The CFO’s Guide to Unlocking Working Capital with Credit and Receivables Technology

Credit and A/R projects are large, complex, expensive and fraught with risks. This e-book demystifies technologies such as Robotic Process Automation and Artificial Intelligence to help finance leaders transform operations.

Executive Summary

The latest innovation in credit and accounts receivable technologies have brought in tremendous efficiencies to finance departments worldwide.

HighRadius’ clients such as Nike, Airgas and Cargill have achieved tremendous impact on productivity of operations and significant positive impact on KPIs such as Days Sales Outstanding. All of it resulted in significant improvements in cash flows to the tune of $22 M annually.

While the promise of technology is a given, there is always a chasm between promise of technology and real world results. The idiosyncrasies associated with either a specific firm or a specific process increase the complexity of fitting technology to business process. Such complexities eventually widen the chasm between expectations and reality. Research conducted by Panorama Consulting corroborates these findings, revealing that close to 54% of ERP implementations met less than 50% of their stated objectives.

HighRadius is a niche solution provider with an exclusive focus on Credit Management process, Payments and Accounts Receivable automation solutions. This document is designed to provide organizations with a greater rate of implementation success based on learnings from more than 400 receivables transformation projects worldwide.

This e-book will discuss the best practices to be followed during pre-implementation, implementation and post implementation phases for successful receivables transformation projects.

Pre-Implementation Best Practices

Credit and Accounts Receivable (A/R) Process Assessment

A credit and A/R process assessment is the first step in the pre-implementation phase. A common pitfall with most firms is that the project leaders straight away get into requirements analysis without understanding the status quo of credit and A/R processes within their organization. To achieve success, it is of utmost importance to determine the current state to set the foundation for future change.

The assessment process provides clarity on the following three items:

- The scope of the receivables transformation project

- Budget and timelines

- Resources required

The assessment process improves decision-making that will have a direct impact on the scope, the cost and the value capture of the project.

Receivables Project Core Team Selection

As a first step, set-up a core team comprised of A/R process owners, IT, senior execs and end users. It is also strongly recommended to add 3rd party consultants to challenge the “it is how things have always been done” mentality.

The core team should be chartered to review the current processes and systems to evaluate the value capture of implementing receivables automation. Figure1 highlights the team composition.

Credit and A/R Assessment Process

At its core, the assessment process provides a detailed view of the activities that that each team member is responsible for and also help track the KPIs of the project’s implementation.

Figure 2 outlines the five stages in the audit process below:

