Cash Conversion Cycle: What Is It, How to Calculate, and Improve It

2 April, 2024

18 minute read

Nimisha Ghosh, B2B Finance Content Strategist

N

Nimisha Ghosh

Nimisha specializes in Order-to-Cash (O2C) transformation, crafting strategic narratives at the intersection of B2B SaaS and FinTech. With over four years of experience, she brings deep expertise in electronic invoicing, receivables automation, and digital payments, translating complex autonomous finance capabilities into actionable insights for modern finance leaders. When she’s not analyzing trends in enterprise finance, Nimisha enjoys reading and traveling. Her approach to writing is rooted in clarity, precision, and a strong understanding of real-world financial challenges.

Last updated: 13 July, 2026

Identify Inefficiencies & Reduce Costs in Cash Application Process Instantly.

The biggest challenge most businesses often face, especially in these dynamic economic conditions, are related to cash flow. A lack of cash flow stifles growth and can even lead to business failure. Cash conversion cycle (CCC) is a key metric that organizations need to pay attention to if they aim to improve their company’s financial health and cash flow. At its core, the CCC is a measure of a company’s operational efficiency. By managing the CCC effectively, companies can optimize their working capital and improve their overall financial performance.

In this blog post, we will cover the cash conversion cycle in detail, including its formula and calculation. We will also provide real-world examples of how the CCC is used in different industries, and strategies for improving your company’s CCC. So, let’s dive in.

Table of Contents

Introduction

What is Cash Conversion Cycle (CCC)?

How to Calculate the Cash Conversion Cycle?

Cash Conversion Cycle Formula

Cash Conversion Cycle vs Operating Cycle

Cash Conversion Cycle Example

Why Is the Cash Conversion Cycle Important to a Business?

Cash Conversion Cycle Interpretation: What is a Good Cash Conversion Cycle?

Common Mistakes in Cash Cycle Analysis

How to Improve Your Cash Conversion Cycle?

How Automation Can Revolutionize Business's Cash Conversion Cycle?

How HighRadius Can Help?

What is Cash Conversion Cycle (CCC)?

The cash conversion cycle (CCC), also known as the cash cycle, measures the length of time it takes for a company to convert its production and sales investments into cash. This metric aids businesses in improving cash flow and profitability by expediting inventory turnover.

CCC is a critical measure of a company’s financial performance, and is used by businesses of all sizes to track how quickly they are able to sell their inventory, collect cash from customers, and pay their suppliers

Learn More about HighRadius’s Accounts Receivable Software

Lower DSO, boost working capital, and increase productivity with our AI-driven accounts receivable platform, integrated with modern ERPs.

Accelerate payment recovery from delinquent customers and boost cash flow through automated collection workflows.

Cash App

Achieve same day cash application with automated remittance aggregation

Credit

Mitigate credit risk, reduce bad debt, and streamline customer onboarding with AI-powered insights.

Deductions

Reduce Revenue Leakage with AI Prediction models that identify valid and invalid deductions.

How to Calculate the Cash Conversion Cycle?

Are you wondering how to calculate the cash conversion cycle (CCC) for your business? Understanding the calculation and the cash conversion cycle formula can help you gain valuable insights into how efficiently your company is managing its working capital and generating cash flow from sales.

The CCC covers three stages of a company’s sales cycle – current inventory sales, cash collection from the current sales, and payables for outsourced goods and services. CCC can be calculated using three working capital metrics, and each of these metrics holds valuable insights into what is happening within the business.

The three metrics are:

Days Inventory Outstanding (DIO) Days Inventory Outstanding measures the average number of days it takes for a company to sell its inventory. It indicates how efficiently a company is managing its inventory and turning its assets into revenue. Essentially, DIO measures how quickly a company is able to convert its inventory into sales.

DIO = (Average Inventory/Cost of Goods Sold) X Number of Days

Days Payable Outstanding (DPO) Days Payable Outstanding is a financial metric that measures the average number of days it takes for a company to pay its invoices from trade creditors or suppliers. This metric is crucial for evaluating a company’s cash flow management and assessing its ability to meet its financial obligations. Essentially, DPO indicates how long a company takes to pay its suppliers and manage its working capital effectively.

