The Comprehensive Guide to Account Reconciliation: Process, Systems, and Examples

2 September, 2024

16 minute read

Soumi Sarkar, Fintech content strategist

S

Soumi Sarkar

Soumi specializes in O2C, finance, and accounting transformation with a focus on bringing a domain-led perspective to accounting, finance and order-to-cash transformation. She crafts insight-driven, CFO-aligned content that helps finance teams optimize operational workflows and drive measurable outcomes. Beyond her professional work, Soumi is a published author of two books, a poetess, an avid reader, and a storyteller who enjoys exploring narratives across both B2B and creative formats.

Last updated: 22 July, 2026

Automate reconciliation and close 30% faster with 5 proven AI use cases.

Account reconciliation compares two sets of financial records to ensure that general ledger balances accurately match external statements. While entries in a general ledger are based on periodic facts, they are prone to timing differences or clerical errors. For example, a check recorded as paid may bounce, or a bank fee may go unrecorded until the statement arrives.

As a core financial control mechanism, reconciliation acts as the gatekeeper of financial accuracy. By verifying that internal ledgers align with external records like bank statements, supplier reports, and sub-ledgers, finance teams ensure that their books reflect reality. This alignment is critical not just for daily operations, but for month-end reporting accuracy, audit readiness, and compliance under frameworks like US GAAP and IFRS.

In this blog, we will dive into the essentials of the reconciliation process, how finance teams can navigate common gaps, and the evolving role of advanced account reconciliation software in modernizing these workflows.

Key Takeaways

Account reconciliation is a financial control mechanism, not just a checkbox; it drives accuracy, compliance, and fraud prevention.

Spreadsheet-based reconciliation is a liability at scale; AI-powered automation is how finance teams close faster and error-free.

Discrepancies left unchecked compound into bigger risks; a consistent reconciliation cadence keeps books audit-ready.

Table of Contents

What Is Account Reconciliation?

Key Takeaways

Why CFOs Prioritize Reconciliation: Importance of Account Reconciliation

Key Types of Account Reconciliation

The 10-Step Account Reconciliation Process

Manual vs Automated Account Reconciliation

Evaluating an Account Reconciliation System: Key Features To Look For

Choosing Between Reconciliation Software vs. Outsourcing Reconciliation Services

Examples of Account Reconciliation

Use case for the account reconciliation process

Benefits Of Account Reconciliation

Key Challenges of Account Reconciliation

Best Practices for Account Reconciliation

Accelerate Your Account Reconciliation With HighRadius’ Agentic AI-Led Account Reconciliation Software

FAQs For Account Reconciliation

30% of finance team’s time is still lost to manual account reconciliations.

With 100% journal entry automation, a leading hotel giant slashed their reconciliation time to minutes.

Why CFOs Prioritize Reconciliation: Importance of Account Reconciliation

Modern finance leaders view reconciliation as more than just matching. It is a strategic pillar for:

1. Improved accuracy and cash flow

Account reconciliation proactively identifies and resolves discrepancies, such as unrecorded payments and overpayments, in financial records. This timely identification and resolution of risks helps improve cash flow, ensure payment for outstanding payments, and maintain accurate and up-to-date financial records.

2. Fraud prevention

Matching the business’s accounting records to external sources, such as bank statements, leads to detecting possible fraud, such as unauthorized transactions or embezzlement.

3. Compliance

One of the most crucial purposes of account reconciliation is to comply with account regulations, such as GAAP accounting principles or SOX requirements, and ensure integrity in financial reporting. Failure to comply can result in penalties and legal action.

4. Better decision-making

Accurate and up-to-date financial records help both internal and external stakeholders make better and more informed decisions. They also give an overview of the company’s financial health, allowing better and more confident decision-making.

In practice, account reconciliation goes beyond just matching entries. CFOs now view it as a control mechanism that directly impacts compliance and audit readiness. Manual spreadsheets often increase exposure to errors and regulatory scrutiny, particularly under frameworks like US GAAP and IFRS. By contrast, automated account reconciliation tools align every transaction against source data in real time, making exceptions visible immediately and giving finance leaders the confidence that reporting is both accurate and audit-ready.