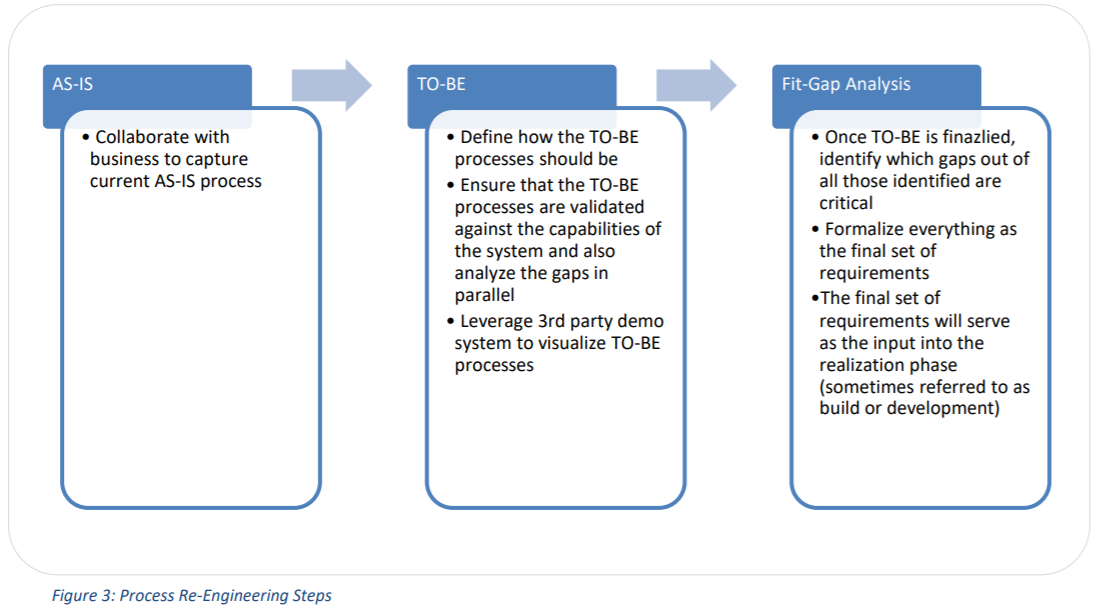

Process Re-Engineering

Technologies such as Robotic Process Automation open up new opportunities to gain efficiencies in routine processes. Therefore, it becomes critical for business teams to “unlearn” or at least shed biases WRT the AS- IS process/legacy systems. Any attempt to design a “new‟ system for an “old‟ process might at best bring in marginal improvements in operational performance whereas redesigning the processes and taking advantage of the emerging technologies is imperative to achieving significant performance improvements. To avoid making this common misstep, follow the outline below:

- Identify Key AS-IS Processes: Start with identifying key processes that directly impact the bottom line of the organization. Study the AS-IS processes without trying to solve all the problems of the current system. For example, a HighRadius client, Dr Pepper Snapple Group, used a Lean 6-Sigma tool called Gemba to observe and analyze the Credit and A/R processes. To learn more, watch this video.

- Determine TO-BE Processes: Once the AS-IS processes have been analyzed, design the TO-BE processes. The TO-BE processes need to take into consideration the IT system that supports these processes. Employ a demo system to visualize how these proposed processes would work in the software to help the core team identify the gaps in their current system.

- Conduct a Fit-Gap Analysis: Most receivables technology implementations are customized according to the business needs. Once the gaps have been identified, the core team must prioritize the gaps according to the criticality and the impact on the bottom-line to define the scope of the project.

Fit-Gap Analysis Document

The fit-gap analysis document should ideally have the following fields:

| Requirement description Business Priority |

ROI Priority Category Minor Gap |

Major Gap ERP Gap Solution Options |

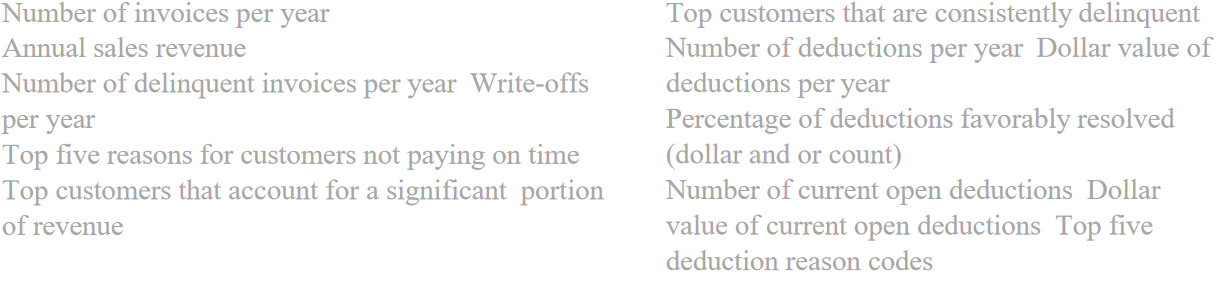

“ROI Priority” is a key column as it is important to track what impacts the KPIs. The below graph (Figure 51) is a good representation of the type of KPIs that could be used to track the performance of credit and A/R teams.

Other important metrics and reports to consider include the following:

