Doubling Down on Collections by Eliminating Waste from Cash-Application Process

How Fortune 1000 companies and SMEs automate credit and accounts receivable operations to improve productivity and collect open A/R faster.

Doubling Down on Collections by Eliminating Waste from Cash-Application Process

Cash application is one of the more resource-intensive processes in accounts receivable and organizations are better off in automating cash application and shifting resources to higher-value activities including collections and credit. The other disadvantage of a slow cash application process is that it is an upstream process that further slows down deductions and collections process. As an example, if a customer had already paid for an invoice but the status is not updated as closed in the ERP, collections analyst will waste time by calling a customer who had already paid.

Top Challenges with The Cash Application Process

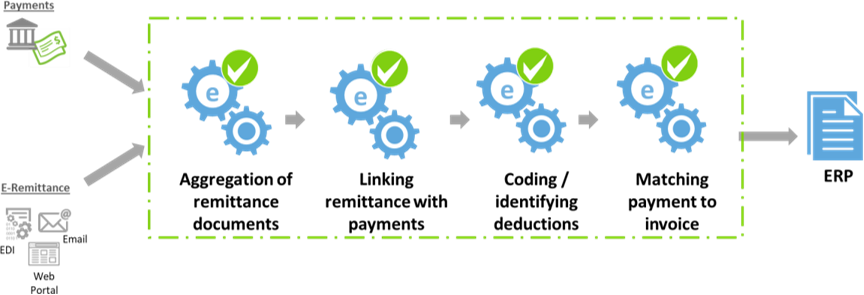

Organizations today receive payments through checks as well as electronic formats including ACH, real-time payments, and credit cards. Reconciling cash for checks and e-payments poses different challenges.  For checks, A/R teams typically receive a bank lockbox file that contains the payment details, however, ERP systems need reconfiguration to be able to read the lockbox file and apply for payments. This is a recurring problem whenever organizations either add a new lockbox service or switch banks. Also, lockbox services tend to be quite expensive to maintain as banks also charge significant key-in fees for capturing remittance data. Nevertheless, this keyed-in data is usually insufficient for successfully posting the payments. The cash application analysts still have to resolve exceptions due to incomplete remittance data or code the deductions while identifying short payments. All of these steps have been illustrated in the above figure.

For checks, A/R teams typically receive a bank lockbox file that contains the payment details, however, ERP systems need reconfiguration to be able to read the lockbox file and apply for payments. This is a recurring problem whenever organizations either add a new lockbox service or switch banks. Also, lockbox services tend to be quite expensive to maintain as banks also charge significant key-in fees for capturing remittance data. Nevertheless, this keyed-in data is usually insufficient for successfully posting the payments. The cash application analysts still have to resolve exceptions due to incomplete remittance data or code the deductions while identifying short payments. All of these steps have been illustrated in the above figure.  Coming to electronic payments, while there is significant adoption of various formats, the cash application team is burdened with the cash reconciliation process as the remittance details are sent separately either through email, EDI or customer portals, and websites. Though the payment itself is electronic and fast, processing the payments is highly manual and time-consuming. The analysts collect remittance from different sources, associate them with incoming payments, link them to corresponding open invoices, check for short payments and discounts and then post the cash in ERP which takes a huge amount of time and effort. All of these steps have been illustrated in the above figure.

Coming to electronic payments, while there is significant adoption of various formats, the cash application team is burdened with the cash reconciliation process as the remittance details are sent separately either through email, EDI or customer portals, and websites. Though the payment itself is electronic and fast, processing the payments is highly manual and time-consuming. The analysts collect remittance from different sources, associate them with incoming payments, link them to corresponding open invoices, check for short payments and discounts and then post the cash in ERP which takes a huge amount of time and effort. All of these steps have been illustrated in the above figure.

How Top Organizations Automate Cash Application

As the challenges have highlighted, cost and resource wastage are problems that have to be addressed on the cash application front.  By leveraging machine learning, organizations are able to automatically aggregate remittances, reconcile cash and identify deductions. Figure 8 talks about how each of the steps ? aggregating remittance documents, coding deductions and applying cash could be automated using an AI-based cash application system.

By leveraging machine learning, organizations are able to automatically aggregate remittances, reconcile cash and identify deductions. Figure 8 talks about how each of the steps ? aggregating remittance documents, coding deductions and applying cash could be automated using an AI-based cash application system.

Cash Application Success Stories: Danone

Danone North America had four FTEs for cash application and with many North American businesses, they had both electronic and check payments that impacted their cash application process. After leveraging an artificial intelligence-powered cash application automation solution, Danone was able to reduce the cash application team from 4 members to 1 and deployed the remaining members to other A/R functions.