of a ten-digit invoice#).

For example, Invoice Numbers of Clients follow a set pattern, such as 12-digit numbers beginning with 900. Customers may exclude ‘900’ and only provide the last nine digits, which is typically insufficient for ERPs. Through our algorithms, the solution can match the right invoice and share the full invoice number with the ERP.

Use Case 3: Remote Deposit Capture

Apply cash directly for checks by directly submitting to the office location through Remote Deposit Capture(RDC) machines or scanning via mobile apps.

Use Case 4: Integration with Collections to Handle No-Remittance Scenarios

This Highradius module helps you identify no-remittance scenarios and better collaborate with the collections and deductions teams. The Cash Application Cloud integrates with Collections Cloud to scan all open payment commitments to consider them as potential remittances.

Customer Case Studies- Cash application process transformation

We have successfully led numerous cash application transformation projects for order-to-cash organizations spanning various regions and industries. Now, let’s examine a specific case study to gain a deeper understanding of how our expertise can benefit you.

How Danone Reduced Overall Costs by 75% While Delivering an Exceptional Customer Experience – A Shared Services Success Story

About Danone

Danone is a global consumer goods provider founded in Barcelona and now headquartered in Paris. This industry-leading multinational corporation has a customer base of more than 1000+ food distributors, consisting of both small mom-and-pop stores and major retailers like Walmart and Amazon. With similar global businesses moving towards a shared services approach for their operations, Danone was already a step ahead – preemptively identifying the biggest obstacles it would face in the transformation of its shared services and coming up with a plan on how to manage these challenges best.

Setting Up a Shared Service Center (SSC): Understanding the Challenges

Establishing an SSC requires a lot of thought and meticulous planning for several variables, be it infrastructure, budget, policies, etc. While the primary motivation for establishing an SSC is to reduce costs, organizations often inadvertently increase their overall expenses thanks to inefficiencies, poor planning, and other unexpected challenges.

Now, let’s explore some of the main challenges that organizations commonly face when adopting a shared services approach.

Multiple Processes and File Formats

For businesses like Danone, which have operations in multiple countries, an SSC often utilizes different service providers in each country for various functions such as scanning, banking services, e-invoicing portals, and ERP systems. This is primarily because most providers do not operate globally.

However, the lack of global operation from these providers results in a lack of standardization across multiple lines of business (LOBs). This inconsistency in processes is particularly evident in supplier payments and invoicing, where different formats are required based on the specific ERP system or country involved. As a result, businesses require an agile and streamlined process that seamlessly integrates with their ERP systems across different geographies.

Inability to Track KPIs for Business

With siloed systems in place across multiple LOBs and different geographies, there is often a lack of visibility, which is necessary for global control and governance. Businesses need a single source of truth for tracking KPIs to identify focus areas for improvement.

Poor Customer Experience

With most global businesses operating under a typical shared services model, prioritizing cost reduction over customer satisfaction has only led to diminished customer retention. The inability of A/R teams to partner across their organization and interact or work with each other in real-time results in a poor customer experience over the long run.

Danone Shared Services – Before HighRadius

Danone’s shared services enterprise faced several challenges related to redundancy. Before automation, almost 100% of Cash, Collections, Credit, and Deductions work was performed manually. That meant the analysts had to go through the entire cash application process with precision to handle specific errors.

- Increased Process Complexity

- Payment formats were mainly electronic fund transfer (EFT), automated clearing house (ACH), and Wire Transfer, meaning a significant amount of dollars came in electronically. Some payments, however, were also accepted through checks, which contributed to almost 5% of the total dollar amount, leaving EFTs as nearly 95% of the total share.

- Danone had multiple lockboxes spanning various geographies. While electronic payments were fast to receive, processing them was an entirely different story – as there were more than 25 portals in use for collecting remittances. From the portal itself, the cash analyst had to capture valuable information on remittances, such as decoupled payments. Sometimes the remittance came in separately through emails. Sometimes, it came in through electronic data interchange (EDI) files and regular bank file formats.

- Remittance aggregation and payment linkage, along with code deduction and manual input into the SAP system, led to several shortcomings.

- This entire process consumed almost 128 hours per week for processing electronic payments and 140 hours for checks.

- Delay in cash posting with dispute identification and resolution caused customer dissatisfaction.

- With the A/R team spending most of their time in cash processing, dispute identification, and resolution, the collections process at Danone took a hit. Danone had no automation in place for its collections. As a result, the analysts dealt with mundane, repetitive tasks, including customer segregation and creating promises-to-pay (P2Ps), rather than focusing on at-risk accounts that required dunning.