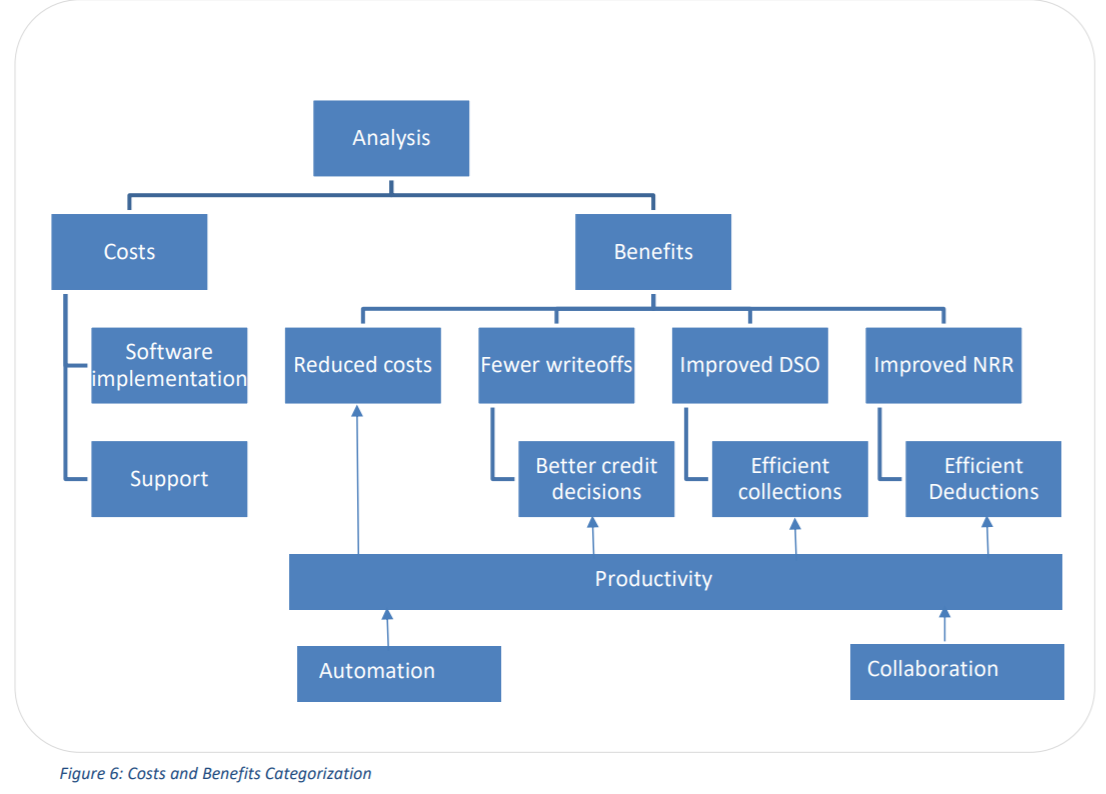

Return on Investment/Cost-Benefit Analysis

Implementing a credit, A/R and invoicing solution directly impacts the costs of a company. Putting together a business case involves a thorough review of the current processes and systems in place and identifies opportunities for improvement via process re-engineering and automation. Some of the KPIs and metrics listed could directly impact the bottom line.

For a more in-depth understanding, please read the eBook on Automating Accounts Receivable- Building a Winning Business Case that outlines the cost-benefit analysis.

Figure 6 analyzes the costs vs benefits to make a business case for receivables transformation projects:

Receivables Technology Fit-Gap

After the assessment, the information needed to address the issues and start filling in the gaps is collected. The next step is to understand the capabilities of various ERPs to achieve TO-BE processes and the deployment options.

Receivables Technology Modules and Capabilities

Most ERPs provide some out of the box functionality for the following four processes:

- Credit Management

- Electronic Invoice Presentment and Payment(EIPP)

- Cash Application

- Collections Management

- Disputes Management

The following image details the key requirements of credit and A/R leaders in various processes:

Operations-Specific Best Practices

Each process in credit and A/R is heavily customized to suit business needs as per the fit-gap analysis.

Additionally, there are many automation opportunities in the credit and A/R processes beyond the basic ERP capabilities, which are enhanced by 3rd party solutions.

Credit Management

Many organizations already have some form of credit management out of the box in ERP systems.

The presence of more than a few of the following within an organization might be an indicator that the upgraded credit management technology might be worth evaluating:

- A distributed system landscape and problems associated with consolidating information for credit decisions

- Large number of customers and scoring, rating and updating of credit limits that could be automated, minimizing laborious credit calculations

- Need for custom scores that combine internal and external data for calculations

- Many external information providers coupled with the desire to eliminate third- party products or plug-ins

- Too much non-value added manual work

Automated Data Aggregation

Credit decisions are complex and involve the manual data aggregation from 3rd party sites including credit agencies (Dunn & Bradstreet, Experian etc.), public financials aggregators and insurance firms. Automating the credit data capture process will save time and improve productivity of credit teams. Figure 8 explains the above pictorially.

Credit Decision Workflows

Credit processes require collaboration for teams within and outside the organization to arrive at credit decisions.