Templates

Your manual reconciliation has a leak—this template fixes it fast.

Use this pre-built bank statement reconciliation template to eliminate errors.

Account reconciliation takes many forms. Businesses must address them all within one framework, reducing the risk of misstatements and strengthening the overall financial close process.

1. Bank reconciliation

Bank reconciliation involves comparing your internal cash ledger with the actual bank statement. Discrepancies often arise due to unrecorded bank charges, interest income, or pending transactions. Modern bank reconciliation tools ensure that cash positions are accurate and audit-ready.

2. General ledger reconciliation

General ledger account reconciliation is the process of matching and verifying the balances in a company’s general ledger against supporting data (sub-ledgers, external systems, etc.), to ensure accuracy and consistency. Automating general ledger reconciliation helps streamline this by applying rules for matching, detecting anomalies, and maintaining audit-ready records to speed up financial close.

3. Credit card reconciliation

Credit card reconciliation matches a business’s credit card statements against its internal records (general ledger, expense reports, etc.) to ensure every transaction is accurate, authorized, and accounted for, helping detect errors, spot fraud, and ensure financials are reliable.

4. Intercompany reconciliation

Intercompany reconciliation is used in businesses with multiple entities. It ensures that all cross-entity transactions align. Balances are reviewed and matched across entities to eliminate mismatches and ensure accurate group-level reporting.

5. Balance sheet reconciliation

Balance sheet reconciliation verifies that all account balances in your financial records match the corresponding supporting data (bank statements, sub-ledgers, ERP entries). By using automated balance sheet reconciliation software, like AI/ML-agents to match transactions, flag mismatches, and generate audit-ready reports, it ensures accuracy, speeds up financial close, and reduces manual errors.

The 10-Step Account Reconciliation Process

To ensure accuracy of financial records, the account reconciliation process includes evaluating, comparing, and reviewing recorded transactions against financial documents like bank statements, invoices, and other financial data. Reconciliation ensures there are no errors that could lead to potential financial mismanagement.

The process helps businesses avoid costly mistakes, detect red flags early on, avoid overdraft charges, comply with regulatory requirements, and streamline the financial close process while maintaining the accuracy and integrity of financial reports. Here’s a step-by-step breakdown of the account reconciliation process.

1. Identify key accounts

Start by pinpointing which accounts require reconciliation—think high-risk or high-volume ones like cash, AP, AR, and payroll. Prioritize those tied to external reporting or where errors can disrupt business operations.

2. Gather source data

Pull relevant documents from both internal systems and third parties—bank statements, vendor invoices, sub-ledgers, and system logs. Incomplete or inconsistent inputs lead to incomplete outcomes.

3. Match line items

Compare internal entries against external records, line by line. Every transaction must tie out—no rounding off, no approximations. This is where most discrepancies surface.

4. Flag and investigate discrepancies

Spot timing gaps, duplicates, missed journal entries, or outright errors. Dig deep to understand whether the root cause is procedural, system-related, or tied to poor data hygiene.

5. Adjust journal entries

Make the necessary corrections in the GL. Whether it’s booking missing interest income or correcting misclassifications, this is the financial cleanup CFOs rely on to stay audit-ready.

6. Document the reconciliation

Log all exceptions, adjustments, and explanations in a clear audit trail. If it’s not documented, it doesn’t exist—especially when auditors or regulators ask questions.

7. Review and approve

Get the reconciliation signed off by the appropriate stakeholders. A second pair of eyes ensures completeness and flags anything missed, which is critical for high-stakes accounts.

8. Archive for audit and reference

Store finalized reconciliations in a centralized system. Clean documentation is your insurance policy when audit season hits or leadership needs answers.

9. Repeat the process

Reconcile on a set cadence, monthly at minimum, more frequently for cash-critical accounts. Reconciliation isn’t a one-time event. It’s a control discipline.

Manual vs Automated Account Reconciliation

Manual account reconciliation often leads to delays, errors, and increased compliance risks—especially as transaction volumes scale. By contrast, automated reconciliation streamlines the process with real-time matching, built-in controls, and exception management. Here’s a side-by-side comparison to highlight the impact of automation across speed, accuracy, and audit-readiness.