- Working Capital Bottlenecks like Increased Days Deductions Outstanding (DDO)

At Danone, the majority of disputes (85%) were caused by trade promotion deductions, and all of them had to be handled manually. Out of these deductions, 90% were found to be valid, requiring significant manual effort to identify and process the remaining 10% that were invalid. The absence of automation led to delays in resolving deductions, resulting in a deduction dispute resolution time (DDO) of over 45 days.Danone’s Need for AutomationDanone was looking for a technology partner with an intelligent solution that was easily deployable and customizable with the flexibility to integrate with their existing systems.The objective behind automation was:

- To increase accuracy and efficiency while improving inspection of A/R operations

- To improve the transient speed at which A/R is processed and, in turn, improve cash handling

- To counter any costs incurred during manual processing or low value-added activities

- Multi-ERP and Bank File Integration: The solution integrates their multiple ERPs and all bank file formats.

- Email Parsing: The solution automatically parses emails and their attachments to collect and process remittance information.

- Optical Character Recognition (OCR): The solution has a distinct AI-enabled OCR feature, automatically extracting remittance information from paper images.

- Web Aggregation Capability: The solution also has a web-based technology to log in to website portals to download and obtain remittance information.

- Automatic EDI Parsing: The solution can parse all formats of EDI files, including EDI 823, EDI 820, 812, bank BAI, and BAI2 formats.

- Real-time Payments: The Cash Application Cloud within the solution allowed for real-time payments with no lag, therefore increasing the cash posting rate for Danone by 95% within 90 days of implementation.

- Code Deduction Management (Deductions Cloud): The solution identifies, matches, and applies code deductions with specific reason codes. The cloud solution also seamlessly integrated with their existing ERP solutions to trigger invalid deduction workflows for collectors, helping them recover more than $6 million.

- 75% Reduction in Overall Costs

- 25% Reduction in Days Deductions Outstanding (DDO)

- 100% Touchless Cash Posting

- $5.9M Recovered Post SSC Creation in Canada within 5 months

- Smooth ERP Integration with Existing Systems

Generating a 75% Increase in Productivity with HighRadiusDanone partnered with HighRadius to automate their end-to-end A/R setup, integrating the siloed systems they had in place. With the first phase of implementation in North America resulting in a noticeable reduction in overall costs as well as improved revenue and working capital impact, Danone expanded its scope to its six SSCs in Europe.The key features constituted:

Danone Shared Services – After HighRadius Solution ImplementationThe challenges of manual and error-prone cash applications, which had negative impacts on downstream processes such as deductions and collections, have been completely eliminated.With HighRadius’ cloud solutions, Danone achieved the following results:

Frequently Asked Questions (FAQs)

1. What is the cash application process?

1. What is the cash application process?

The cash application process is the process of matching incoming payments from customers to their corresponding open invoices and recording them in your accounting system.

It typically involves three steps:

-

- Collecting payments and remittances from checks, ACH, wire transfers, and customer portals

-

- Matching payments to invoices using remittance details such as invoice numbers, purchase orders, or payment amounts

-

- Posting the payment to your ERP to close open balances and update your accounts receivable records

When done accurately and on time, cash application ensures your financial records reflect the true state of your cash flow and keeps downstream processes like collections and dispute management running smoothly.

2. What are the most common challenges in the cash application process?

2. What are the most common challenges in the cash application process?

The biggest pain points tend to be manual remittance aggregation across multiple sources, difficulty matching payments to invoices when remittance data is incomplete or incorrect, managing short payments and deduction coding across different ERP systems, and the downstream impact on collections when cash is not posted on time. Together, these challenges reduce team productivity and increase the cost of running accounts receivable operations.

3. How does automation improve the cash application process?

3. How does automation improve the cash application process?

Automation removes the manual effort involved in aggregating remittances, matching invoices, and posting cash to your ERP. AI-powered solutions can read remittances from emails, portals, EDI files, and scanned checks, then match them to the correct invoices automatically. This reduces processing time significantly, minimizes errors, and allows analysts to focus on exception handling and higher value tasks rather than repetitive data entry.

4. What are the core cash application best practices for finance departments?

4. What are the core cash application best practices for finance departments?

To maintain high data integrity and healthy cash flow, teams should adopt these cash application best practices:

- Maintain a Daily Application Schedule: Applying cash on the same day it is received prevents “unapplied cash” from bloating the balance sheet and ensures collectors have accurate data.

- Standardize Reason Codes: Use a uniform set of codes for deductions and short-payments so that Sales and Collections can easily understand why a balance remains open.

- Centralize Remittance Data: Encourage customers to send all payment advice to a single, dedicated email alias to prevent lost information across different personal inboxes.

- Establish Clear Over/Short Policies: Define a “tolerance limit” (e.g., $10 or less) where small discrepancies are automatically written off rather than spending manual hours investigating minor cent differences.

- Cross-Departmental Feedback Loops: Regularly share reports with the Sales and Credit teams regarding “mystery payments” to help improve the quality of information received from customers at the source.