DPO = (Accounts Payable/Cost of Goods Sold) X Number of Days

Days Sales Outstanding (DSO) Days Sales Outstanding is the financial metric that measures the average number of days it takes for a company to collect payment from customers after making a credit sale. The metric is crucial for the company’s financial health; it signifies how good a business is at recovering its past dues. Essentially, DSO indicates how effectively a company collects cash from customers who make purchases on credit.

DSO = (Accounts Receivable/Total Credit Sales) X Number of Days

Cash Conversion Cycle Formula

The formula for calculating the cash conversion cycle (CCC) is:

Cash Conversion Cycle = DIO + DSO – DPO

Where DIO stands for Days inventory outstanding, DSO stands for Days sales outstanding, DPO stands for Days payable outstanding.

Cash Conversion Cycle vs Operating Cycle

While the Cash Conversion Cycle outlines how cash is tied up in operations, it is often confused with Operating Cycle. The two metrics are closely related, but they measure slightly different aspects of a business’s cash flow efficiency. Understanding the distinction can help finance leaders make more informed decisions about working capital management.

Operating Cycle

The operating cycle measures the total time it takes for a company to convert its inventory purchases into cash from sales. It focuses on the entire process from acquiring raw materials, producing goods, selling them, and finally collecting cash from customers.

Operating Cycle = DIO + DSO

The operating cycle does not consider payables, which means it only tracks cash tied up in operations, not how long a company can defer payments to suppliers.

Cash Conversion Cycle (CCC)

The CCC builds on the operating cycle by factoring in Days Payable Outstanding (DPO), the time a company takes to pay its suppliers. By subtracting DPO from the operating cycle, CCC measures the net time cash is tied up in the business.

CCC = DIO + DSO – DPO

A shorter CCC indicates that the company recovers cash faster, improving liquidity and reducing reliance on external financing.

A longer CCC suggests cash is tied up for extended periods, which could strain working capital.

Operating cycle focuses solely on the time to turn inventory into cash, cash cycle provides a fuller picture by factoring in how long the company can delay payments to suppliers. This provides a clearer view of cash flow efficiency and working capital management, showing the net duration for converting operational investments into cash

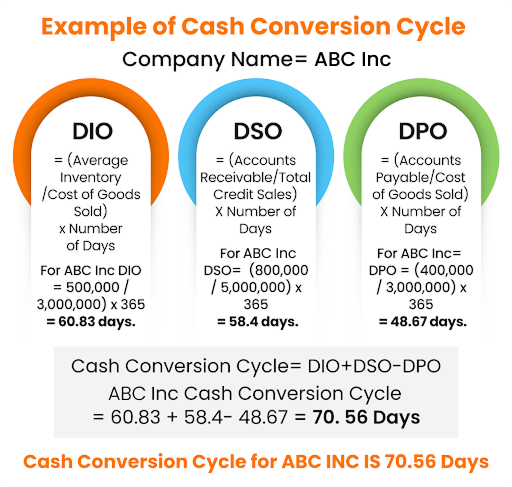

Cash Conversion Cycle Example

Now, let’s take an example to simplify the process of calculating the cash conversion cycle. Consider a company called ABC Inc., which operates in the bicycle manufacturing industry and aims to calculate its cash conversion cycle. To begin, the company must determine its days inventory outstanding (DIO), days sales outstanding (DSO), and days payable outstanding (DPO).

DIO: The company’s DIO can be calculated by dividing the average inventory by the cost of goods sold (COGS) and multiplying by the number of days in the period. Suppose ABC Inc. has an average inventory of $500,000 and COGS of $3,000,000 for the year, and the year has 365 days. Then, the DIO can be calculated as follows:

DIO = (500,000 / 3,000,000) x 365 = 60.83 days.

DSO: The company’s DSO can be calculated by dividing the accounts receivable by the total credit sales and multiplying by the number of days in the period. Suppose ABC Inc. has accounts receivable of $800,000 and total credit sales of $5,000,000 for the year. Then, the DSO can be calculated as follows:

DSO = (800,000 / 5,000,000) x 365 = 58.4 days.

DPO: The company’s DPO can be calculated by dividing the accounts payable by the COGS and multiplying by the number of days in the period. Suppose ABC Inc. has accounts payable of $400,000 and COGS of $3,000,000 for the year. Then, the DPO can be calculated as follows:

DPO = (400,000 / 3,000,000) x 365 = 48.67 days.