Manual vs Automated Account Reconciliation

Aspect

Manual Account Reconciliation

Automated Account Reconciliation

Process Speed

Slow and time-consuming; relies heavily on spreadsheets and emails

Real-time matching and processing via AI and system rules

Accuracy

Prone to human errors, omissions, and delays

High accuracy with system-driven matching and exception flagging

Resource Dependency

Requires significant finance team bandwidth

Reduces workload, freeing up resources for strategic analysis

Scalability

Difficult to scale with volume or organizational growth

Evaluating an Account Reconciliation System: Key Features To Look For

When moving from spreadsheets to a dedicated account reconciliation system, enterprise-level organizations should look for these non-negotiable features:

Automated Transaction Matching: Using AI/ML to match thousands of lines of data in seconds.

Direct ERP Integration: Seamless connections with SAP, Oracle, NetSuite, or Microsoft Dynamics.

Real-Time Dashboards: Visibility into reconciliation status across global entities.

Anomaly Detection: AI-driven flagging of potential errors or fraudulent activities.

Audit-Ready Documentation: Automatically generated audit trails and digital signatures.

Choosing Between Reconciliation Software vs. Outsourcing Reconciliation Services

Many businesses struggle to decide whether to keep reconciliation in-house using an account reconciliation system or outsource it to account reconciliation services.

Feature

Account Reconciliation System

Account Reconciliation Services (Outsourced)

Control

Full internal control and data visibility.

Relies on third-party reporting.

Speed

Real-time, continuous reconciliation.

Typically periodic (monthly/quarterly).

Cost

Predictable subscription model; high ROI.

Variable service fees; often higher long-term.

Security

In-house data security and SOC compliance.

Third-party data handling risks.

Scalability

Handles millions of transactions via AI.

Limited by the service provider’s headcount.

Examples of Account Reconciliation

Account reconciliation isn’t a one-size-fits-all task. It spans multiple functions across the balance sheet. From cash and receivables to intercompany and investments, each type of reconciliation ensures your books reflect economic reality and stand up to audit scrutiny.

1. Reconciling the cash balance in the ledger with the bank account

The cash balance in a company’s books may not always match the bank account balance. This discrepancy can arise from several factors, such as missed entries, bounced payments, fees incurred, or interest accrued. Reconciling these balances ensures the accuracy of financial records and helps detect potential issues early.

2. Reconciliation of accounts payable

Accounts payable refers to the money a company owes to its suppliers, vendors, and employees. Smooth handling of accounts payable is essential for producing and delivering goods or services. Regular reconciliation of accounts payable is crucial to identify issues such as short payments, disputes, or missed early payment discounts, ensuring operational efficiency and maintaining good supplier relationships.

3. Reconciliation of accounts receivable

Accounts receivable represent the amount customers owe for goods or services delivered. Regular reconciliation of accounts receivable is critical for ensuring steady cash flow and positive customer relations. This process helps verify that there are no short payments, deductions, or disputes, and that credit facilities are adjusted accordingly to prevent bad debt.

4. Reconciliation of inter-company transactions

Inter-company transactions must be reconciled in organizations with subsidiaries or group companies to ensure accuracy across all entities. Intercompany reconciliation ensures that cash balances, liabilities, and assets are correctly reflected in each company’s financial statements, helping to maintain financial transparency.

5. Reconciliation of asset transactions

Companies often buy or sell assets such as property, machinery, or inventory. These transactions must be accurately reflected in the company’s books through proper balance sheet reconciliation, ensuring that the books correctly represent the company’s asset base and its depreciation over time.