Empowering credit teams with set workflows and streamlining the processes will greatly improve the productivity of all the stakeholders. It is recommended to create workflows for the following cases:

- Credit limit approval

- Credit limit increase requests

- Blocked orders

- Bankruptcy alerts

- Collateral expiries

Online Credit Application

Many organizations process hundreds of credit applications every month while onboarding new customers. In that process, there is a lot of back and forth between sales, customer support and customer teams to put together a credit application.

Providing a standard online application where customers can fill out all the required details will significantly speed up customer onboarding time. The online credit application will also increase the productivity of sales personnel for they don’t have to get involved in data collection.

Electronic Invoice Presentment and Payment

EIPP solutions have struggled with low customer adoption because:

- It requires changes to current processes

- It introduces manual A/P processing as customers have to login to web portals

- It removes the float that many organizations count on

Having a phased roll out and a strong incentive plan are critical for ensuring that the implementation of EIPP solutions is a success. Here are some best practices:

- Start with the smallest customers who are easier to influence and are good candidates for Phase One. Large customers are less likely to want to change their processes

- Quantify the cost savings upfront, such as the elimination of paper based billing, DSO reduction, lockbox cost reduction, staff realignment due to self-service, etc. to gain an insight into what savings are available for incentives

Apart from the above, choosing the right payment solution that is compliant with PCI DSS norms is important. To learn more about the differences between payment platforms and the how to risk associated with credit card data theft view the video here.

Cash Application

Cash application is one of the most manual operations in the credit to cash process. There are many reasons for this – various payment modes, non-standard remittance formats, electronic remittance decoupled from payment, many channels of remittance delivery, including email, portal and paper, just to name a few. This inherently inefficient process then becomes a bottleneck for most accounts receivable operations teams because it slows down downstream processes like deductions and collections. Consider the following scenarios:

- A customer has already paid but, because of the delays in applying cash, the collections analyst still calls the customer for payment

- A customer has short paid but the A/R team could only start working the deduction after calling the customer or receiving the claims file to identify the reason

Figure 9 highlights the manual steps in cash application. In addition to the above, in case of check payments, the issues are with:

- Limited information sent on the check stub

- Data entry from the check stub to ERPs

- Linking open A/R to payments

- Bank Lockbox expenses

In case of electronic payments, the issues are with:

- Multiple sources such as EDI, email and websites from which remittances have to be aggregated

- Submitting remittances with PO number, partial invoice number instead of invoices

- Linking open A/R to payments

All of the above steps including aggregation of remittances, linking and matching remittance and open A/R could be automated by artificial intelligence and Robotic Process Automation(RPA) powered systems.

Collections Management

A collections analyst’s primary responsibility is correspondence with customers. And yet, according to many findings, an analyst spends only 20% of his/her time on correspondence and rest of the time organizing who to call, collecting backup and engaging in other activities including composing emails.

Some best practices for the collections management are outlined in the following section.

Rules-Based Correspondence

A McKinsey study stated that more than 70% of collections calls are made to customers who would have paid anyway. This statistic seems to indicate a redundancy in the process, and unnecessary work being done, especially considering there is technology available that could analyze and prioritize the collections workflow.

For example, dunning notices (outlined in Figure 9) could be sent through RPA by configuring rules and linking the correspondence technology with accounts receivable module in the ERP.

Collect on Clean Receivables with Prioritized accounts

Prioritized accounts in a worklist is the single most important feature for collections analysts. However, a collections agent usually transacts with many kinds of open A/R items, including those that are disputed, that have promises to pay and so forth and ageing list doesn’t capture all these attributes.

Often such A/R items are deemed “uncollectible” on that particular day and a collector’s worklist should not contain any of these uncollectible items. While configuring the collections worklist, make sure to exclude the following AR items from a collector’s worklist:

- Items with open promise to pay: Items with an open promise to pay, or items with a future payment promised on date, these items should be excluded from the ‘To Be Collected’ amount

- Dispute cases not in a ‘To Be Collected’ status: All open dispute cases which have not been updated with a status that is mapped to the ‘To Be Collected’ in collections management should be excluded from the ‘To Be Collected’ amount

- Items with a current dunning notice: If a line item has recently been dunned, this amount should be excluded from the ‘To Be Collected’ amount

- Items arranged for payment: All amounts that are (1) collected with a debit memo procedure or (2) where the account statement balance contains a payment notification from the bank should be excluded from the ‘To Be Collected’ amount

For more information on identifying clean receivables and prioritizing accounts for collections, watch the on-demand video here.