Now that we have calculated the DIO, DSO, and DPO, we can use the CCC formula to determine the company’s cash conversion cycle. Substituting the values we calculated, we get:

CCC = 60.83 + 58.4 – 48.67 = 70.56 days.

Therefore, the cash conversion cycle of ABC Inc. is 70.56 days.

Why Is the Cash Conversion Cycle Important to a Business?

Now that we have understood the formula and calculation for the cash conversion cycle, let’s dive deeper into why it’s important for your business and how it can impact your financial health.

The cash conversion cycle helps manage the inventory. If not managed well, a company will either be short on supply or have too much of it, increasing storage costs. Apart from the inventory management and cash flow efficiencies, CCC also assists finance leaders in:

1. Determining the financial health of the company

The CCC is often used by key stakeholders to assess a company’s financial health and liquidity. A lower CCC indicates that a company is able to convert its inventory and receivables into cash quickly, which can improve its ability to meet its financial obligations and pay back business loans.

2. Improving trade credit terms with vendors

Vendors often look at a company’s CCC when deciding whether to offer trade credit. A lower CCC indicates that a company has healthy liquidity and is more likely to pay its bills on time. This can improve a company’s chances of getting better credit terms from vendors.

3. Gaining easy access to capital and loans

A lower CCC can also improve a company’s chances of getting approved for business loans. This is because a lower CCC indicates that a company has a healthy cash flow cycle and is better able to pay back its loans. This can add a sense of security for lenders and increasing approval prospects.

Cash Conversion Cycle Interpretation: What is a Good Cash Conversion Cycle?

To understand whether a company’s CCC is “good”, one needs to keep in mind that this is entirely dependent on the industry standards and how efficiently the operations of a business are managed. Generally, a lower CCC is considered a good cash conversion cycle, however, the appropriate target CCC varies by industry.

Industry Benchmarks Across Sectors

Retail: Retail typically operates on a negative CCC as their inventory turnover is quick and they usually collect payments from their customers before paying their suppliers.

Typical CCC: Often negative or very low.

Manufacturing & Construction / Capital-Intensive Industries: Manufacturing shows a positive CCC due to high inventory levels and longer production cycles. Construction projects often involve milestone-based billing, which extends the cash conversion timeline. Cash is tied up for longer periods before sales are realized.

Typical CCC: Usually higher CCC, depending on production complexity and project size.

SAAS/ Software: Since the subscription revenue is collected upfront and there is little to no inventory holdings, the CCC is usually reported very low or in negative.

Typical CCC: Often low or negative.

Consumer Goods & E-commerce: These industries have an immediate or negative CCC due to rapid sales, upfront customer payments, and delayed supplier payouts.

Typical CCC: Negative or close to zero.

While these benchmarks are excellent reference points, when setting CCC target for ones own business, it is absolutely necessary that the company’s size, market and business model be taken into consideration.

Positive vs. Negative Cash Conversion Cycle

Positive Cash Conversion Cycle: A positive CCC means the company takes longer to convert investments in inventory and receivables into cash than the time it takes to pay suppliers. This ties up working capital and may strain liquidity, especially in industries with long production cycles. However, the benefits of Positive CCC are that it reflects strong investment in inventory and customer relationships, which may be necessary to maintain product quality, service levels, or competitive positioning.

Negative Cash Conversion Cycle: A negative CCC is highly favorable, as it indicates the company collects cash from customers before it needs to pay suppliers. This creates a cash surplus, reduces reliance on external financing, and improves liquidity.

In general, a negative CCC is most common in fast-moving CPG and e-commerce businesses where products sell quickly and payments are collected upfront. A positive CCC, on the other hand, is typical for manufacturing and capital-intensive industries with longer production cycles or significant long-term investments, where slower cash conversion is the natural outcome of the business model.

A simple way to understand the trajectory of a cash conversion cycle is by using graphical interpretation, the downward and upward movement. If the CCC is in a declining trend, it denotes a positive sign, and if you observe an upward trend, it means potential inefficiencies in your order-to-cash processes.

In short, CCC is a valuable metric, but it doesn’t have a definitive good or bad score. Assess its significance within your company and its unique requirements. Additionally, monitoring cash management efficiency is the initial step to unlock your most cost-effective capital source. With understanding in hand, you can develop a plan for further improvement.