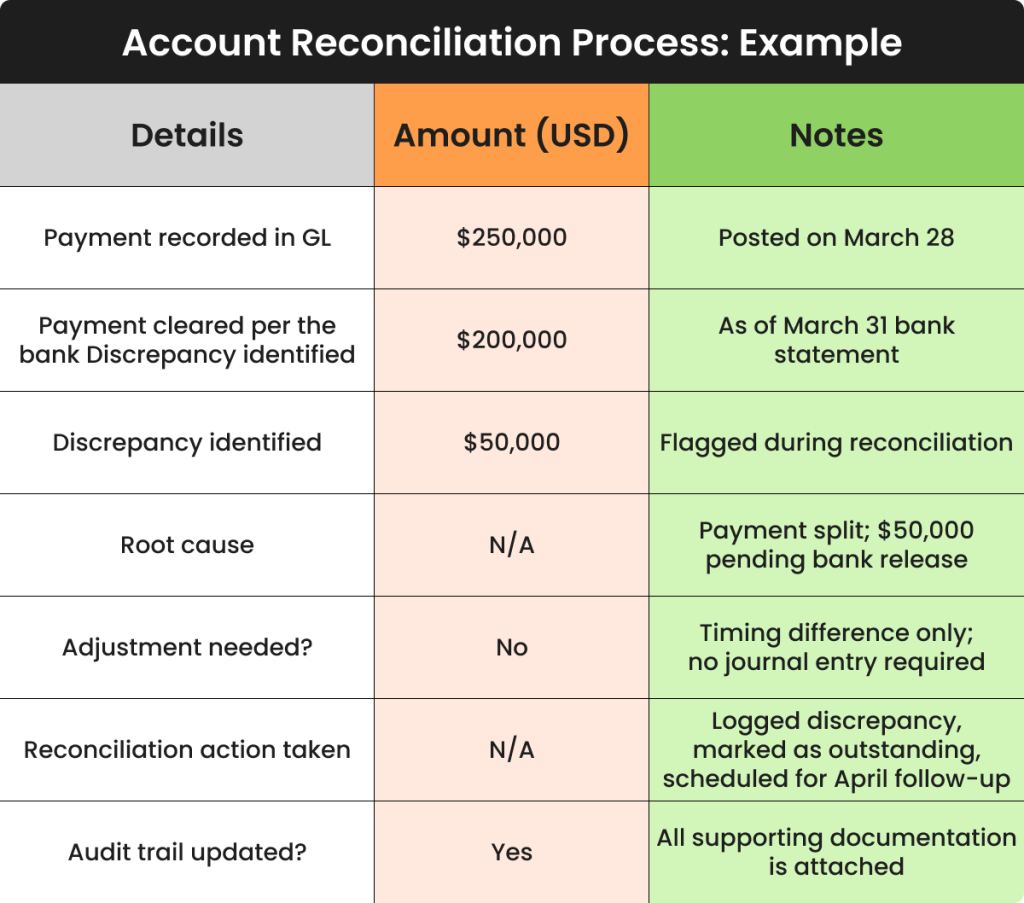

Use case for the account reconciliation process

A mid-sized FMCG firm recorded a $250,000 vendor payment in its general ledger on March 28. However, the March 31 bank statement showed only $200,000 had cleared.

During month-end reconciliation, the finance team flagged a $50,000 discrepancy. A closer review confirmed the payment was processed in two parts—$200,000 cleared immediately, while $50,000 was held due to a bank processing delay.

Resolution:

The $50,000 was marked as an outstanding item in the bank reconciliation and documented as a timing difference. No journal entry was required, but the discrepancy was logged for audit readiness and tracked to ensure it cleared in April.

Benefits Of Account Reconciliation

Consistent reconciliation drives precision. It aligns ledger entries with bank statements, receivables, and payables, highlighting mismatches, ensuring GAAP compliance, and revealing fraud or billing irregularities. In short, it results in clean books, fewer surprises, and better calls at the executive table. Here are a few benefits of the account reconciliation process.

1. Ensures accuracy

Account reconciliation checks the reliability of financial records. It ensures accurate reported balances by matching general ledger entries with external documents like bank statements or invoices. This reduces the risk of misstatements and builds trust in financial reporting.

2. Identifies errors and discrepancies early

The account reconciliation process flags mismatches before they escalate. Whether it’s short payments, duplicate entries, or missing charges, reconciling accounts helps uncover issues early on – before they derail close cycles or invite audit red flags.

3. Maintains compliance

It supports alignment with financial regulation and strengthens GAAP adherence and audit preparedness by ensuring records are complete, verified, and backed by documentation.