Deductions Management

Deductions Management is process intensive and requires cross departmental collaboration between Credit, Collections, Accounts Receivables, Customer Service, Logistics, Sales and others. In a recent study conducted by the Credit Research Foundation (CRF) on customer deductions, lack of cross-departmental cooperation and inefficient processes were identified as the top two internal challenges for controlling deductions.

Here are some of the best practices while transforming deductions operations.

Workflows for Collaborative Resolution

RPA is the key technology to implement workflows for deductions management. Configuring rules for routing deductions cases to appropriate roles is done through RPA. Some of the best practices are:

- Define and implement specific workflows for at least the top three to five reason codes that account for more than 80% of deductions

- Implement a generic workflow for all other reason codes

- Implement credit memo approval workflow versus a paper-based offline approval process

Rationalize Deduction Reason Codes

- Create a two-level hierarchy (category and reason code)

- Create between a minimum of 10 and a maximum 100 reason codes

- Do not create a customer-specific reason code as a main deduction reason code

Review Cash Application’s Impact

As discussed earlier, cash application has a significant impact on deductions operations as lot of deductions could be identified while applying cash. Review cash application processes for opportunities to improve the postings that significantly enhance the deductions resolution process.

The artificial intelligence technology available today could automate the aggregation, linking and matching remittance information with payments to automatically post cash and open deductions cases if applicable.

Figure 11 shows the cash application process.

The following is a summary of recommendations to consider:

- Ensure that deductions are coded and residuals are posted to original invoices where appropriate

- Ensure that cash application includes all the relevant backup

- Capture BOL, POD, Payment files

- Make sure that cash application references invoices, POs and A/R documents within the deductions case

- Create matching algorithm to help in the linkage

Define Scope

Clearly define the scope of each module and the level of customization required. The common pitfall here is planning a Phase 1 with out-of-the-box features of ERPs with the anticipation of Phase 2 for enhancements and customization.

Even though some companies manage to get budgets for a Phase 2, most FSCM implementations do not have a follow-on Phase 2 and end with what was implemented in Phase 1. A separate, consequent phase for enhancements and customization will cost significantly more compared to including customizations as part of Phase 1.

Implementation Best Practices

This chapter captures the best practices once a receivables transformation project is officially budgeted and kicked off. To ensure user acceptance and a successful implementation follow the practices described in this section.

Implementation Methodology

Follow a proven project implementation methodology. Figure 14 is a summary of the HighRadius implementation methodology:

This document does not cover all the details of each phase and sub-phases. It only highlights the key aspects that are important from a receivables technology project implementation stand-point.

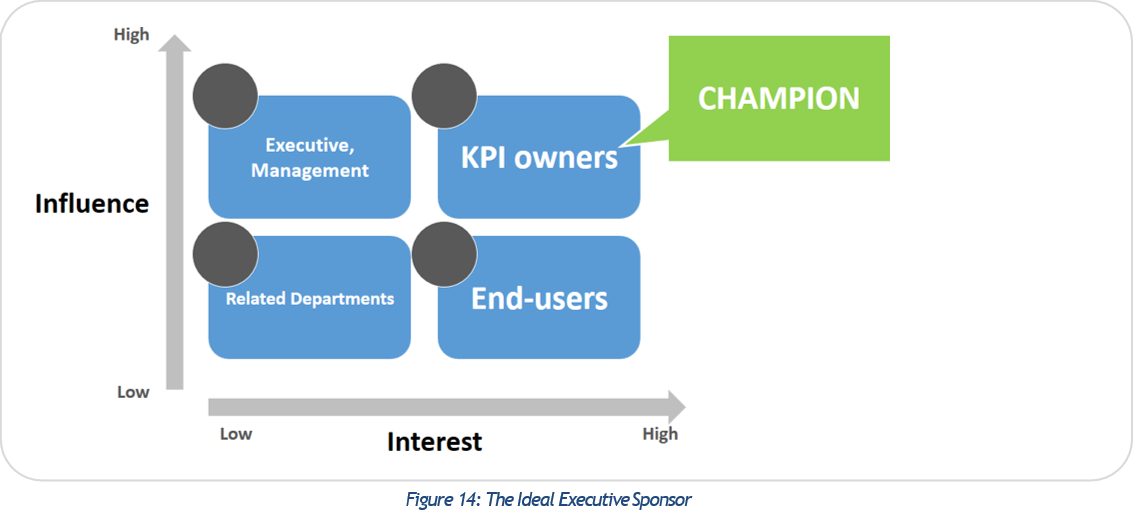

Executive Sponsorship

Having the commitment and support of a senior executive to the project will set the context for serious engagement from both business and IT teams to the project. The senior executive who is actively involved will stay informed on the project status and will help with clearing roadblocks, allocate resources, etc.