Common Mistakes in Cash Cycle Analysis

Even though the cash conversion cycle is widely used and is considered one of the most important indicators of working capital efficiency, it is often misinterpreted. Businesses rely on CCC to make decisions about liquidity, supplier negotiations, and investment planning. Any error in analyzing the metric could very easily lead to a faulty strategy (e.g., holding excess inventory, misjudging liquidity, or setting unrealistic targets). Here are the most common mistakes and what they mean in practice:

Ignoring Seasonality Looking at CCC at just one point in time can be misleading.

Why: Sales and collections often spike or dip in certain seasons.

Industry examples: Retailers see CCC shorten during holidays, while manufacturers see demand surges in specific quarters (e.g., automotive launches) that distort CCC trends. SaaS companies may see distortions during annual renewal cycles.

Overlooking Payment Terms and Discounts CCC calculations sometimes ignore supplier terms or discounts that impact cash flow.

Why: Missing these details makes CCC look worse (or better) than it really is.

Industry examples: Manufacturers with 90-day supplier terms may actually have more liquidity than their CCC shows. Retailers buying in bulk may shorten DPO if they take early-payment discounts.

Treating Industry Benchmarks as Absolute Comparing your CCC to an industry average without context can give the wrong impression.

Why: Benchmarks vary by company size, strategy, and bargaining power.

Industry examples: Amazon’s negative CCC isn’t the only ‘good model’ to follow, Walmart’s positive CCC reflects its scale and brick-and-mortar structure. Treating either as a universal benchmark would mislead businesses. Manufacturers may have higher CCCs by design because of long production cycles.

Focusing on Only One Component (DIO, DSO, or DPO) Many businesses try to optimize just one lever instead of balancing all three.

Why: Improving inventory turnover but neglecting receivables or payables can still lock up cash.

Industry examples: A manufacturer may cut inventory (DIO) but still struggle if customers delay payments (DSO). A SaaS firm may collect upfront (low DSO) but lose out if they pay vendors too quickly (short DPO).

Not Considering the Bigger Cash Flow Picture CCC shouldn’t be analyzed in isolation.

Why: A “good” or “bad” CCC means little without context of overall cash flow, costs, and financing.

Industry examples: E-commerce companies may have negative CCC but still face cash strain from high logistics expenses. Manufacturing firms may have a positive CCC but remain stable due to long-term financing.

Case Studies

Transform Your AR operations With Automation

Discover how Yaskawa transformed its accounts receivable process, reducing bad debt and past-due payments with AR automation.

To optimize your CCC, organizations need to focus on reducing DSO and DIO while increasing DPO. This involves selling inventory faster, collecting payments sooner, and extending bill payment periods. However, organizations need to remember that shortening collection cycles is not the ultimate goal; the key is to prevent customers from falling too far behind on their payments. By being proactive and preventing delinquency, businesses can improve cash flow and maintain control over accounts receivable collection, crucial for running business efficiently.

We all know that merely sending an invoice and expecting timely payments may not always be realistic. That’s why it’s important to take preventive steps to avoid delinquency from the outset. By working to keep customers from becoming significantly past due, organizations can reduce overall cycle times and ensure a consistent cash flow. Here are some key tips to help improve the cash conversion cycle:

Better payables management: Managing payables such as supplier payment terms is the key to controlling working capital. You can see positive trends in your CCC if you leverage and consolidate your spending by increasing supplier collaboration and extending payment terms.

Prioritize inventory management: Poor inventory management could lead to lower sales due to the inability to service the placed orders. Thus, inventory management should be prioritized alongside sales, profit, and payment data of the customers. Development of new relationships with customers and clients can also improve inventory management.

Empower and enable customers to pay with ease: To improve your cash conversion cycle, understand why customers delay invoice payments. Offer solutions to resolve their underlying invoice issues and disputes to reduce the risk of overdue invoices. Categorizing and prioritizing customers by size and risk profile can also be beneficial.

Ensure consistent communication: Maintain consistent follow-ups through emails and phone calls. Utilize all provided contact information, including office phone, mobile number, email address, and supervisor’s details. If there’s no response within 24 hours to a voicemail or email, consider making another call or escalating the matter to the contact’s supervisor.