4. Detects fraud and irregularities

Account reconciliation detects all policy violations before corrupting the system and workflows. By regularly reconciling accounts, finance teams can catch unauthorized transactions, errors, or misuse, thereby closing the door on potential fraud.

5. Enables confident decision-making

Account reconciliation helps businesses drive informed executive actions. It ensures clear, verified data across systems, giving leaders clarity on cash, liabilities, and receivables, leading to smarter financial moves without second-guessing the numbers.

6. Faster month-end close

Accurate reconciliation clears exceptions quickly, freeing teams from a last-minute scramble. With pre-built templates, real-time dashboards, and audit-ready reports, accounting teams expedite the month-end close process without cutting corners.

Ebooks

Still Reviewing Entries Manually? Agentic AI Can Do It in Seconds.

See how CFOs are replacing repetitive accounting checks with autonomous precision.

The biggest roadblocks in reconciliation come from within: fragmented systems, manual workarounds, and poor visibility. Here’s what’s really holding finance teams back.

1. Spreadsheet dependency creates bottlenecks

Teams juggling reconciliation manually waste valuable hours just trying to get clean numbers. Especially with teams that still rely on spreadsheets for reconciliation efficiency, they find it extremely difficult to keep up with the modern accounting demands. Moreover, the lack of standardization leads to inconsistent processes and increased audit risk.

2. Transaction volume exceeds capacity

Businesses often see too many transactions and too little time. Without proper transaction reconciliation, finance teams may rush critical recon tasks, leading to downstream reporting issues. Errors pile up, and finance teams are stuck cleaning up instead of closing faster.

3. Unexplained gaps in data

Missed entries, reversed transactions, or forgotten adjustments aren’t just clerical issues—they directly impact trust in the financial close. Businesses often lack stakeholders’ confidence and erode credibility, with stakeholders questioning reports.

4. Poor timing and cutoff differences

When systems operate on different timeframes, mismatched balances become inevitable. If not caught quickly, they distort your month-end view. It often results in time-consuming back-and-forth just to justify what’s already been booked.

5. Hidden fraud risk

Lack of reconciliation between independent systems creates blind spots where fraud can fester. Businesses need a robust architecture that not only detects fraud but also removes the spaces where it could hide. Without early detection, financial damage escalates long before red flags are raised.

Best Practices for Account Reconciliation

Account reconciliation is only as strong as the process behind it. The following practices help finance teams tighten controls, eliminate inefficiencies, and maintain clean, audit-ready records, without slowing down the close.

1. Maintain a consistent reconciliation schedule

Account reconciliation should be done regularly—weekly or monthly—based on volume and risk. Waiting too long means errors go unchecked and snowball into bigger problems, causing disruptions throughout the books and systems.

2. Leverage automation to streamline workflow

Manual spreadsheets don’t scale. It’s high time for finance teams to use advanced, automated account reconciliation tools that integrate with your ERP to automate transaction matching, flag anomalies, and accelerate close cycles. It’s how finance teams regain time and control.

3. Establish clear role separation

Accountants must segregate duties across initiation, recording, and reconciliation. When one person owns too many steps, errors and fraud slip through. Strong internal control starts with separation.

4. Ensure proper documentation standards

Account reconciliation goes beyond mere accounting arithmetic. It’s the first and most important step of an audit. Log discrepancies, track who approved changes, and build a clear trail. Clean documentation helps build a defense in audits and reviews.

5. Incorporate a formal review step

Every account reconciliation should go through a second layer of review. The purpose of the process is to ensure integrity in your finances. Teams must get another set of eyes on it before it hits reporting.

Accelerate Your Account Reconciliation With HighRadius’ Agentic AI-Led Account Reconciliation Software

Legacy account reconciliation tools leave too much work in spreadsheets. Finance teams manually pull data, hunt down discrepancies, and rely on email to resolve exceptions. The process slows month-end close, consumes accounting bandwidth, and increases audit risk. Without automation, teams spend more time fixing issues than analyzing the numbers.