An ideal sponsor for the project would be a senior executive who believes that technology will impact the performance of KPIs. Such executives fall in the sweet spot of having both the interest in the project and also the necessary influence to sponsor it. Figure 15 highlights the ideal champion to pick for executive sponsorship.

Project Team Selection

Staff the project team to include representation from both IT and Business. The following is a summary of internal resources recommended for allocation to the project.

NOTE: The resource list below does not account for the specialty consultants that might be required from a credit and A/R technology vendor. Tables 2 and 3 outline the IT and business resources needed to implement SAP Receivables Management.

Testing

The following is a summary of testing best practices:

- Conduct at least two, preferably three, system integration testing (SIT) cycles

- Create test scripts beyond feature testing, for every possible business process scenario

- Test scalability as it is extremely critical for high invoice and deductions volumes

- More than one million invoices in a year would be considered high volume

- For a multi-system scenario (refer to section 2.5.1), scalability is extremely critical

Training

Training is key to the success of an implementation and is often overlooked when prioritizing. Implementations tend to be focused on the realization phase due to their technical nature. One of the biggest challenges in software implementation is accurately capturing the right criteria and requirements. What is intuitive to a consultant or an IT employee might not be to an end user. The following is a summary of recommendations to ensure users receive rigorous training and are not “left out” until the very end of the implementation.

- Be sure the consultants train the users before the wrap-up of the implementation. Have the consultants “Train the Trainer” and assist the “Trainer” in conducting training sessions

- Choose a Super User from the credit and collections department as the “Trainer”

- Since they understand the business side and have working relationships with the users, they will also be available beyond a formal training session as a “go to” contact

- Conduct training on day-to-day business processes versus system features and functions

- For, example, a credit hold on an order emerges in a call to the customer that was conducted to check the status of open invoices, and results in a promise-to-pay creation in the system

- Create detailed training documentation with systematic screenshots of the system

Post Go-Live Best Practices

Post go-live it is all about evaluating the new processes and applying course corrections as and when required.

