B2B Credit Management: Meaning, Process, and How It Works

B2B credit management is the end-to-end process of assessing, approving, and monitoring customer credit to control risk and protect cash flow. Modern systems use AI and automation to enable faster, consistent, and data-driven credit decisions.

1. What is B2B credit management?

B2B credit management is the structured process of evaluating, approving, monitoring, and controlling credit extended to business customers across the order-to-cash (O2C) cycle. It combines credit risk analysis, policy enforcement, and continuous monitoring to ensure revenue protection while enabling sales growth.

2. How does B2B credit management work in practice?

B2B credit management operates as a multi-stage workflow that spans customer onboarding, risk evaluation, decisioning, and ongoing monitoring.

It begins with credit application processing, where customer data and financials are collected and validated. This is followed by credit risk scoring, where internal and external data are analyzed to assign risk levels. Based on predefined policies, the system executes credit decisioning, including approvals, rejections, or limit assignments.

Post-decision, continuous monitoring and alerts ensure that changing customer behavior is captured and acted upon in real time.

With automated credit management, you unlock 70% faster credit decisions!

Check our Credit Management Software Datasheet to learn more.

3. What are the core components of a B2B credit management process?

A modern B2B credit management system includes tightly integrated components:

- Credit application processing – Data capture, online credit application processing and validation, and workflow routing

- Credit risk scoring – AI-driven credit scoring software that uses financial, behavioral, and external data

- Credit decisioning – Policy-based approvals, limit assignment, escalation and faster credit decisioning and credit review

- Credit agency and financial data integration – External data enrichment from bureaus and filings

- Continuous risk monitoring – Real-time alerts for credit events and behavioral changes

- Workflow automation – Standardized approval hierarchies and exception handling

These components work together to ensure consistent, scalable, and auditable credit decisions.

4. What role does AI play in B2B credit management?

AI transforms B2B credit management from a periodic, manual process into a continuous, decision-driven system.

AI models analyze structured and unstructured data, such as payment behavior, financial ratios, and external risk signals to generate dynamic risk scores. They also enable automated credit decisioning, where low-risk cases are approved instantly, and high-risk cases are escalated with context.

In advanced systems, AI agents also process B2B credit applications, predict blocked orders, payment delays, and risk deterioration, allowing teams to act before revenue is impacted.5. How is credit risk evaluated in B2B environments?

Credit risk evaluation in B2B credit management combines multiple data layers:

- External data – Credit bureau scores, public financials, trade association data

- Internal data – Payment history, credit utilization, order behavior

- Derived metrics – Financial ratios such as debt-to-equity and liquidity indicators

These inputs are processed through scoring models that dynamically adjust weightage based on customer segment, geography, and risk profile, ensuring more accurate and context-aware decisions.

6. What is automated credit decisioning in B2B credit management?

Automated credit decisioning refers to the use of predefined rules, scoring models, and AI-driven recommendations to approve or reject credit requests without manual intervention.

For example, low-risk customers or small credit limit requests can be auto-approved based on thresholds, while higher-risk cases are routed through approval workflows. This ensures faster decisions while maintaining policy control and auditability.

3 tips to shorten credit review cycles and keep customer onboarding moving.

Read our Credit Review Guide to learn more.

7. How does B2B credit management impact the O2C process?

B2B credit management acts as the control layer within the O2C cycle, determining whether orders are approved, fulfilled, or blocked.

Strong credit management ensures:

- Faster customer onboarding

- Reduced order blocks

- Improved collections outcomes

- Lower bad debt

Weak credit management, on the other hand, leads to delayed approvals, revenue leakage, and increased risk exposure.

8. What challenges do companies face in B2B credit management?

Operational inefficiencies in data, decisioning, and workflows create systemic challenges in scaling B2B credit management.

- Fragmented data across systems:

Customer credit data is scattered across ERPs, bureaus, and spreadsheets, making it difficult to form a unified and reliable risk view.

- Manual and inconsistent credit decisions:

Credit scoring and application tools depend on individual analyst judgment, leading to variability in decisions and lack of standardization.

- Limited visibility into real-time risk:

Static reports fail to capture changing customer behavior, delaying identification of emerging credit risks.

- Delays in onboarding and approvals:

Manual data collection, validation, and approval workflows slow down customer onboarding and order processing.

- Difficulty scaling credit operations:

As volumes increase, manual processes cannot keep pace, limiting the ability to manage larger and more complex credit portfolios efficiently.

9. How do modern systems improve B2B credit management?

Modern B2B credit management software uses automation, AI, and integrations to standardize and scale credit processes.

They enable:

- Real-time credit risk monitoring:

Continuously tracks customer behavior, payment patterns, and external risk signals to identify changes in creditworthiness as they happen.

- Centralized customer data and hierarchy management:

Consolidates data across ERPs, credit bureaus, and regions into a unified view, enabling parent-child hierarchy mapping and global credit exposure control.

- Automated workflows for approvals and reviews:

Standardizes credit approvals, periodic reviews, and escalation paths using rule-based and AI-driven workflows to eliminate manual intervention.

- Proactive alerts for risk events:

Detects critical events such as payment delays, credit rating changes, or financial deterioration and triggers immediate review or action.

- Consistent, policy-driven decisioning:

Applies predefined credit policies, scoring models, and thresholds to ensure uniform and auditable credit decisions across all customer segments.

This shifts credit management from a reactive function to a proactive, data-driven control system.

A Wrong Credit Management Vendor Can Increase Bad Debt by 20%.

Use our Free Vendor Evaluation Scorecard to find the right fit.

10. Why is B2B credit management critical for business performance?

B2B credit management directly impacts cash flow, revenue realization, and risk exposure.

Effective credit processes reduce bad debt, improve working capital, and accelerate the order-to-cash cycle, while ensuring that credit decisions support growth without increasing financial risk.

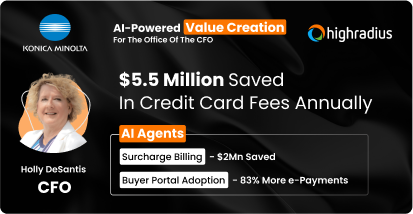

From Chaos to Cash: How Finance Teams Reclaimed Millions in 6 Months

Leading enterprises are rethinking credit and collections with AI—automating everything from credit scoring and blocked order prediction to high-risk account follow-ups and dispute resolution. In just 6 months, they’ve seen 20% drop in bad debt, and unlocked over $2M in additional cash flow.

Book A Discovery Call