HighRadius’sAccount Reconciliation and financial reconciliation software bring in exclusive automated account reconciliation features that replace fragmented reconciliation with connected, real-time workflows. Teams configure matching logic, auto-certify low-risk accounts, and manage exceptions using built-in workflows. Moreover, automated transaction matching capabilities give a real-time snapshot of matched vs unmatched transactions, helping accountants work faster with fewer errors. The result? Finance teams cut reconciliation timelines by up to 30% and achieve 99% accuracy.

Take a deep dive into HighRadius’ R2R solutions

Getting granular visibility and control into your accounting process is just a click away.

Achieve up to 90% transaction auto match without of the box matching rules

Financial Close Management

Reduce days to close by 30% with detailed checklist for month end close

Anomaly Management

Resolve 80% of anomalies with auto suggested actions.

FAQs For Account Reconciliation

1. Why is account reconciliation important?

Account reconciliation validates the accuracy of financial records and ensures that balances reported in the books match actual transactions. For CFOs, it is a critical control that supports compliance, audit readiness, and investor confidence.

2. What are the different types of account reconciliation?

The most common types are bank reconciliation, general ledger reconciliation, intercompany reconciliation, credit card reconciliation, balance sheet reconciliation, accounts receivable reconciliation, and accounts payable reconciliation. Together, these ensure that every transaction is accounted for and reported accurately.

3. How does automation improve account reconciliation?

Automation reduces the dependency on manual spreadsheets, accelerates exception handling, and provides a transparent audit trail. By automating account reconciliation, finance teams can shorten close cycles, improve accuracy, and reduce compliance risks.

4. How often should businesses perform account reconciliation?

Most organizations reconcile accounts monthly. However, high-volume or high-risk accounts may require weekly or daily reconciliation. The frequency should be aligned with transaction volume, risk exposure, and reporting deadlines.

5. How does account reconciliation support audits and compliance?

Auditors often review account reconciliation controls as part of financial reporting evaluations. A consistent and timely process demonstrates compliance with frameworks such as US GAAP and IFRS, while also reducing the burden of evidence gathering.

6. What are the risks of not performing account reconciliation?

Failure to reconcile accounts can result in inaccurate financial reporting, exposure to fraud, delayed close cycles, and compliance penalties. Over time, it can undermine credibility with auditors, regulators, and stakeholders.

7. What is an account reconciliation system?

An account reconciliation system is a software solution that automates the matching of financial records, identifies discrepancies, and ensures the accuracy of the general ledger. It replaces manual spreadsheets with AI-driven workflows and real-time dashboards.

8. What are the benefits of account reconciliation services?

While account reconciliation services involve outsourcing the process to third-party experts, most modern enterprises prefer software-as-a-service (SaaS) to maintain better data security, lower costs, and achieve real-time visibility into their financial health.

HighRadius Named a Challenger In 2025 Gartner® Magic Quadrant™ for Financial Close and Consolidation Solutions

HighRadius stands out as a challenger by delivering practical, results-driven AI for Record-to-Report (R2R) processes. With 200+ LiveCube agents automating over 60% of close tasks and real-time anomaly detection powered by 15+ ML models, it delivers continuous close and guaranteed outcomes—cutting through the AI hype. On track for 90% automation by 2027, HighRadius is driving toward full finance autonomy.

HighRadius Named ‘Rising Star’ in 2024 ISG Provider Lens™ Finance and Accounting Platforms Report

HighRadius leverages advanced AI to detect financial anomalies with over 95% accuracy across $10.3T in annual transactions. With 7 AI patents, 20+ use cases, FreedaGPT, and LiveCube, it simplifies complex analysis through intuitive prompts. Backed by 2,700+ successful finance transformations and a robust partner ecosystem, HighRadius delivers rapid ROI and seamless ERP and R2R integration—powering the future of intelligent finance.

HighRadius Named As A Major Player For Treasury & Risk Management Software By IDC

HighRadius is redefining treasury with AI-driven tools like LiveCube for predictive forecasting and no-code scenario building. Its Cash Management module automates bank integration, global visibility, cash positioning, target balances, and reconciliation—streamlining end-to-end treasury operations.