Evaluate KPIs

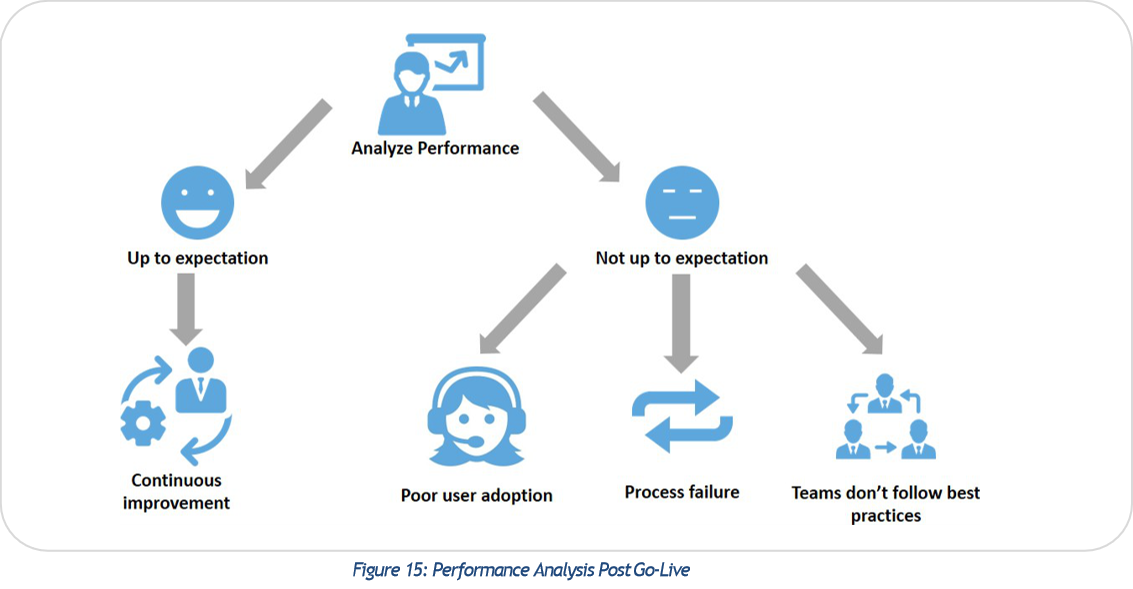

Process owners have to revisit KPIs and check whether TO-BE processes that were designed in the audit phase are performing to expectations. Figure 16 shows possible steps needed depending on whether performance of the new system meets expectations or not.

If the implementation performs as expected, set these processes for a continuous improvement program for yearly gains.

If the performance is not up to expectations, do a root cause analysis and fix the problems. It has been found that most failures mainly fall into three buckets:

- User adoption: Poor user adoption is a big factor in process failure for improvements but is only apparent when users start affecting the processes through adoption

- Failure to adhere to best practices: This is also another major factor in failure as each process has a set of best practices to follow for maximum impact

- Poor process design: This scenario is not as frequent as the above two but could happen if the process designed was not up to the mark

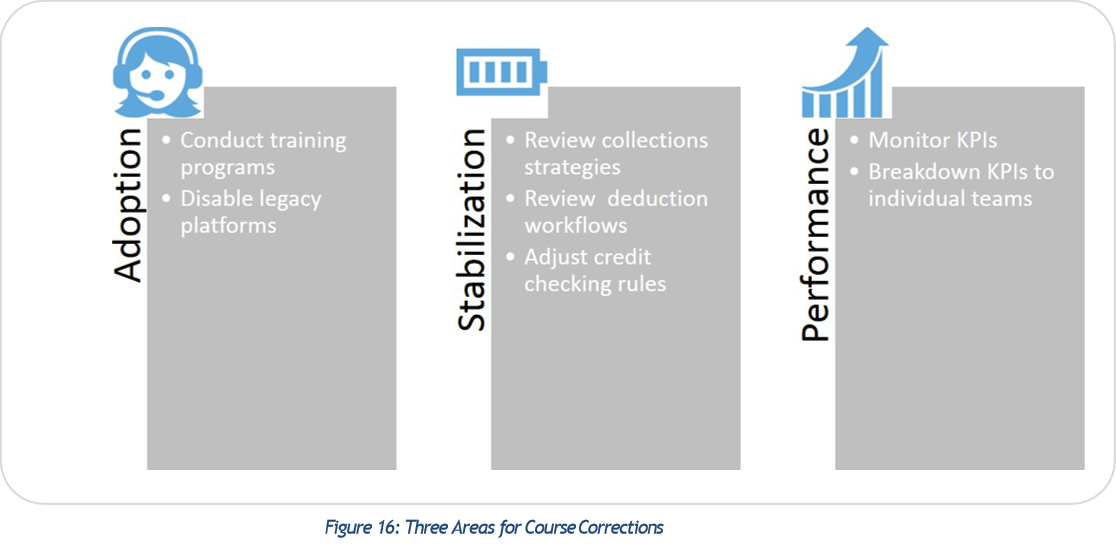

Apply Course Corrections

Once root-cause analysis has been completed, decide on course corrections. Figure 17 – Steps to correct failures related to user adoption, stabilization and ways to monitor performance.

User adoption and adherence to best practices are improved by conducting training programs and disabling access to legacy platforms. Breaking down KPIs to individual teams will also help in a comparative analysis of where each team stands.

Addressing process design failure means credit and A/R teams must “go back to the drawing board” to redesign the process. A system will only be as good as the inherent process that runs on it. Some of the common processes that need reviewing are 1) Credit workflows, 2) Collections strategies and collections segments, 3) Dispute resolution workflows, and 4) Cash Application process.

Summary

Automation of manual processes in credit management process and receivables operations is a sure shot way to improve productivity of teams by at least 50%. However, a system is only as good as the underlying processes that run on it and the automation it provides to reduce team workload. Hence it becomes very important for process owners to assess their current processes and incorporate best practices from top performing organizations before embarking on receivables transformation initiatives.

Recommendations