Have a clear credit and payment policy: Be clear with your clients and clearly convey your payment expectations and collection procedures to them. Encourage open communication and have clients explain their payment processing procedures to work together in ensuring timely payments. This collaborative approach fosters a smoother payment process and strengthens client relationships.

Take proactive measures: Be proactive and anticipate customer needs. For example, if a customer requires an additional bill copy, send it in advance without waiting to be asked. Maximize your collections software by configuring it to automatically send transaction documents, such as invoices or proofs of delivery. This proactive approach improves the customer experience and streamlines the collection process, enhancing efficiency and satisfaction.

Call early, call often: When significant dollars are involved, calling before an invoice is past-due is an effective strategy. Making a list of those who are likely to pay late and flag their transactions for a proactive call. If an invoice goes overdue, make a call or send an email within days of the event. This approach helps in early resolution and ensures timely payments, contributing to better cash flow management.

Leverage automation: Harness the power of automation to optimize your cash conversion cycle. The efficiency of your cash conversion process directly influences working capital, cash flow, and overall financial performance. In today’s competitive landscape, relying on outdated, manual procedures can hinder growth and efficiency.

How Automation Can Revolutionize Business’s Cash Conversion Cycle?

If your business is not leveraging automation, it’s time to consider the transformative potential it can bring to your CCC. By automating critical processes such as credit management and collections, businesses can streamline their workflows, reduce manual errors, and increase efficiency. Here are some key benefits of automating these processes:

Enhanced efficiency: Automation allows businesses to prioritize customers based on their credit risk and payment behavior, enabling collectors to focus their efforts on the most critical accounts. This streamlined approach to collections enables a more efficient use of time and resources, leading to faster revenue realization and shorter cash conversion cycles.

Improved accuracy: Automated credit management systems use advanced analytics to provide businesses with real-time credit risk visibility. This enables decision-makers to make more informed credit decisions, reducing the risk of bad debt and improving overall accuracy in the credit management process. Taking analytics based credit decisions enables organizations to reduce non payment risks and improve cash conversion in the long term.

Faster dispute resolution: Automated dispute management systems enable businesses to quickly identify and resolve disputes, reducing the time it takes to resolve payment issues and improving overall cash flow.

Enhanced customer experience: Automated collections systems enable businesses to engage with customers in a more personalized and timely manner and design personalized payment options for them. This can lead to improved customer satisfaction and loyalty, as well as faster payment times.

Data-driven insights: Automated systems provide businesses with real-time insights into their collections process, enabling decision-makers to analyze performance, identify trends, and make data-driven decisions that improve overall cash conversion cycle.

How HighRadius Can Help?

Effortlessly optimizing the cash conversion cycle (CCC) ensures a smooth flow of funds and finely tuned working capital for organizations. At the core of CCC optimization lies automation, which transforms complex processes such as setting customer credit limits, inventory tracking, and collections management. By embracing automation, businesses reduce manual efforts and errors, accelerating revenue realization and enhancing cash flow. Leveraging AI and RPA technology, businesses can streamline the order-to-cash process, gaining real-time insights into collection performance.

HighRadius offers AI-driven solutions that redefine CCC optimization. The HighRadius Order to Cash Suite automates credit management, AR collections software, invoicing, cash application and dispute resolution, leading to faster revenue realization and improved cash flow. Designed to streamline workflows and enhance the customer journey, HighRadius’s O2C solutions drive financial performance, reducing DSO by an impressive 20%.

But HighRadius goes beyond automation; it empowers organizations to make data-driven decisions through AI-powered analysis. By seamlessly integrating workflows for AR teams and automating routine tasks, resources are freed to focus on high-yield endeavors, resulting in a remarkable 30% increase in productivity. With HighRadius O2C Suite, the journey towards CCC optimization is not just a destination but a testament to innovation and success.

Frequently Asked Questions (FAQs)

1. What is the cash conversion ratio?

The cash conversion ratio is a financial metric used to assess a company’s ability to convert its net income into cash flow. It measures the proportion of cash generated from operations relative to net income, indicating operational efficiency in converting profits into cash.

The cash conversion ratio is a financial metric used to assess a company’s ability to convert its net income into cash flow. It measures the proportion of cash generated from operations relative to net income, indicating operational efficiency in converting profits into cash.

2. What are the factors affecting the cash conversion cycle?

The factors affecting the cash conversion cycle (CCC) include inventory management, accounts receivable, and accounts payable. A longer inventory holding period, longer payment terms from customers, and longer payment terms to suppliers can all contribute to a longer CCC.

The factors affecting the cash conversion cycle (CCC) include inventory management, accounts receivable, and accounts payable. A longer inventory holding period, longer payment terms from customers, and longer payment terms to suppliers can all contribute to a longer CCC.

3. What is the optimal cash conversion cycle?

The optimal cash conversion cycle (CCC) varies by industry and business nature. Generally, a lower CCC is considered better as it indicates efficient management of working capital. However, the appropriate target CCC varies by industry, and businesses should aim to improve their CCC over time.

The optimal cash conversion cycle (CCC) varies by industry and business nature. Generally, a lower CCC is considered better as it indicates efficient management of working capital. However, the appropriate target CCC varies by industry, and businesses should aim to improve their CCC over time.

4. What is a negative cash conversion cycle?

A negative cash conversion cycle occurs when a company’s accounts payable period is longer than its accounts receivable and inventory turnover periods combined. This results in cash being received from sales before payments are due, improving liquidity and operational efficiency.

A negative cash conversion cycle occurs when a company’s accounts payable period is longer than its accounts receivable and inventory turnover periods combined. This results in cash being received from sales before payments are due, improving liquidity and operational efficiency.

5. What is a good cash conversion cycle?

A shorter cash conversion cycle is considered a good cash conversion cycle and indicates efficient management of receivables, inventory, and payables, which improves liquidity and operational performance. However, what constitutes a “good” cycle varies by industry and company objectives.

A shorter cash conversion cycle is considered a good cash conversion cycle and indicates efficient management of receivables, inventory, and payables, which improves liquidity and operational performance. However, what constitutes a “good” cycle varies by industry and company objectives.

6. What is cash flow conversion?

Cash flow conversion refers to the process of turning sales revenue into cash receipts. It measures how effectively a company converts its sales into actual cash inflows by managing receivables, payables, and inventory efficiently. It is crucial for assessing liquidity and operational efficiency.

Cash flow conversion refers to the process of turning sales revenue into cash receipts. It measures how effectively a company converts its sales into actual cash inflows by managing receivables, payables, and inventory efficiently. It is crucial for assessing liquidity and operational efficiency.

7. What is the cash to cash cycle?

Cash to cash cycle, also known as the cash conversion cycle, measures the time it takes for a company to convert its investments in inventory and other resources into cash flow from sales. It’s measured by adding days inventory outstanding to days sales outstanding and subtracting days payable outstanding. It involves managing accounts receivable, inventory, and accounts payable effectively to optimize liquidity.

Cash to cash cycle, also known as the cash conversion cycle, measures the time it takes for a company to convert its investments in inventory and other resources into cash flow from sales. It’s measured by adding days inventory outstanding to days sales outstanding and subtracting days payable outstanding. It involves managing accounts receivable, inventory, and accounts payable effectively to optimize liquidity.

8. What is the cash flow cycle?

The cash flow cycle depicts the movement of cash in and out of a business over a specific period. It begins with cash inflows from sales, investments, or financing, followed by outflows for expenses, investments, and debt repayment, influencing a company’s liquidity and financial health.

The cash flow cycle depicts the movement of cash in and out of a business over a specific period. It begins with cash inflows from sales, investments, or financing, followed by outflows for expenses, investments, and debt repayment, influencing a company’s liquidity and financial health.

HighRadius Named as a Leader in the 2024 Gartner® Magic Quadrant™ for Invoice-to-Cash Applications

Positioned highest for Ability to Execute and furthest for Completeness of Vision for the third year in a row. Gartner says, “Leaders execute well against their current vision and are well positioned for tomorrow”

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR Automation Software for Large and Midsized Businesses

HighRadius stands out as an IDC MarketScape Leader for AR Automation Software, serving both large and midsized businesses. The IDC report highlights HighRadius’ integration of machine learning across its AR products, enhancing payment matching, credit management, and cash forecasting capabilities.

Forrester Recognizes HighRadius in The AR Invoice Automation Landscape Report, Q1 2023

Forrester acknowledges HighRadius’ significant contribution to the industry, particularly for large enterprises in North America and EMEA, reinforcing its position as the sole vendor that comprehensively meets the complex needs of this segment.